당시에 MDS (myelodysplastic syndrome)에 대한 임상3상 결과가 좋아서 FDA 승인이 기대가 되는 상황이었습니다. 오늘 FDA의 Advisory Committee Meeting이 있었는데 12:2로 승인을 하는 쪽으로 결론이 났습니다. 물론 FDA가 이 결정에 따룰 이유는 없지만 그래도 최종 결정에 긍정적인 결과를 주리라고 기대합니다.’

현재 MDS의 치료제로는 erythropoiesis-stimulating agents (ESA)가 거의 유일한 치료제라고 해도 무방한데 Geron은 Imeltestat을 ESA에 듣지 않는 환자들에 대한 치료제로 승인 요청을 할 예정입니다. Imetelstat에 대한 PDUFA date는 6월 16일입니다.

Members of the FDA’s Oncologic Drugs Advisory Committee voted 12 to 2 on Thursday that the benefits of Geron’s imetelstat outweigh safety risks for the treatment of certain anemic myelodysplastic syndrome (MDS) patients who are dependent on blood transfusions.

While regulators raised concerns around cases of cytopenia, or low levels of white blood cells or platelets, advisory committee members said they were confident that the risks appear manageable. The FDA noted on Thursday that there was a “notably higher” incidence of neutropenia and thrombocytopenia in the imetelstat arm of a Phase III trial.

“Though I am concerned about the risks in this total trial population — in other words, not just the responders — I do believe it is more likely than not that there is a quality-of-life benefit here that is real,” University of Colorado associate professor Christopher Lieu said.

Stanford University School of Medicine professor Ranjana Advani added, “The community of doctors who take care of these patients know how to manage these side effects.”

Members also pointed to the fact that imetelstat met its primary endpoint in a Phase III trial, helping patients achieve eight-week red blood cell-transfusion independence, as well as a key secondary endpoint measuring 24-week independence.

MDS occurs when the normal production of blood cells is disrupted. Most patients with lower-risk MDS experience anemia, which can cause symptoms ranging from fatigue to irregular heartbeat and has also been linked to shorter survival. Those with severe anemia may be dependent on continuous transfusions. Patients who spoke during the adcomm stressed that frequent transfusions impacts their quality of life.

Ravi Madan, a senior clinician head at the National Cancer Institute’s Center for Cancer Research, was one of two members who voted against imetelstat’s benefit-risk analysis.

“I interpreted the question pretty strictly,” he said. “Even low-risk MDS patients are at high risk from their disease, but they shouldn’t also be at risk from their treatments as well.”

The FDA also raised concerns in briefing documents published in advance of the meeting that a majority of patients in the only randomized efficacy trial for imetelstat were enrolled outside of the US. Geron’s chief medical officer Faye Feller acknowledged that a majority of patients were from the EU, but assured the committee that “overall, the demographics are representative of the US MDS population.”

Traditionally, a class of drugs called erythropoiesis-stimulating agents (ESA) have been used off-label to treat lower-risk MDS patients with transfusion-dependent anemia. Bristol Myers Squibb’s Revlimid and Reblozyl are approved to treat anemia in MDS patients, and last year Reblozyl won a label expansion for first-line lower-risk patients who may require transfusions.

But Vanderbilt University School of Medicine professor Michael Savona, who was a member of the steering committee for imetelstat’s Phase III trial, said the use of those drugs is restricted to specific subgroups of patients.

“After failure of ESAs there is no good therapy for most patients,” he said during the meeting.

Geron is seeking approval for patients who have failed on or are ineligible for ESA treatment.

Johnson & Johnson saw early potential in imetelstat, shelling out $35 million upfront and promising another $900 million in milestones to partner on the drug a decade ago. The company backed out of the collaboration four years later, citing “a strategic portfolio evaluation and prioritization of assets.”

GRO Biosciences Inc. today announced that the company has secured $2.1 million in a seed funding round led by Digitalis Ventures and joined by Eric Schmidt’s Innovation Endeavors. The funds will support buildout of bioprocess development for GRO Biosciences’ platform of genomically recoded bacteria for the production of therapeutic proteins with enhanced properties, such as increased potency and stability, and improved targeting and delivery into cells and tissues.

GRO Biosciences was co-founded by the following:

George M. Church, Ph.D., professor of genetics, Harvard Medical School, will serve as head of the company’s scientific advisory board.

Andrew D. Ellington, Ph.D., professor of biochemistry, University of Texas at Austin, will serve on the company’s scientific advisory board.

Daniel J. Mandell, Ph.D., will serve as the company’s CEO.

Christopher J. Gregg, Ph.D., will serve as the company’s chief scientific officer.

P. Benjamin Stranges, Ph.D., will serve as the company’s principal scientist.

Marc J. Lajoie, Ph.D., and Ross Thyer, Ph.D., will serve the company in advisory roles on a consulting basis.

By recoding the genomes of bacterial strains used in biologics production, GRO Biosciences can expand beyond the 20 amino acid building blocks typically found in proteins to introduce non-standard amino acids that can customize the shape and chemical properties of the protein.

“For decades, bacteria have been used as the workhorses of the biotech industry in the production of blockbuster therapeutics, and we believe that we can dramatically expand their utility by recoding their genomes,” said Dr. Church. “GRO Biosciences’ technology addresses the fundamental limitations of producing proteins with non-standard amino acids, opening up the possibility of creating a new universe of designer proteins with enhanced therapeutic properties at commercial scale.”

Nearly all monoclonal antibodies, as well as many other therapeutic proteins, such as interferon, human growth hormone and insulin, used to treat common chronic conditions, rely on disulfide bonds to maintain their 3-dimensional structure needed for biological activity. However, disulfide bonds are not stable in the presence of reducing agents found in cells and in blood, which means that the therapeutic effect of the proteins is short lived after administration to the patient.

(Picture: Andrew D. Ellington at University of Texas at Austin)

GRO Biosciences is addressing the challenge of therapeutic protein instability by replacing disulfide-bond-forming cysteine amino acid residues with selenocysteine, a naturally-occurring amino acid that is rarely incorporated into proteins, but is found in the cell. Selenocysteine has a structure and chemical properties very similar to cysteine, however diselenide bonds are stable under the same conditions where disulfide bonds are not, leading to a much longer half-life of the therapeutic protein.

“Protein therapeutics represent a $180 billion market, yet product stability, targeting and delivery into the cell still remain significant challenges to be addressed if we are to enhance the patient experience, achieve better compliance and improve health outcomes,” said Geoffrey W. Smith, founder and managing partner of Digitalis Ventures. “If GRO Biosciences can make a therapeutic protein product that is more stable and requires less frequent dosing, then that is a win for patients and the healthcare system.”

GRO Biosciences is taking advantage of redundancies in the genetic code to reassign redundant codons to new, non-standard amino acids. For example, there are three different stop codons which are responsible for halting the elongation of a growing protein: UAG, UAA and UGA. GRO Biosciences has developed a recoded strain of bacteria that has replaced all of the UAG stop codons with UAA stop codons and reprogrammed the UAG codon to new amino acids such as selenocysteine. By replacing all codons that code for cysteine residues in a protein with UAG, selenocysteine can be selectively incorporated in place of cysteine residues to form stabilizing diselenide bonds.

“GRO Biosciences is literally reprogramming biology,” said Dror Berman, Managing Partner of Innovation Endeavors. “What I find most compelling is their ability to converge game-changing synthetic biology with powerful computational design to create a new class of living organisms, unlocking unprecedented capabilities in medicine, materials and biotechnology.”

GRO Biosciences has established preliminary proof of concept of its platform by producing diselenide stabilized antibody products as well as therapeutic proteins, such as human growth hormone, in its selenocysteine recoded bacteria. In all instances, yields were high, selenocysteine incorporation at the desired sites was 100 percent, and all diselenide bonds formed correctly leading to the properly folded protein. The diselenide bonds dramatically increased stability in physiologically relevant conditions, as confirmed by functional assays.

Many of the protein therapies available now, as well as many more still in development, got their start on computers. Software identifies the protein shapes best suited for therapeutic applications and those designs are tested in a lab. While computational techniques have advanced the design and development of new therapeutic proteins, even the most advanced of these are limited to 20 standard amino acids found in nature that are building blocks of all proteins. Harvard University spinout GRO Biosciences aims to improve protein therapies by expanding this amino acid alphabet.

GRObio has been quietly developing its technology for the past several years. The company has made progress in its preclinical research and it’s now positioning itself to advance its own therapies, and to strike up partnerships with pharmaceutical companies interested in working with the startup’s technology. To support those efforts, GRObio announced on Wednesday a $25 million Series A round of funding co-led by Leaps by Bayer and Redmile Group.

The science behind GRObio comes from the lab of George Church, a Harvard scientist whose discoveries have led to the founding of many life sciences startups. Dan Mandell, GRObio’s co-founder and CEO, was a research fellow in genetics at Harvard, where he worked with Church on computational design of new proteins whose folding and function depends on this new amino acids alphabet, comprised of non-standard amino acids (NSAAs).

Therapeutic proteins are produced by harnessing the protein-translation machinery of bacteria. Companies such as Ginkgo Biosciences, Synlogic, and Absci work with E. coli to produce their commodity chemicals and proteins. For many synthetic biology companies, E. coli are the bacteria of choice because they are inexpensive and easy to use, Mandell said. GRObio also works with an E. coli-based organism. But the company has gone further than what nature provides by recoding the E. coli genome so that these bacteria are able to produce proteins by using NSAAs. GRObio calls these bacteria “genetically recoded organisms,” or GROs.

“What’s special about these organisms is they can make proteins comprised of amino acids beyond the 20 standard amino acids,” Mandell said. “These organisms are the only organisms that can produce these NSAA proteins at high efficiency, and at scale.”

So why would anyone want a GRO-produced protein made from NSAAs? Mandell said that therapeutic proteins made with standard amino acids still have limitations ranging from safety issues to the durability of the treatment. Working with NSAAs enables the production of customized proteins whose shape and chemical properties offer advantages for a biologic drug.

GRObio is working with two families of NSAA chemistries so far. The first, which the company calls DuraLogic, makes a protein that is more stable and improves its half-life. Currently available biologic drugs dosed as frequent injections are inconvenient or undesirable (or both), which leads many patients to miss doses, Mandell said. By making a more stable protein, GRObio could produce a drug whose therapeutic effect lasts for a longer period of time, which means a protein therapy that requires less frequent injections.

The second NSAA family, which GRObio has dubbed ProGly, enables the biotech to directly modulate the immune system, offering a new way to address autoimmune diseases. The way the immune system distinguishes a foreign protein from one that is part of the body is by detecting sugar molecules called glycans on the protein’s surface, Mandell said. GRObio aims to express proteins decorated with human glycans, which would reeducate the immune system to recognize them as belonging to the body.

GRObio hasn’t disclosed what diseases it aims to address, other than to say the technology has applications in autoimmune and metabolic disorders. One of the company’s early projects was a form of insulin modified in a way to enable weekly dosing. The company wasawarded a Phase I Small Business Innovation Research grant in 2019 for that research, followed by a Phase II grant in 2020. Mandell acknowledged that GRObio has worked on insulin, and said the company has received about $1.5 million in non-dilutive capital to support that work.

Without specifying a disease target, Mandell said he expects GRObio could begin its first human tests of a GRO-grown therapeutic protein in 2024. The new financing will support the preclinical research leading up to those tests. GRObio is also looking for pharmaceutical industry partners. Those partners could license GRObio therapeutic candidates, taking on the responsibility of clinical development and potential commercialization of new protein therapies.

Mandell said GRObio is also considering alliances with companies that want to work with NSAAs but can’t because they don’t have access to a production platform that can produce NSAA-based proteins at scale. Mandell said GRObio has been approached by companies that have already designed their own new molecules and are looking at GROs as a way to produce them.

Prior to Wednesday’s funding announcement, GRObio had raised $2.1 million in a 2017 seed financing led by Digitalis Ventures and Innovation Endeavors. Those firms also joined the Series A round, bringing the startup’s total investment to $31.2 million to date.

Genomics and synthetic biology pioneer George Church, PhD, says GRO Biosciences (GRObio), a developer of enhanced protein therapeutics he co-founded based on platform technology discovered in his Harvard Medical School lab, reflects a truism about startup formation.

“Every postdoc has an invention, but not every invention is something that we want to immediately launch,” Church, who heads GRObio’s scientific advisory board, observed recently on “Close to the Edge”, GEN Edge’s video interview series. “We try to incubate them as long as possible inside the lab until we’re sure that they’re mature enough so that we won’t get diluted out immediately by running out of VC [venture capital] money.”

GRO stands for “genomically recoded organisms”—the first production organisms made with modified genomes and engineered protein translational machinery, according to the company.

By recoding the genomes of bacterial strains used in biologics production, GRObio reasons that it can expand beyond the 20 amino-acid building blocks typically found in proteins to introduce non-standard amino acids (NSAAs) that can customize the shape and chemical properties of the protein.

“What we do is to systematically alter the genetic code,” Daniel J. Mandell, PhD, who is GRObio’s CEO, summed up to GEN Edge.

Church’s Harvard Medical School lab first described and characterized GROs in a paper published in 2013 in Science.

In 2015, Church, Mandell and seven co-authors reported in Nature their successful computational redesign of essential enzymes in the first organism possessing an altered genetic code, conferring metabolic dependence on NSAAs for survival.

The following year, Church led a research team in applying recoding to design and synthesize a bacterial genome, an exercise designed to show how new organisms could be created that feature functionality not previously seen in nature.

Also in 2016, Church, Mandell, and four others co-founded GRObio to commercialize the technology by developing protein therapeutics based on computational protein design and synthetic biology technologies. Among the co-founders are Andrew Ellington, PhD, whose lab at the University of Texas at Austin focuses on developing novel genetic codes and synthetic organisms based on engineering the translation apparatus; and Christopher Gregg, PhD, GRObio’s chief scientific officer (CSO).

Mandell was wrapping up a PhD in computational protein design at University of California, San Francisco, about a decade ago, and seeking a postdoctoral position when he came across Church’s research on GROs.

“It was an epiphany”

“For me it was an epiphany: Now we can go beyond the 20 amino acids and build designer proteins that can carry out almost any function. I came to George’s lab to bring these two worlds together of computational protein design and genome-wide recoding,” Mandell recalled.

Daniel J. Mandell, PhD, GRO Biosciences co-founder and CEO

“We did some early work demonstrating that you can in fact predictably engineer proteins whose folding and function depend upon non-standard amino acids, to convince ourselves that we really can do this in a rational way. That’s when we turned our attention to the question of what are the outstanding problems in the clinic that we might address using that technology.”

Mandell joined Church’s lab within a year of Gregg joining: “We very quickly realized we both had entrepreneurial designs and mesh very well, and we put a lot of time into thinking about how we could try to commercialize this technology.”

Gregg, now GRObio’s CSO, was pursuing a PhD in glycobiology, studying how glycans interact with the immune system. He started a short-lived synthetic biology startup focused on biofuel, before switching gears to integrating synthetic biology with organism and genome design.

“Luckily, I was able to get George’s interest in my thesis, which had to do with glycobiology and human-specific disease preponderances,” Gregg recalled. “I came in as the organism [GRO] was getting finished. It was just such a ripe platform for trying new things and solving new problems. Then when Dan and I realized that we had the same interests, we just started running with it.”

That pursuit paid off for GRObio last month, when it completed a $25-million Series A financing co-led by Leaps by Bayer and Redmile Group. Redmile is a San Francisco venture and private equity investment firm. Leaps is the equity investment arm created by Bayer to establish new companies and invest in early-stage technologies with breakthrough potential to “fundamentally change the world for the better.”

Bayer came to invest in GRObio, Mandell said, through relationships he had with the pharma/consumer goods/agbio giant and contacts from GRObio’s network of investors. Among investors joining the financing were Digitalis Ventures and Innovation Endeavors. (The Series A brings total investment in GRObio to $31.2 million so far.)

Proceeds from the financing, GRObio said, will support development of its GRO platform, a scale-up of bioprocess manufacturing, preclinical validation studies, and IND-enabling studies for GRObio’s pipeline of NSAA protein therapeutics designed to treat autoimmune and metabolic diseases.

“These are just initial focus areas,” says Mandell. “Autoimmune disease and metabolic diseases are a really a small part right of this broader universe [of opportunities]. But there are specific indications in there that we’re focusing on.” The company isn’t yet disclosing those indications, except to say they will address unmet clinical needs.

Beyond the pipeline

Taking this universe of NSAA chemistries, Mandell and colleagues want to ask some big questions. “Which problems really can’t be solved in the clinic without this new expanded universe of chemistries at the amino acid level? Some of these problems have interesting-looking solutions coming down the clinical development pipeline,” Mandell said. “That’s not really where we want to play. We want to play in areas where we think we can solve Holy Grail challenges and there isn’t another way to go about this.”

GRObio has constructed a “biofoundry” consisting of proprietary computational protein design and robotics pipelines, with the aim of streamlining development of NSAA translational machinery and NSAA protein products. The biofoundry applies strain and genome engineering, automation, analytics, and protein design software to build uniquely scalable NSAA protein “factories” from trillions of candidates.

GRObio emerged from stealth mode in 2017, raising $2.1 million in seed funding led by Digitalis Ventures, with participation from Innovation Endeavors, the venture capital firm whose co-founders include Eric Schmidt, Google’s former CEO and later executive chairman of Google and its parent company, Alphabet Inc.

From three people when it started, GRObio has since grown its staff to 16 people. “We will double in size by 2023,” Mandell said.

GRObio hopes its alphabet-expanding approach will enable it to grow its own significant share of a protein therapeutics market that according to Market Research Future (MRFR) is expected to increase over the next six years at a compound annual growth rate of 6.86%–for a nearly 60% rise to about $290.69 billion in 2027 from $182.69 billion this year.

GROs are intended for high-efficiency, commercial-scale production of proteins with NSAAs. These NSAAs are intended to enhance protein therapies with capabilities such as unprecedented duration of action and more precise control of the immune system.

GRObio is building its pipeline by advancing its first two product families of NSAA platform chemistries: DuraLogic™ is designed to enable flatter pharmacodynamic profiles and relaxed dosing schedules, while ProGly™—short for “programmable glycosylation”—are designed to produce biologics that enable the immune system to treat autoimmune disease, or to eliminate immunogenic side effects of protein-based therapies.

DuraLogic integrates NSAAs to enhance and maintain the three-dimensional structure of proteins needed for therapeutic activity. “That means things like resistance to proteases that can degrade the therapeutic, resistance to reducing agents that can break bonds in the protein that will render it inactive or misfolded, and the potential in some cases to increase the thermostability of the protein, so it can either last longer in storage, or just have a longer in vivo half-life,” Mandell said.

ProGly consists of glycan-containing NSAAs designed to induce or inhibit an immune reaction. GRObio says its GRO platform enables precise placement of defined ProGly compositions on the protein surface needed to elicit immune response.

Re-educating the immune system

“You can actually retrain or re-educate the immune system to treat a particular protein as self or non-self by administering that protein with a particular glycan’s signature. You give it what’s called a tolerizing signature,” Mandell explained. “The body will remember that this is a self-protein, and over a short period of time can begin to actually reverse the autoimmune response to that protein.”

GRObio expresses that protein in its platform, decorated with ProGly NSAAs that take on the form of human-like glycans.

“By putting that into your body, your immune system begins to learn that this is a self-protein and it builds up an immune memory of that protein and stops attacking it,” Mandell said. “This is really a way that we can begin to reverse a number of different autoimmune diseases, by taking an antigen-specific approach.”

That approach, he added, contrasts with broadly immunosuppressive drugs that turn down auto immune response by knocking down a patient’s immune system—an approach Mandell said increases susceptibility to infection and cancer and also often causing metabolic disorders: “What we want to do is re-educate the immune system to treat the one protein or the small number of proteins that you’re reacting to as self-proteins for the first time.”

The genetic code of each gene combines the four natural nucleotides of DNA—adenine (A), cytosine (C), guanine (G), and thymine (T)—to spell out three-letter codons specifying an individual amino acid. There are 64 different naturally occurring codons that encode 20 natural amino acids.

“What we did was to modify the genome to remove all the instances of one or more of those codons. Then, by installing on what we call new translational machinery from the cell that recognizes a particular codon, we can actually now reassign the meaning of part of the genetic code to direct the incorporation of a new amino acid,” Mandell said.

The company’s GRO platform expands the amino-acid alphabet to overcome limitations of protein therapeutics to address product stability, immunogenicity, and delivery into the cell.

Exploiting redundancies

“We’re exploiting redundancies in the genetic code to reassign redundant codons to new, non-standard amino acids, because there’s more than one way to specify a particular amino acid or stop,” Mandell explained.

For example, three codons code for the “stop” signal (UAG, UAA, and UGA), halting the elongation of a growing peptide chain. GRObio developed a recoded strain of bacteria that replaces all UAG stop codons with UAA stop codons and reprogrammed the UAG codon to new amino acids such as selenocysteine, a naturally occurring amino acid found in the cell, yet rarely incorporated into proteins.

By replacing all codons that code for cysteine residues in a protein with UAG, selenocysteine can be selectively incorporated in place of cysteine residues to form stabilizing diselenide bonds. Proteins stabilized with diselenides maintain stability and resist the reduction found both in human blood plasma, which destabilizes therapeutics, as well as in solvents and buffers, which destabilize industrial enzymes.

“It was quite evident that people were excited about working with the first recoded strain and they started looking around for what the best products were,” Church recalled. “The first thing we had published on the first NSAA we’ve published for biocontainment was bipA [biphenylalanine], and that did not seem like a good starting product. But diselenides, which we did in collaboration with Andy Ellington’s lab, looked like a great initial product, and that was quite enough to get the company launched.”

Gregg cited insulin as an example of a treatment that could be engineered for less frequent dosing through a selenocysteine NSAA that could be designed to prevent the breaking of bonds between the peptide chains that renders the molecule non-functional.

“Now all of a sudden,” he said, “you’ve got a fundamental mechanism by which you can say, this NSAA will support the survival of this molecule in this environment, on a timescale that we think will be beneficial to patients as a product.”

Synthetic biology has brought many breakthroughs to the biotherapeutics space over the last decade. The dropping cost of sequencing and precision genome editing has paved the way for personalized medicine. At the same time, generative AI technology has enabled the designing of antibodies with a much higher clinical success rate. Yet, scientists’ ingenuity is still challenged by the laws of biology. All biologics are susceptible to unpredictable degradation rates and immune responses, in addition to being constrained to the 20 natural amino acids that make up these therapeutics.

But now, one company is challenging that paradigm. Pearl Bio, a synthetic biology company backed by Khosla Ventures, has recently emerged from stealth mode with a hefty IP portfolio of 24 patents that protect their groundbreaking technology: a genetically recoded organism. With it, Pearl Bio is creating entirely new classes of materials for smart biologics.

Pearl’s genetically recoded organism, combined with the engineered translational machinery of the cell, breaks the rules of life by enabling the incorporation of building blocks beyond the 20 amino acids that exist in nature. This technology can disrupt the medical paradigm by producing novel chemistries that solve existing challenges in the immunotherapeutics space and pave the way to completely new materials.

What is a Genetically Recoded Organism (GRO)?

Pearl’s cornerstone technology is a genetically recoded organism (GRO), which heralds a new era of synthetic biology. The rules of life are written in a four-letter genetic code: A, T, C, and G. These letters form three-letter words—called codons—that encode the amino acids which make up the tissues and enzymes of all living beings. However, biology is not perfect: there are 64 possible combinations of ATCG but only 20 amino acids. This phenomenon is known as “redundancy.”

The idea of using those redundant codons for a practical purpose has been around for a while. “It dates back to the late 2000s. I was working as a postdoc in George Church’s lab, together with Michael Jewett,” recalls Farren Isaacs, Co-founder and Science Advisor at Pearl Bio. “We were always the first people to get to the lab in the morning. There was no one around at that time, and we would brainstorm ideas.”

Isaacs and Jewett, Pearl Bio’s other Co-founder and Science Advisor, were working on the bleeding edge of synthetic biology at that time: “I was recoding genomes, and Michael was engineering ribosomes. We realized that when you put those two technologies together, you have the ability to basically repurpose the genetic code and the translational machinery of any cell to produce entirely new materials,” says Isaacs.

In 2013, scientists from the Isaacs lab managed to free up one of those three-letter combinations by editing the entire E. coli genome. Now the missing codon could be assigned to code for anything else, such as non-natural amino acids, which do not occur in any living beings. By introducing these new-to-nature building blocks, you could make proteins that are impervious to degradation, target specific tissues and disease states,and attach highly specialized payloads.

“That could lead to fundamentally new kinds of therapeutics that have longer stability and reduced immunogenicity,” says Isaacs.

A New Way to GRO

Years went by, but Isaacs, Church, and Jewett kept working on tweaking the technology to improve and expand on what it could do. In 2020, the two decided to co-founder Pearl Bio together with Amy Cayne Schwartz, Chief Operating Officer & Chief Business Officer, and George Church and Jesse Rinehart of Yale as Science Advisors. Pearl Bio was officially financed and launched in Q3 of 2021.

“This is something that we’ve been incubating over many years: developing the technology, de-risking proof of concept, and filing IP,” says Isaacs. “With platform technology companies, you want to be poised to advance product development from day one.”

And Pearl Bio was. They had been working to secure an impressive portfolio of 19 patents to corner the market of multi-functionalized biologics. The newly issued U.S. patent 11,649,446 gives Pearl Bio the exclusive license for engineering programmable biologics by encoding synthetic chemistries and now brings their total patent figures to 24.

When the paper describing the first GRO was published in 2013, the technology and the strain were released publicly. But just like the first version of iOS, there were many things that needed to be improved to make the strain better suited for commercial applications. For example, the initially published version only had one codon freed up, which meant that it could only encode one alternative amino acid. Pearl took this concept further and now also holds exclusive rights to a newly developed GRO with two open coding channels to endow multi-functionality into protein therapeutics.

“Another key piece of IP is the orthogonal tethered ribosomes. This allows Pearl to engineer the ribosome to work efficiently with exotic substrates beyond L-alpha amino acids, opening access to new classes of therapeutic biomaterials. This capability holds promise to transform biopharmaceutical development,” says Jewett.

Other companies have also taken a stab at challenging the paradigm within the biotherapeutics space. For example,Ambrx, a clinical-stage biopharmaceutical company using an expanded genetic code technology, IPO’d for $126 million in 2021. However, Ambrx’s technology does not use genetically recoded organisms. Synthorx is another synthetic genome company in this space which was acquired by Sanofi for $2.5 billion in 2019. Their Expanded Genetic Alphabet technology that adds a novel DNA base pair can be used to create optimized biologics. GRO Biosciences, a company in Cambridge, MA, is expanding the amino acid alphabet to deliver on the promise of protein-based therapies. Their platform comprises Genomically Recoded Organisms (GROs) for high-efficiency production of non-standard amino acid (NSAA) proteins at commercial scale.

What distinguishes Pearl Bio is that they hold a number of broad-blocking patents giving Pearl the exclusive right to encode synthetic amino acids using engineered synthetases and translation machinery to drive multi-site incorporation of synthetic amino acids and other building blocks with site-specificity at high yield and purity.

Schwartz thinks this technology is poised to overcome a lot of the shortcomings of current biologics on the market: “For example, optimizing the drug-antibody ratio has been a defining challenge because when you attach the drug to natural amino acid residues, you are limited in the number and specific location since multiple lysines, for example, are found in a given protein and are critical for its function. Thus, approaches that attach to natural amino acids are constrained, lead to heterogeneous products, and typically ablate protein function. By contrast, Pearl can attach up to 50 synthetic amino acids at monomeric precision to tune therapeutic properties while preserving protein sequence and function.”

Such precision enables the programmability of a therapeutic window with a half-life of up to three weeks to address specific disease indications or patient populations. “With this, we have the opportunity to advance both best-in-class and first-in-class therapeutics to address critical unmet needs and solve challenges plaguing the biologics industry,” says Schwartz.

The Future of Biotherapeutics

Pearl has positioned itself as the leader in this new field thanks to advancing technology and staking the IP landscape. They have developed exclusive next-generation multifunctional capabilities, such as adding synthetic monomers, multiple types of modifications, and multiple locations.

“It’s exciting to see ideas from whiteboards over 15 years ago realized in technologies that are now poised to transform the therapeutic landscape and evolve novel biomaterials. Pearl is pioneering a new era of biotherapeutic design by enabling access to new disease targets and evolution of entirely new classes of molecules,” says Church.

“Today, we can access two distinct functionalities. With our Series A funds, we will advance the technology to access three or more distinct functionalities,” says Schwartz. “We are excited to drive next-generation molecules to the clinic to change the therapeutic landscape with the evolution of smart programmable biologics.”

Pearl Bio, a synthetic biology company backed by Khosla Ventures, is recoding life to create a new era of biologics and biomaterials. A newly issued breakthrough U.S. patent 11,649,446 related to engineering programmable biologics by encoding synthetic chemistries bolsters Pearl’s patent portfolio to corner the market of multi-functionalized biologics with Pearl’s exclusive license to the issued patent. The Pearl team includes world leaders in synthetic biology, genome recoding, and ribosome engineering: Drs. George Church (Pearl Bio, Scientific Advisory Board), Farren Isaacs (Yale University), Michael Jewett (Stanford University) and Jesse Rinehart (Yale University).

“By encoding diverse synthetic chemistries into proteins, Pearl is able to tune half-life, target delivery to diseased cells, and attach cytotoxic payloads to tailor valuable therapeutic properties, overcoming key barriers preventing market approval,” explained Co-Founder Amy Cayne Schwartz. Pearl’s platform leverages 24 exclusively licensed patents and applications evolved over the last decade by the company’s scientific Co-Founders, Dr. Isaacs and Dr. Jewett. The company is advancing partnerships with pharmaceutical companies alongside internal programs to develop next-generation “smart” biologics.

Bringing together the newly-issued patent with existing broad blocking patents on genomically recoded organisms, tethered ribosomes and engineered translational machinery enables access to new frontiers by site-specifically encoding synthetic monomers to derive novel biologics and biomaterials.

Pearl’s technology preserves the natural protein activity while endowing valuable therapeutic properties to address defining challenges in biologic drug development – toxicity, stability, and targeted delivery – fast-tracking the path to market. For example, compounds designed to sustain presence of a cytotoxic payload in the tumor microenvironment coupled with access to novel targets will open-up entirely new therapeutic opportunities to address unmet medical needs and transform patient quality of life.

About Pearl Bio

Backed by Khosla Ventures, Pearl Bio was launched by Scientific Co-Founders Drs. Farren Isaacs (Yale), Michael Jewett (Stanford), and Amy Cayne Schwartz, J.D. (Pearl Bio) bringing together 24 patents in a platform technology to advance multi-functionalized biologics and biomaterials by encoding synthetic chemistries. Broad blocking patents afford freedom to operate, and the company has rapidly advanced capabilities in-house and through pharmaceutical partnerships. Pearl Bio may be followed at: pearlbio.com Twitter: https://twitter.com/PearlBio

20 June 2023. A new U.S. patent, licensed to a start-up biotechnology company, describes processes for linking together chains of synthetic peptides into therapeutic proteins. The U.S. Patent and Trademark Office issued patent number 11,649,446 last month to four inventors at Yale University and elsewhere, including a founder of the company Pearl Bio in Cambridge, Mass. that acquired rights to the technology.

Pearl Bio is a two year-old enterprise discovering synthetic combinations of peptides, short chains of amino acids, for new therapies and bio-based materials. The company is commercializing research by biomedical engineering labs of its scientific founders Farren Isaacs at Yale University and Michael Jewett at Stanford University, as well as Yale physiology professor Jesse Rinehart and Harvard Medical School geneticist George Church. Pearl Bio says the new patent is the latest of 24 patents it licenses exclusively for its basic technology.

The Farren Isaacs lab at Yale studies genome engineering techniques, particularly for high-volume programming of genetic chemistries in single cells and across cell populations. The lab says its discoveries make possible large-scale assembly of genomes into hierarchies that express genetic modifications to achieve desired outcomes, even new organisms if needed. This capability includes engineered protein synthesis in the ribosome, where messenger RNA translates and sequences genetic codes into chains of amino acids to form peptides, then linking together peptides into longer multiple peptide chains and proteins.

Produce synthetic proteins in greater yields

The new patent, which lists Isaacs as the lead inventor and assigned to Yale University, describes processes for preparing multiple peptide chains from amino acids, particularly amino acids not normally found linked together in their natural states. The patent includes methods for producing synthetic proteins in greater yields than conventional processes, or where conventional techniques would not allow for those combinations of amino acids to produce adequate yields or purity, or even occur in some cases.

“By encoding diverse synthetic chemistries into proteins,” says Pearl Bio co-founder and chief operating officer Amy Cayne Schwartz in a company statement released through BusinessWire, “Pearl is able to tune half-life, target delivery to diseased cells, and attach cytotoxic payloads to tailor valuable therapeutic properties, overcoming key barriers preventing market approval.”

Pearl Bio says its synthetic proteins retain their natural protein activity, but still allow for tuning the protein chemistry to reach specific targets, maintain stability, and reduce toxicity. The company cites as examples delivery of cancer-killing proteins to tumors through the protective microenvironment, while also accessing novel therapeutic targets. Pearl Bio says it’s forming partnerships with drug makers to develop what the company calls the next generation of smart biologics. In addition, says the company, its process makes possible genetically altered organisms that can produce strings of basic components constructed into wholly new biologics and bio-based materials.

Merck & Co. has signed up to Pearl Bio’s synthetic biology platform, offering up to $1 billion in biobucks for potentially cancer-busting biologics.

The collaboration could pile more biologics onto Merck’s pipeline and serves as validation for Pearl, which emerged from stealth in June 2023 with the backing of Khosla Ventures. Merck is paying an undisclosed upfront fee and offering up to $1 billion in milestone payments for Pearl to identify biologics to treat cancer.

The biotech describes itself as creating “template-directed biomaterials with tunable properties.” Co-founder, Chief Operating Officer and Chief Business Officer Amy Cayne Schwartz elaborated in an email to Fierce Biotech, describing how the platform can “encode synthetic chemistries to tune therapeutic properties (eg half-life, drug antibody ratio.” The company is in the process of raising its series A round, she told Fierce.

“Pearl Bio is recoding life for a new era of programmable or ‘smart’ biologics,” Schwartz wrote. “Series A resources will be used over the next two years to drive molecules to the clinic and further differentiate our technology with the ability to endow three distinct functionalities with tunable properties into biologics.”

Pearl was spun out of research from Farren Isaacs, Ph.D., and Michael Jewett, Ph.D., that centers on using ”genomically recoded organisms” to add synthetic chemistry to biologics. The company counts famed molecular engineer and serial entrepreneur George Church, Ph.D., as one of its scientific advisers. In June 2023, the U.S. granted a patent to Pearl and its founders that bolsters their multifunctional biologic ambitions, cementing future use of tools like synthetic amino acids and tethered ribosomes.

As for Merck, it’s just the latest collab to land on its conveyor belt of licensing pacts. The Big Pharma’s recent slate of bets has largely focused on oncology, including deals with C4 Therapeutics and Daichii Sankyo, alongside the $680 million acquisition of Harpoon Therapeutics.

Juan Alvarez, Merck’s vice president of discovery biologics at Merck Research Labs, described Pearl in a release this morning as a “pioneer in developing recoded organisms.”

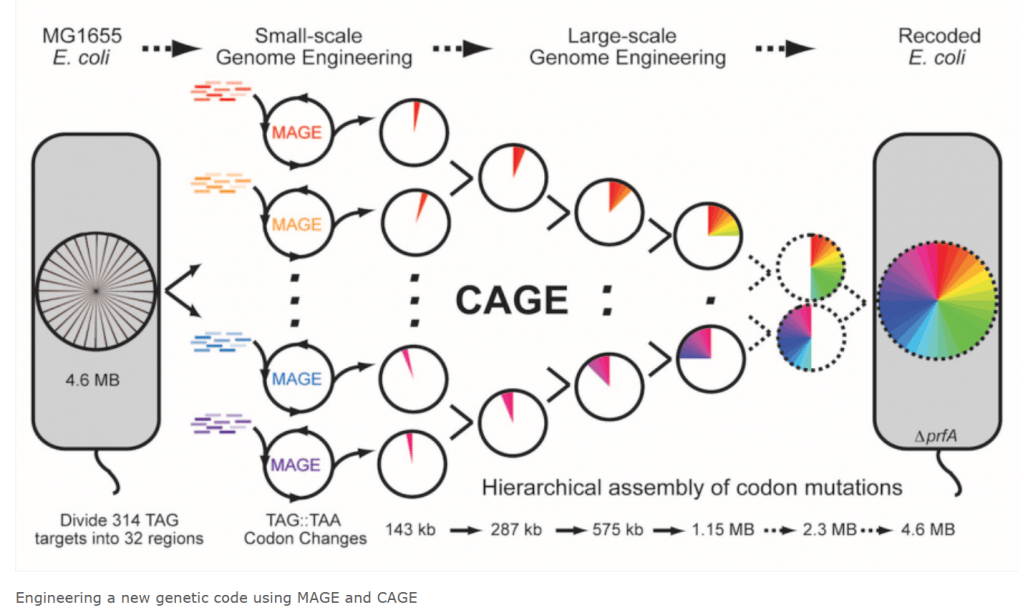

Farren Issacs Lab at Yale University 에 보여진 연구내용을 보면 MAGE (Multiplex Automated Genome Engineering)과 CAGE (Conjugative Assembly Genome Engineering) 을 통해서 Recorded E. Coli 를 만들 수 있습니다. Hierarchical assembly of codon mutations를 통해 다양한 사이트에 정확도 높은 조작을 할 수 있다는 설명입니다.

(Picture: Bruce Booth, Ph.D., Partner at Atlas Ventures)

안녕하세요 보스턴 임박사입니다.

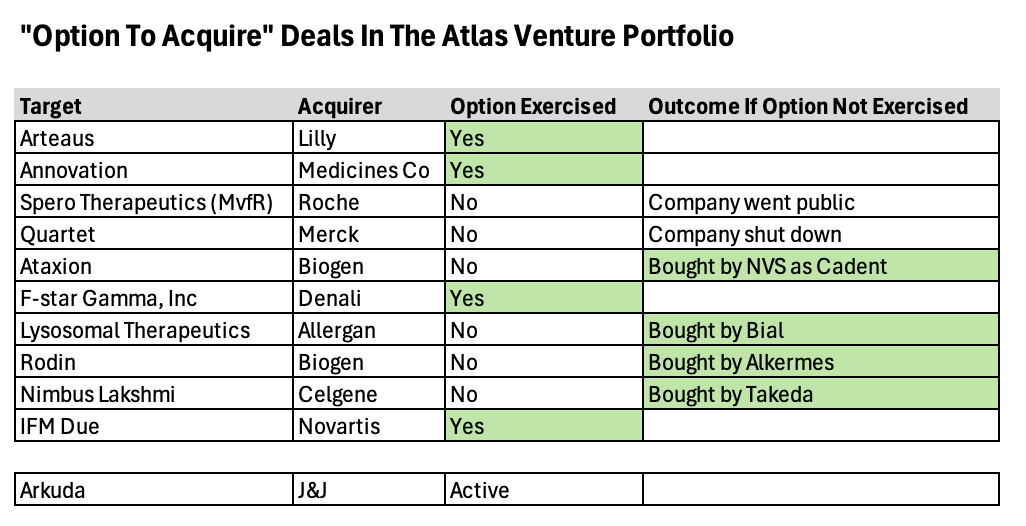

주식투자에서 Option Investing이라는 방식이 있습니다. 이 방식은 Structured Deal로서 Downside Risk를 줄이고 대신 Upside Gain도 어느 정도 포기함으로써 어려운 시장에서 살아남은 방법이라고 할 수 있는 Venture Investing Strategy 중에 하나입니다. 보스턴의 벤처캐피탈인 Atlas Ventures의 Bruce Booth 박사는 “Option-to-Buy M&A” Model을 가장 먼저 시작한 VC로 기억합니다. 2011년에 시작한 이래 아래와 같은 다양한 회사들이 이 모델에 의해 투자 회수가 되었습니다. 최근은 IPO시장이 2010년대에 비해서는 훨씬 좋은 상황이지만 언제든지 시장은 반대로 돌아설 수 있다는 생각으로 이 모델에 대해 다시 한번 생각을 해 보고자 합니다.

2007-2008년에 미국 서브프라임모기지 사태와 리먼-브라더스 사태로 시작된 글로벌 금융위기는 전세계 주식시장을 비롯한 금융시장에 오랜기간 충격을 주었는데 바이오텍의 충격은 당시 매우 심했습니다. IPO 시장은 수년간 적은 수의 기업만 가능했을 뿐만 아니라 IPO Valuation도 낮아서 당시 Venture Capital 에는 자금 회수를 할 방법이 상대적으로 어려운 실정이있습니다.

빅파마를 비롯한 바이오텍의 대량 해고가 매년 끊이지 않았던 어려운 시기였고 따라서 빅파마들의 파이프라인의 생산성도 크게 낮아지고 있었습니다. Original Drug Patent Expiry에 의한 Generic 압력은 그 어느 때보다 높았습니다. 반면 미국 대학이나 연구소에서 생산되는 기술혁신은 새로운 Drug Targets와 Platform이 태어날 기회가 되기도 했습니다.

2010년까지 미국 IPO 시장에 대한 Atlas Ventures의 블로그 글이 당시 상황을 잘 말해 줍니다. 2010년은 Nasdaq 시장지수를 반영한 바이오텍 IPO에서 전년에 비해 5% 정도 상승함으로써 그나마 선방한 해였습니다. 하지만 바이오 기업의 특성 상 나스닥 시장에서 가격이 중요한데 여전히 낮은 수준의 가격으로 벤처캐피탈의 입장이나 Crossover Investors 입장에서도 좋은 상황은 못되었던 것 같습니다.

Several recent stories from WSJ and VentureWire have highlighted the challenging performance of the IPO markets for biotech in 2011. It has indeed been tough: more shares offered at lower prices = more painful dilution. From a pricing perspective, the Class of 2010’s thirteen biotech IPOs faced similar challenges.

Surprisingly, however, the markets have been reasonably good to the 2010 class since their IPOs. Here is the price performance relative to their IPO price as of today:

The average and median performance of this “Class” is 18% and 14%, respectively – which is quite abit better than several of the recent prior classes performance. Ventrus, Aegerion, AVEO, Anacor have all appreciated by more than 30% since their IPO.

However, the NASDAQ itself has also been on a tear, up above 30% since mid-2010. To get a sense for individual company outperformance vs the market, I’ve adjusted the performance of the Class by the NASDAQ’s performance from the individual IPO dates:

The order shifts as one would expect in a bullish stock market with newer IPOs moving up in the ranking (less adjustment) and older IPOs moving down (more adjustment). Importantly, however, the class average stock performance was still up 5% after adjusting for NASDAQ market performance. That’s respectable.

From a venture standpoint, since IPOs are financings not exits, understanding the price performance relative to their last private round is important. From what I can tell, it has actually been pretty strong. Here’s a snapshot of performance of 12 of these 13 where I could get the last private round pricing (courtesy of a friendly biotech investment banker). Unfortunately I don’t have data on Ventrus Biosciences. I’ve plotted the current stock price on the Y-axis and implied “last round” pre-IPO price on the X-axis. Any ticker above the line is at least “in the money” for the last private investor (maybe or maybe not for the early investors depending on the step-ups or cramdowns along the way); below the line are “underwater” positions for that last round. Good news is most are near or above the line – with considerable outperformance for Aegerion (nearly 3x) and Complete Genomics (2x). Tengion is sadly quite an underformer – roughly 10 cents on the dollar.

The takeaway message here is that despite the ‘doom & gloom’ around biotech IPOs, there’s some glimmer of hope in the post-market performance for the “Class of 2010”.

Hopefully the pricing struggles of Class of 2011 will be forgotten with some strong stock performance ahead.

이런 어려운 금융환경 속에서 Atlas Ventures는 Bill Gates와 함께 Nimbus Discovery LLC를 만드는 새로운 시도를 합니다. Nimbus Discovery LLC는 Option-to-buy M&A Model의 선구자적 기업이라고 볼 수 있습니다. 2009년 당시 아직 비상장기업이었던 Schrödinger라는 Computation drug discovery company가 있었는데 Bill Gates도 이 회사의 대주주 중 한명이었습니다. 당시 Schrödinger가 WaterMap이라는 In silico SAR Model을 개발했는데 이를 이용해서 Global Virtual Biotech을 만드는 실험을 한 것입니다.

Nimbus Discovery LLC는 Virtual Biotech Model을 Computational Drug Discovery에 연결한 방식이었습니다. 2009년부터 2010년까지 1년간 인더스트리의 백여개 표적을 조사하고 그 중에서 가장 경쟁력이 있다고 판단하는 십여개의 표적에 집중해서 Project 단위별 C-Corp를 만들고 IP를 각 회사에 집중시키는 방식이었습니다. Schrödinger의 60명의 박사들이 참여하고 해외 CRO들이 합성, Biology, DMPK 등을 하는 방식으로 해서 실제로 Nimbus의 인력은 필요 인력의 10-15분의 일에 지나지 않게 만든 것입니다.

Bill Gates has just backed one our new startups – Nimbus Discovery LLC – as part of an extension to the seed tranche. Here’s the press release.

It might come as a surprise to some, but Bill Gates has been a long-time biotech supporter: he was a founding investor in ICOS and was on that Board for 15 years, and importantly, he’s also one of the largest investors in Schrödinger, the world’s leading computation drug discovery company, and our founding partner with Nimbus.

So, with this financing, we’re launching Nimbus out of ‘stealth mode’. Here’s the story.

We founded Nimbus Discovery in 2009 with Schrödinger and have incubated the company here at Atlas for the past couple years. It’s fair to say Nimbus is a rather unconventional biotech, possessing three distinctive features.

Unique Drug Discovery Partnership with Schrödinger provides access to an unparalleled technology suite without the financial burden of having to build it organically. Beyond the sheer breadth of Schrodinger’s software offerings, the crown jewel from our perspective is their new technology for evaluating the energetics of specific water molecules in binding sites called WaterMap™.

Our bodies are 90+% water and yet most structure-based drug design models fail to integrate proper solvent (water) effects with regards to both entropy and enthalpy. WaterMap™ does this. We’ve already found it to be an incredibly powerful tool for identifying specific optimization strategies based on novel water-energy-driven Structure-Activity-Relationships. WaterMap™ is a incredibly well validated technology and has been applied (retrospectively) to about 45 different targets using ligands that have highly heterogenous structures. Not only does WaterMap™ accurately predict binding affinities, it explains SAR that would otherwise be inexplicable. In short, super cool science at the cutting edge of in silico drug discovery.

Our partnership with Schrödinger provides us with far more than just this software package though – we get a large number of dedicated computational chemists, access to thousands of processors via their cloud computing network, new unreleased software algorithms, and exclusivity around specific targets. Continuous, advanced access to the most cutting edge technology applied in a personalized way to our targets allows Nimbus to maintain its first mover advantage.

Moreover, Schrodinger continues to make a huge investment in its platform leveraging an army of ~60+ PhDs and the deep-pocketed support of Bill Gates and David Shaw. (As an aside, it’s probably the only biotech with two billionaires as its top two investors). It is no surprise that Schrodinger has led innovation in the field: the company currently has 50+ peer reviewed publications many of which are among the most heavily cited articles in the in silico modeling space.

Ultra-lean “virtually integrated, globally distributed” R&D operating model to aim for exquisite capital efficiency. We’re really pushing the envelope on virtual drug discovery. We have 10-15x more FTEs working for the company externally as inside the company.

The core team is two incredible individuals (Rosana Kapeller and Jonathan Montagu) who, in addition to being very smart seasoned biotech startup veterans, excel at integrating remote workstreams and collaborators. We’ve got several teams at offshore CRO partners doing biology, chemistry, crystallography, in vivo work, etc…. Not to mention a core set of KOL academic collaborators. We think we’ll be able to work on 3-4 programs with this setup.

It’s paying dividends already: on less than $2M spent, we’ve generated a selective, potent IRAK4 inhibitor (cancer, inflamm) and a set of lead scaffolds against other targets.

One of the key features of the operating model is the virtual integration of all these pieces, with in silico model refinement in the core of the ‘engine room’ so to speak. WaterMap and tools like it depend on constant structural model enhancement, which requires real time integration of project data into our models. Our remote virtual teams interact on almost a daily basis to integrate these new streams of information. This allows us to use these tools for more than just improving selectivity and potency – but also to more precisely know which part of molecules to optimize for PK/ADME concerns as well.

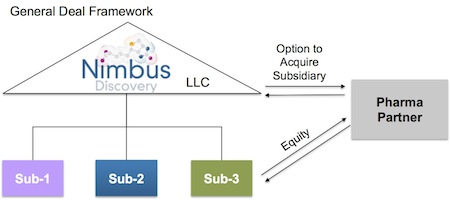

Novel asset-centric corporate structure to promote liquidity and capital velocity. Back in 2009 we spent a lot of time figuring out how to leave the limitations of the traditional C-corp structure behind and adopt a more flexible LLC-holding company structure with target-specific subsidiaries as C-corps. A few companies have recently announced they are doing this as well, like Adimab and Ablexis. This structure does a couple very valuable things (beyond creating a job for accountants to track the project financing).

First, it enables project-driven ‘clean’ transactions with Pharma, such that a Pharma can just acquire the target-specific subsidiary and own the IP/assets of a particular program if it so chooses.

Second, and importantly, it solves the classic drug discovery illiquidity problem (where it takes 7-10 years to get liquid via M&A or IPO); this LLC structure enables us as shareholders to cycle capital back to our investors in a tax-efficient manner on a per project basis. Furthermore, it creates this type of ‘deal optionality’ without foregoing any of the traditional benefits of C-corps.

At the end of the day these three elements are great value enablers, but ultimately it’s about the medicines we discover. To pick the targets we sought to generate drugs against, we took an orthogonal approach to traditional “biology” driven target selection. History has shown that generally in silico technologies in drug discovery are helpful tools for the vast majority of targets, but not game-changing. With Nimbus, we wanted to let the technology identify targets where its new insight into SAR was potentially transformational rather than incremental – essentially, to find the rare 10% of targets where these technologies offered a compelling path to new, differentiated chemical matter against hot targets. To accomplish this, we spent the first 12 months of the company screening several hundred ‘hot targets’ in the industry’ pipeline before picking the 10% or so to focus on with Schrödinger.

Our two lead programs today:

IRAK4. One of the most interesting immune-kinase targets in both B-cell cancers (like the IRAK4-dependent MyD88-driven Activated Diffuse B-cell lymphoma and inflammation. It’s traditionally been very challenging to get selectivity and cellular potency; we’ve managed to generate a series that addresses both of those and aim for a development candidate by end of 2011.

ACC or Acetyl-CoA Carboxylase. A critical enzyme in the metabolism of lipids and a top target for obesity as well as cancer metabolism. It’s been very hard to drug effectively. We’ve managed to get very interesting leads against a unique allosteric domain that should enable a differentiated profile.

Saving the best for last, it’s fair to say our team is exceptional. Rosana Kapeller is our CSO and was founder of Aileron Therapeutics after nearly a decade at Millenium. Jonathan Montagu is our CBO and was with Concert, J&J, Chiron and BCG. The broader team of folks at Schrodinger, like Ramy Farid (President of Schrodinger and founding Board Director of Nimbus), and our chemistry leadership (Ron Wester, Gerry Harriman, Donna Romero, John McCall) are also incredible.

With that rundown, we’re officially out of stealth mode and aiming to close on a Series A soon. Exciting times.

Nimbus의 Series A를 한지 2년 후 (창업 후 4년 후) 이 모델에 대한 블로그 포스팅이 있었는데 당시는 ACC 프로그램이 DC selection을 한 상태였습니다. Investor 입장에서 Platform Company인 Nimbus Discovery LLC는 영원히 운영되고 자회사들만이 독자적으로 생존하며 매각되는 조건의 구조였습니다.

A couple years ago we unveiled a new startup called Nimbus Discovery LLC which was experimenting with a new model that combined three key elements: Schrodinger’s cutting edge in silico drug screening and design platform, a truly virtual and globally distributed operating model for drug discovery, and an asset-centric LLC-based corporate structure (discussed here).

Although it’s too early to tell what eventual value will be created from this experiment, the company’s early biomarkers are strongly positive. Nimbus has cracked two very tough-to-drug targets of high interest to Pharma (immunokinase IRAK4 and lipid-pathway regulator ACC), and is entering IND-enabling development this year. The technology and virtual operating model have worked well together in efficiently delivering high quality drug candidates.

Importantly, the market validation of the model has also been positive: today Nimbus announced a deal with Monsanto, and last month announced a similar deal with Shire – both involve collaborative drug discovery with a pre-defined path to liquidity around those projects. Given the unique nature of the deals, I thought it would be worth sharing more details and a few general reflections on the model.

Both deals are structured to take advantage of the Nimbus asset-centric approach: they involve equity or equity-like investments in individual R&D programs housed in standalone subsidiaries, alongside an option to acquire those subsidiaries at a specific milestone with pre-negotiated deal economics. These are very enabling for Nimbus: project-based resourcing to support the prosecution of a pipeline with clear value creation points defined at the outset without the need for dilutive funding at the parent LLC level.

These collaborative deals were born out of close relationships Atlas has with both Monsanto and Shire. Over the past few years, both companies have been able to watch Nimbus deliver against its existing programs, in particular for ACC, IRAK4, Tyk2. Here’s the short promotional on their programs’ progress On ACC, it took Nimbus only 16 months from standing start with a virtual screen to get to a fully characterized Development Candidate (DC) with a first-in-class allosteric regulator of the target; for IRAK4, the team has discovered truly selective inhibitors with potent in vivo activity and DC-like profiles; and lastly, they have cracked the Tyk2 selectivity challenge vs closely homologous JAK2 and other JAK family members. The progress of these case studies and the familiarity they had with our team definitely facilitated both transactions. More evidence for why tighter collaborative Pharma/Venture relationships are value-creating.

The bigger picture: why these deal structures make sense

For the biotech, these deals help build a portfolio comprising multiple program-focused entities under an LLC umbrella. In some respects, the pipeline becomes a collection of call options on individual paths of potential liquidity.

For Pharma, these structures can be tailored to the requirements and sensitivities of each partner, in many cases enabling what could be described as a P&L-sparing, “balance sheet supported” portfolio of innovative projects. This may not always be the interest of a partner, but accessing the otherwise inaccessible cash on the balance sheets of Big Pharma is a definite positive for these deal structures.

For shareholders, including investors and team members, this model secures potential routes to liquidity that accrue as programs are progressed and monetized through development – importantly without having to sell the entire company. In essence this model creates the evergreen drug discovery stage biotech – a real unicorn in the history of biotech (because most drug discovery biotechs have to either sell or become later stage development players to achieve liquidity).

Lastly, the structure has enormous financing flexibility: any individual subsidiary/program can be financed separately if desired – creating options for going longer on specific programs without diluting the parent platform company (or for a new investor, without having to fund drug discovery if that’s not their interest).

Nimbus certainly anticipates doing more of these types of structured transactions, both for its lead programs (IRAK4, ACC, Tyk2) and de novo collaborations around jointly-identified targets. Several of our other platform-based drug discovery companies, like RaNA Therapeutics, are structured in this way and will likely be pursuing deals of this type. Other drug discovery platform biotechs, like Forma and Viamet, have also been experimenting with versions of this LLC-holding company model. Several subsidiary-level deals have been done across the industry (like Forma-Genentech, among others). To my knowledge, none of these have yet to hit their acquisition-triggering milestones. It will be exciting to see what happens when this crop of deals matures to their pre-defined endpoints.

Creatively thinking about new approaches, new business models is part of innovating around the venture model – some experiments will work, some won’t. But the Nimbus experiment feels pretty good right now.

그로부터 10년이 흐른 후 Atlas Ventures의 Jeb Keiper가 14년간의 Nimbus Discovery LLC Model에 대한 이야기를 잘 정리해 주었습니다. 3개의 Chapter로 구성이 된 “The Book of Nimbus”라는 책입니다.

Nimbus Therapeutics began 14 years ago. The premise at the time was that putting computational chemistry in the primary position for new molecule ideation would upend the drug discovery paradigm. It did just that. Three best-in-class molecules in the clinic, over $400 million invested and over $4 billion returned to equity holders, all while focused on our mission to design breakthrough medicines for patients.

Fourteen years on, this corporate experiment has gone far beyond the initial idea, and has established an R&D engine more effective than most big pharma R&D groups at producing best-in-class small molecules against targets that matter in human disease biology. Throughout that time Nimbus has not just built functional capabilities and continued adopting technological innovation, but importantly has worked tirelessly to establish strong cross-functional and interdisciplinary ties that bind discovery and development into a more cohesive, more effective R&D engine. Much of our success springs from being nimble and pragmatic on the journey: by optimizing areas we know work well and adapting to ever-changing landscapes in the capital markets, therapeutics spaces, and laws and regulations (e.g., IRA).

The Book of Nimbus is still being written, but its arc over the years already shows the shape of what I believe to be Nimbus’ mark on our industry: as an R&D powerhouse with the potential to repeatedly create breakthrough medicines for patients.

1장은 2009년부터 2016년까지 7년간의 이야기입니다. Atlas Ventures의 Bruce Booth와 Schrödinger Ramy Farid 사이의 대화로 시작된 말도 안되는 아이디어 – “2년간 $10 Million을 투자해서 5개의 프로그램을 DC 단계까지 만든다”는 터무니없는 아이디어로 시작합니다. 이 아이디어는 5년에 하나의 DC로 수정되었고 투자금액은 $50 Million으로 올라갔습니다.

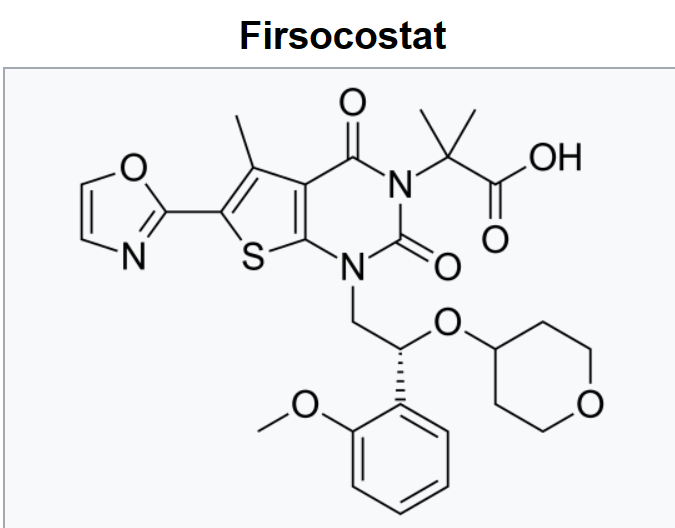

ACC Inhibitor인 Firsocostat이 Gilead에 팔렸고 MASH 치료제로 개발 중입니다.

Chapter 1 – An Unreasonable Idea

The year was 2009. Barack Obama had just been sworn in as the 44th president. The automotive industry just received an $81 billion bailout from the federal government, and unemployment sat at 10% (the highest in 25 years). Michael Jackson died, Slumdog Millionaire won the Oscar for Best Picture, and meanwhile Bruce Booth of Atlas Venture and Ramy Farid, CEO of Schrödinger, began work on a very unreasonable idea. It was the beginnings of Project Troubled Water, Inc.: set up a “virtual project team,” leverage Schrödinger scientists to lead computational chemistry, and do all the wet work at CROs. Invest $10 million to get 5 development candidates in 2 years. Unreasonable indeed.

The five development candidates in two years became one development candidate in five years. The cost went from $10 million to $50 million, inclusive of investments in the platform and broader pipeline. In those respects, one might look at Nimbus’ first chapter as a failure, but they’d be wrong. Because the other thing that happened was the creation of an incredible discovery engine that entirely changed the small molecule drug discovery paradigm. Those years of hard work forged the unique project style that coupled computational chemistry leadership with battle-tested medicinal chemists, biologists who are subject matter experts on the target, and CROs and academic collaborators that fueled an unprecedented “DMTA” engine: Design a molecule on a computer, Make the molecule at a CRO, Test the molecule in a proprietary bespoke biological screening cascade for the target, and Analyze the resulting data, which would then feed the design phase of the next iteration. Blood, sweat, and tears poured into the establishment and optimization of this framework. High science led the vanguard of the work, yet behind the scenes a novel business structure was developed simultaneously, the LLC structure. The LLC structure at Nimbus is more than just a holding company framework; it is an intricate, well-planned set of agreements, accounting methods, and governance operations procedures that allowed the Nimbus discovery engine to flourish. Long-time Nimbi extraordinaire Holly Whittemore perfected this approach alongside the amazing counsel at Goodwin, notably Bill Collins, Mitch Bloom, Dan Karelitz, and many others.

By the time Chapter 1 was nearing its end, Project Troubled Water, then Nimbus Discovery, became Nimbus Therapeutics as we took a further step to forward integrate into clinical development. Having partnered our lead IRAK4 asset with Genentech (which ultimately failed to progress), Nimbus entered the clinic with our allosteric inhibitor of acetyl-CoA carboxylase (ACC) in healthy volunteers, with plans to begin a Phase 2 in NASH. Our ACC inhibitor, now named firsocostat, remains first-in-class, and is in a Phase 2b study in severe NASH patients run by Gilead, who acquired the program in 2016.

For further reading about Nimbus’ first chapter, many an excellent blog has been written about those formative days. Check out:

2장은 2016년부터 2022년까지 6년간의 이야기입니다. Fircocostat을 Gilead에 매각한 후 회사의 미래에 대한 논의가 있었고 BD를 통해 2017년 Celgene과 Tyk2와 STING program에 대한 Option deal을 합니다. 그런데 2019년초에 BMS가 Celgene을 합병하면서 Tyk2 프로그램에 위기가 옵니다. BMS는 Nimbus의 Tyk2 program을 back-up으로 가져갔고 BMS가 가진 Tyk2 Inhibitor인 Sotyktu Deucravacitinib) 이 승인이 나면서 Nimbus의 Allosteric Tyk2 product는 Psoriasis 치료제로 선회하게 됩니다.

Phase-3 data package를 가지고 빅파마 들과 딜을 한 결과 Takeda에 매각됩니다.

Chapter 2 – Building an Integrated Approach

It was 2016, we had sold our lead asset to Gilead, and we had no idea what exactly was going to happen next. The transaction in 2016 was also the first true biotech “exit” of a holding company/single asset that would return capital to investors and employees – like a true M&A – but preserve the rest of the portfolio and the Nimbus business model. Miraculously, everyone came back to work the next day, week, month, and it truly felt like a new adventure as we knew we were charting a course not many previously had. The transition had its challenges though: we had begun working in clinical development, hired staff, and now were reset to an early-stage preclinical company. All our resources in chapter 1 had begun funneling to the lead program, and with only $67 million raised over 7 years, Nimbus was not exactly “robust” at an enterprise-level. We had just 22 people by the end of that year, 15% of the company having departed following the Gilead deal.

At that time the Nimbus Board discussed the next chapter of our company. The first thought was to never raise money again; become a perpetual motion machine. We kept 5% of the Gilead deal proceeds in 2016 in the hopes we could span our way to a next BD deal in our pipeline – and we did! In 2017 we formed a classic Celgene option deal with our two most advanced programs, TYK2 and STING. Nimbus retained full ownership and control of the programs in exchange for funding and pre-programmed exits of $400 million each for Phase 1b data in a few years.

That created a conundrum. With the two lead programs effectively pre-sold, what would the rest of Nimbus do? Would we wind down and exit, or chart some different path? That critical strategic discussion led to some fundamental changes in Nimbus, changes that ultimately laid the groundwork for amazing success in chapter 2.

The year was 2018, and the Board at Nimbus had agreed with our plan to re-invest in discovery and build out our internal pipeline. The successful computational powerhouse DMTA cycle we had built could broaden applications across more targets. And in that new pipeline, our goal was to identify “The One” (I personally cannot help but think of Keanu Reeves’ character Neo, from the Matrix movies). “The One” was a molecule that we would forward-integrate further around, which would be the nucleus to crystallize our clinical development organization. The strategic shift spawned our mission statement at Nimbus: We design breakthrough medicines. It also led to a $65 million equity financing to kickstart pipeline creation. Little did we know that “The One” would be a molecule we already had in our hands, our allosteric TYK2 inhibitor….

This direction and change in strategy fomented uncertainty, which led to inevitable turnover. Nine years in at that point, we saw 25% of the Nimbi depart that year, including our first CEO, Don Nicholson, and I am humbled the Board asked me to step in as Nimbus’ next CEO. Having said farewell earlier to our founding CSO, Rosana Kapeller, my first step was to rebuild the fundamental high science foundation of the company. I turned to my good friend and former colleague, Peter Tummino, then VP, Global Head of Lead Discovery at Janssen, to be our next CSO. Over the next four years, the science at Nimbus flourished, and with it, the reputation for excellence grew. We became the magnet for top talent that Nimbus is now known for, attracting such amazing scientists as Christine Loh, Scott Edmondson, Mark Cartwright, and so many more, too many to name, but all of whom deserve my most humble thanks for joining on this mission to design breakthrough medicines for patients.

In the middle of chapter 2, the most dramatic wrinkle then occurred. It was January 3rd, 2019, and BMS just announced that they were acquiring Celgene. I remember learning of this from Holly Whittemore, as I cheerfully greeted her with “Happy New Year” on my first day back to the office. She replied, “Hey, did you see this?” and swiveled her monitor to show me the news. After I picked my lower jaw up off the floor, I said 30 seconds later “We are going to keep our TYK2 program.” Celgene had signed up for the option deal with Nimbus in 2017 to access our (hoped-for at the time) best-in-class allosteric TYK2 inhibitor to compete with their rival BMS’ TYK2 inhibitor (which today is known as Sotyktu). BMS had just begun Phase 3 trials of their agent, which was likely to be successful — as we now know it was.

The initial interactions with BMS were pragmatic and sensible. Following the close of the BMS deal, the Nimbus TYK2 option was allowed to persist as a backup option, should the BMS TYK2 drug fail in Phase 3. During the year-of-Covid, 2020, we slowly started our Phase 1 program with our TYK2 candidate while BMS slogged through Phase 3. Then came 2021, the most consequential, and tumultuous, year in the Book of Nimbus thus far. It was a period of dramatic activity, much of it well-documented in the public domain, but thankfully all resolved by January of 2022. In the end, after a rollercoaster of legal ups and downs, we settled out of court, leaving Nimbus sole ownership of its TYK2 program.

Throughout this period of interacting with BMS, litigation attorneys, and the FTC, Nimbus was fortunate to find investors who believed in our team, our science, and our conviction that we had a sound strategy that did not rely on a binary outcome of whether we won or lost litigation. We were fortunate to raise $225 million to power TYK2, as well as the rest of our pipeline, including the clinical start of our HPK1 inhibitor program in cancer patients. That funding enabled the two Phase 2b trials of our TYK2 program, one in psoriasis and one in psoriatic arthritis.

In 2022, with sole ownership of our lead asset, Nimbus began seriously considering an initial public offering after 13 years of private operation. Our CFO, Ian Sanderson, had joined to lead us through that transition, and instead his experience and expertise led us through finding private funding at the start of a very turbulent period in the public capital markets. By mid-summer 2022, the market sentiment was downright sour, and Nimbus was running low on the cash needed to power up our programs. In true Nimbus fashion, we did continue to keep all our options on the table, and the BD team at Nimbus had been in constant communication since 2019 with all key pharma partners that would entertain talks about our TYK2 program. Our Phase 2b study was wrapping up and we expected data in Q4; meanwhile, on every investor’s mind was the expected approval of BMS’ TYK2 inhibitor in September. Nearly 90% of investors and physicians had predicted that BMS would get a black box warning on Sotyktu, since TYK2 was a JAK family member, even though Sotyktu was super selective against the other JAKs. When the approval finally arrived at 11pm on the PDUFA date with no black box, suddenly, allosteric TYK2s were a new class of medicines for psoriasis with potential in many autoimmune diseases.

Shortly after the Sotyktu approval, our 260 patient Phase 2b study read out. The data, ultimately unveiled at AAD in March 2023, were stunning: biological efficacy rivaling IL-17 and IL-23 with an oral small molecule, and possessing a safety profile at least as benign as BMS’ Sotyktu. Our long-time clinical development lead, Bhaskar Srivastava, an M.D. Ph.D. dermatologist, could not contain his excitement. He delivered one of the most well designed and executed studies in the field and deserves enormous credit for developing a medicine with such profound potential for so many patients.

In the frenetic weeks that followed the unblinding of the study, our Chief Business Officer, Abbas Kazimi, was on center stage, building a team including the excellent advice of Phil Ross at J.P. Morgan and wise counsel of Sarah Solomon at Goodwin. The pharma relationships Nimbus had established allowed diligence teams to engage efficiently and move past the first point of an interaction – trust. Our small team was able to support multiple major pharmaceutical companies plowing through diligence, not just withstanding the onslaught but in fact delivering a data package of Phase 3-ready quality. The bidding was fast and furious, and ultimately the incredible team at Takeda, led by CEO Christoph Weber and R&D Head Andy Plump, became the most compelling group dedicated to taking our program forward to patients, which we announced on December 13, 2022. We could not be more thrilled with their leadership and commitment, and we closed the deal by February of 2023.

For further reading about Nimbus’ second chapter, many excellent blogs were written about this period. Check out:

2023년 이후 Nimbus는 3장을 쓰기 시작했습니다. 새로운 Breakthrough Medicine을 개발한다는 계획입니다. 구조조정이 있었고 Oncology와 Immunology Programs를 개발하고 있습니다.

Chapter 3 – Establishing a Legacy R&D Institution

This blog is being written as we turn the page to chapter 3, however the groundwork began with long-range planning almost a year ago. We had scenarios for every eventuality for the TYK2 data, partnering interest, and the financing environment. With that said, we knew if we were successful in psoriasis, the implications would require a large multinational company to create the value of global registrations in multiple indications. Given the value of established infrastructure in pharma, it was clear that an M&A acquisition of our TYK2 subsidiary was likely.

We therefore have had some time in which to contemplate what this next act for Nimbus holds. Although we are just now at the beginning stages of the great journey to come over the coming years, many of the formative pieces are now in place — just as our TYK2 program was at the time of Nimbus’ last inflection point. Our clinical-stage HPK1 inhibitor is now progressing into expansion trials in solid tumors, while a crafted pipeline of opportunities, including what we would consider a disruptive medicine in the autoimmune field, heads toward the clinic next year. While our expertise in immunology and oncology is strong, we also have depth in metabolic disorders, and have a fabulous collaboration with Eli Lilly on AMPK activators, along with earlier programs in discovery.

And excitingly, we are better positioned than at any point in our history to navigate what comes next. Our investments throughout chapter 2 have built an organization with an even wider skillset, from discovery through to clinical execution, and deeper disease area expertise than ever before. Key to Nimbus’ third chapter will be Chief Medical Officer Nathalie Franchimont, who joined us from Biogen late last year to lead our Development organization, building upon our foundations of quality, operations, and execution. Nathalie, Peter Tummino and Bhaskar Srivastava are building out our early clinical and translational biology expertise, while at the same time we are investing in our computational capabilities, tackling tough targets like transmembrane GPCRs in our discovery pipeline. As the winds of change in our industry keep blowing strong, the flexibility and optionality of the Nimbus structure remain a key competitive advantage that has contributed to this enterprise’s longevity.