Internet의 세상에서 가장 흥미롭고 즐거운 일은 세계 곳곳을 방문하지 않아도 다른 사람들의 생각을 읽을 수 있는 Blog나 Youtube 등이 있다는 것입니다. 모두 다 좋은 블로거나 유튜버가 아닌 것이 꾸준히 10년 이상 그 일을 묵묵히 해야 비로소 진가를 드러내는 사이버 세상에서 만나게 되는 이런 꾸준한 블로거들과 유튜버들을 만나면 참 반갑죠.

오늘 소개할 분은 “배당주 투자 (Dividend Investing)”나 FIRE Movement를 말하는 한국 블로거나 유튜버들에게 많이 알려진 분입니다.

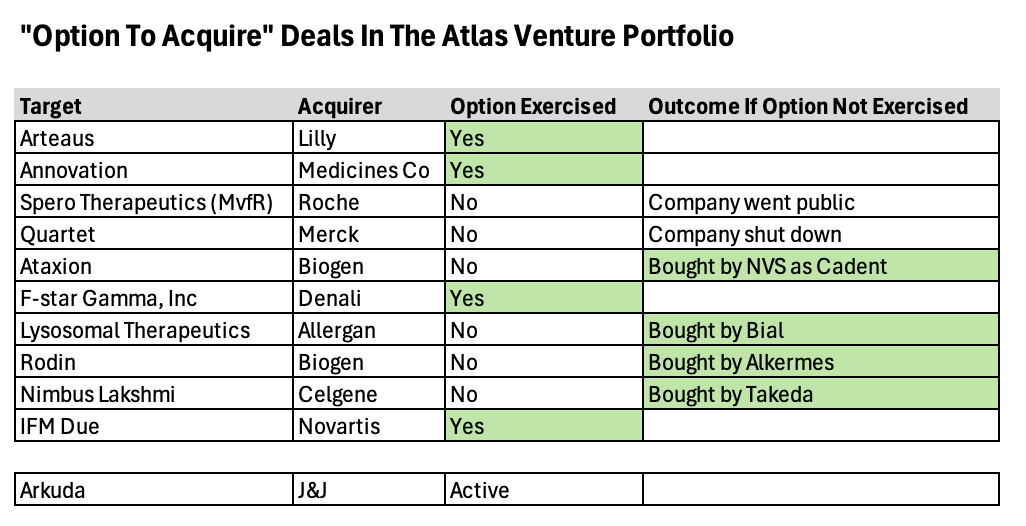

Bob Lai는 캐나다 뱅쿠버에서 두자녀를 포함한 4인가족으로 살고 있고 Hi-Tech에서 일하는 대만계 캐나다인입니다. 그는 아내와 함께 글로벌 금융위기 시기인 2011년부터 배당주 투자를 시작해서 지금까지 13년간 지속적으로 투자했습니다. 그의 투자기록을 남기기 위해 블로그를 2014년부터 쓰기 시작해서 블로거로서도 10년이 되었죠.

2023년에는 $3,600/month를 배당주 투자로 이루었고 2024년부터는 >$4,500/month를 배당으로 벌고 있으며 2025년에 배당만으로도 >100% 생활비를 벌게되어 경제적 자유를 이룰 수 있을것 같다고 했습니다.

I started this blog to show it is possible to achieve financial independence as a single-income family with two young kids while living in Vancouver Canada, one of the most expensive cities in the world. My wife and I started building our dividend portfolio in 2011 after a financial epiphany. Today, the portfolio generates over $4,500 in dividends per month. Our dream is to become financially independent and live off dividends by 2025. (Source: https://www.tawcan.com/)

Bob Lai의 이야기를 들어볼까요? 작년에 2차례에 걸쳐서 인터뷰한 것이 있습니다.

Bob Lai가 블로그를 통해 몇년 전에 알게된 익명의 투자자 “Canadian Reader B”에 대한 이야기를 소개한 글이 있는데, 굉장히 특이합니다. 익명의 Reader B는 2004년에 55세의 나이로 배당주 투자수익만으로 은퇴를 한 분입니다. 그러니까 지금은 75세가 되었겠죠. 그는 엔지니어였고 아내는 사무직이었으며 두사람 합산 소득은 약 $200,000 (2억 6천만원) 이었다고 합니다.

그가 처음에는 $10,000을 배당주에 투자하기 시작해서 2021년 4월 기준으로 $360,000/year (4억6천만원)을 매년 배당으로 벌고 있다고 합니다. 뿐만 아니라 세금도 거의 내지 않고 있다고 하는군요. 이렇게 배당주 투자자가 된지도 이제 36년이 되었다고 합니다. 그러니까 1985년 (36세) 에 주식투자를 시작해서 1990년 (41세) 에 뉴스레터를 통해 배당주 투자에 대해 알게 되고 배당주 투자를 시작해서 2004년 (55세)에 은퇴를 한 것이죠.

“장기적으로 세금을 적게 내려면 401(k), IRA보다는 주식계좌에 배당주를 사서 장기보유하라는 것입니다. (The most optimum way to achieve tax-efficiency under such conditions is to focus on buying and holding Canadian dividend paying stocks in non-registered accounts.)”

Reader B가 자신의 계좌에서 4.2%를 인출한다고 했는데요. 이 말에 의하면 그의 배당주 가치는 2021년 4월 기준 $8.5 Million (110억원) 입니다. 그의 배당주 투자원칙은 다음과 같습니다.

“캐나다 주식 중 실적이 좋은 배당주에 투자를 매년 늘리고 절대 팔지 않는 것입니다. (To buy gradually over time, high-quality Canadian tax-efficient dividend paying stocks and hold them indefinitely.)”

그가 투자한 주식은 “방어주이면서 시가총액 높은 주식 (Conservative large cap stocks) – 배당귀족주”을 $10,000씩 투자하는 것이었습니다. 배당률이 2% 이상되어야 투자를 했습니다. 2% 이상 배당률을 고수했지만 너무 높은 배당률도 피했습니다. 배당컷 가능성이 있기 때문입니다. 만약 배당컷이 있으면 반드시 팔고 더 안정적인 배당성장주를 투자했습니다.

TSX60에 있는 Dividend Aristocrats에 투자를 한 것입니다. 그는 미국회사나 어떤 외국기업에 투자하지 않고 캐나다 회사에만 투자를 했습니다.

REITs 투자도 했는데 캐나다의 세금문제 때문에 Tax-efficient account에서 REITS 투자를 했다고 합니다.

직장생활을 하는 동안에 회사는 임직원들에게 다양한 혜택을 주며 최대한 일을 열심히 할 수 있도록 독려합니다. 하지만 또 한편으로는 언제든지 회사가 어려울 때 아니면 임직원이 필요하다고 느끼지 않을 때 내보낼 가능성이 상존하죠. 미국회사에는 고용계약서에 “at-will termination”이라는 문구를 반드시 넣습니다. 이 문구를 이용해서 언제든지 Layoff (정리해고)를 할 명분이 있고 임직원의 입장에서도 언제든지 자신이 그만두거나 다른 회사로 옮기고 싶다면 퇴사할 수 있습니다. 다만 퇴사할 때에는 통상적으로 2주 미리 알려서 업무인수인계에 차질이 없게 하는 것이 도의적인 룰입니다. 회사가 정리해고를 할 경우에도 많은 경우에는 바로 그날 당장 통보하고 나가라고 하지만 어떤 경우에는 몇주 혹은 몇달 미리 알려주어서 준비를 시키는 경우도 있습니다. 제가 지난 회사가 M&A 되어서 정리해고 될 당시가 그랬는데 저는 당시 2주 Notice를 받고 퇴사를 했습니다.

미국에는 사실 정년 (停年) 이라는 개념이 없습니다. 한국처럼 “60세 정년이면 정년퇴임 혹은 정년퇴직” 이런 개념이 없는거죠. 물론 미국 소셜연금 (Social Security Benefit)을 받을 때 몇세에 자신이 받을 수 있는 연금의 100%를 받느냐를 의미하는 “Full Retirement Age (FRA)”라는 개념이 있기는 합니다. 현재는 67세가 FRA에 해당되어서 만약 62세에 소셜연금을 받으면 70% 정도를 받고 반대로 70세에 소셜연금을 받으면 124%를 받게 됩니다. 하지만 그렇다해서 67세가 정년 (停年) 이라는 뜻은 아닙니다. 주위에도 이 나이를 지나서 일하는 분이 있습니다. 한국의 임금피크제나 일본의 시니어사원제도 같이 특정 나이에 이르면 연봉이 깍이는 것도 없습니다. 연공서열제로 연봉을 채택하는 것이 아니라 철저히 성과와 직무 위주의 연봉제를 택하기 때문에 자신의 가치에 따라 연봉이 오르기도 하고 내리기도 할 뿐 단지 나이가 많아는 이유만으로 연봉을 일괄적으로 깍는다면 미국에서는 바로 소송감입니다. 미국법이 보호하는 “Age Discrimination (나이 차별)” 조항에 걸리기 때문입니다.

그래도 나이가 들면서 “언제까지 일하는게 좋은가?”는 저의 오랜 화두이다 보니 몇년 전부터는 가족들과 이 주제로 자주 얘기하곤 합니다. 아이들은 “은퇴를 하고 아빠의 삶을 즐기세요!” 라고 하고 아내는 “되도록이면 회사를 그냥 다니세요!” 하는 얘기를 듣곤 하지요.

화두를 바꾸어서 언제 그만두느냐 말고 “언제 그만두든지간에 회사를 다니는 동안에 직장생활의 혜택을 어떻게 얼마나 최대로 누리느냐?”에 대해 한번 생각을 해 보려고 합니다. 두사람의 의견을 먼저 청취해 보고자 합니다.

경매투자 – 보통 소득까지 생기는데 5년이상 걸린다. 즉, 축적의 시간이 필요하기 때문에 직장생활 기간 중에 시작해야 한다.

투자소득: 투자활동으로 버는 돈 – 부를 통해 당당함을 가질 수 있다 (경제적 자유)

신수정님의 말씀을 경청해 보면 직장생활의 혜택을 활용하는 것은 결국 회사에 올인하는 것이 아니라 (1) 직장생활에 충실하면서 (2) 부캐로 소득을 얻을 수 있는 준비를 시작하고 (3) 투자활동을 해서 부를 늘여 나가는 것 – 이라는 세가지로 결론을 낼 수 있습니다. 신수정님은 현직에 계시기 때문에 이렇게 말씀하실 수 있는 것일 수도 있습니다.

두번째 소개할 분은 김상진 작가라는 분인데 대기업에서 임원으로 계시다가 해직되신 분이십니다. 강제퇴직 당하다 보니 좀더 현실적인 (?) 말씀을 하시는 것 같습니다. 김상진님은 평생 4번의 퇴직을 하신 특이한 경력이 있으신데 3번은 자진퇴사였고 한번은 강제퇴직이었는데 마지막이 강제퇴직이었습니다.

가장 후회스러운 것이 주제입니다.

주인의식을 가졌던 것: “주인이 아니다!” 주인처럼 일하다 보니 강제퇴직 후 허탈감, 분노, 억울함이 컸다.

더하고 싶은 욕심이 있었지만 회사는 그렇지 않았던 것이다. 타인에 의한 퇴사여서 받아들이기 힘들었다.

회사에서 높은 직위에 오르면 노후가 준비된다고 생각했는데 잘못된 생각이었다.

나의 미래를 위해 투자했어야 한다: 회사에 대한 열정을 제2의 인생을 준비하는데 썼다면 어땠을까?

회사 다닐 때 공부를 했어야 한다. 대학원을 다녀서 지식을 축적하고 도움을 주자.

55세에 퇴직 이후를 위해 준비를 했어야 한다. 60세는 늦다. – (예) 배당주 투자, 구매대행

은퇴자금 축적을 했어야 한다: 연봉이 2억대였지만 고연봉 세금이나 직위로 인한 씀씀이 (골프 등)로 인해 퇴직 후 자금이 부족했다.

강제퇴직 후 아내가 다른 사람에게 도움이 되도록 책을 써보라고 권유해서 책을 쓰면서 치유가 됨.

세번째 분은 정도영 소장입니다. 이 분은 유체이탈화법이라고 하죠. 자신의 말씀을 제3자처럼 말씀하십니다.

퇴직 이후에 무엇을 할지 알고 있다는 것만으로도 50%는 된 것이다: 다른 삶에 대해 생각해 보지못한 사람들이 많다. 퇴직 후 여행은 한달만 다니면 지친다.

50대/60대는 변화에 취약하기 때문에 미리 준비하는 자세가 중요하다.

유망자격증에 따르지 말고 구인공고가 많이 나는 자격증을 따야 한다. 자신에게 맞는 자격증을 따야 한다.

요양보호사 – 일은 힘드나 일자리는 많다.

전기분야 자격증 (전기기능사, 전기산업기사, 전기기사)이 일자리가 많다.

지게차 운전기능사가 일자리가 많다 – 그러나 자신에게 맞는지 따져봐야 한다.

사회복지사가 쓰임새가 넓다.

중장년 일자리의 70% 이상은 소개, 추천에 의한 것이다. 채용을 하는 경우는 지인 추천을 통한다. 퇴직 전 2년전부터 네트워킹을 해야 한다. 오랜만에 만나는 사람을 만나야 한다 (정보채널이 넓혀진다는 연구결과가 있다) 좋은 자리는 공고가 나오지 않는다.

그런데 Oligonucleotide 자체가 Oral Delivery가 된다면 어떨까요? mRNA Translational Regulation에 Clinically validated regimen은 Antisense Oligonucleotide 나 siRNA인데 RNA 기반인 siRNA에 비해 DNA gapmer를 보유한 Antisense Oligonucleotide는 Formulation Development에 따라 Oral Delivery가 될 가능성이 여전히 있어 보입니다. 다른 Tide 약물인 Peptide 약물이 최근 GLP-1 치료제 분야에서 경구용으로 성공하고 있는 것을 보면 더욱 이런 가능성을 간과하기 어려운데요.

그래서 Oral Antisense Oligonucleotide에 대한 생각을 좀 해보고자 합니다. 이것에 대해 Novartis 연구원이면서 블로거인 Derek Lowes의 글에서 시작해 볼까 합니다. 2017년에 쓴 글인데요 이렇게 오래 전의 글도 다시 읽어볼 수 있다는 게 역시 블로그의 매력이라 할 수 있습니다.

Readers may recall a post here last year about an odd trial of an antisense drug for Crohn’s disease. Celgene had acquired the drug (mongersen, GED-301) from Nogra Pharma of Ireland back in 2014 as a late-stage candidate, and for a while, things looked good. In fact, going back and reading the stories, you’d think that everything was pretty much on track:

Celgene ($CELG) bet big on the little-known Irish biotech Nogra Pharma when it partnered on a mid-stage drug for Crohn’s disease. And today Celgene spelled out the reasons why it gambled $710 million upfront on a Phase II drug, highlighting data that support a clear case that the therapy can help spur clinical remission in a broad group of patients.

An oral antisense agent is a pretty bold move, but then again, a Crohn’s drug of that sort just needs to hit its target in the gut wall, not make it into circulation. And mongersen’s target is Smad7, a key player in the transcriptional signaling machinery for an important inflammation pathway (among other things). This is the sort of target that is very difficult indeed to go after with a small molecule, and that’s when you see the antibodies and oligonucleotide-based modes get tried. Later results were not as encouraging, though. And the reason I called that trial uninterpretable almost exactly a year ago was that it had no control arm, making it very hard to tell the difference between mongersen’s effects and a placebo. On Friday, Celgene had an announcement on a full placebo-controlled Phase III trial, and guess what? It actually isn’t that different from a placebo. Fancy that. The announcement was that the trial was being discontinued due to futility; an interim analysis showed that nothing was happening. Unfortunately, that candidate was actually a pretty important part of Celgene’s plans and revenue projections. When the company did their 2014 deal, it raised eyebrows because of the steep upfront price for a relatively unproven therapy from a relatively unknown (and very small) partner, but Celgene was (as they said at the time) into Planning Boldly For the Future, as well as Executing Transformative Deals on Late-Stage Clinical Assets and all that stuff. Unfortunately, the science crept up and sank its teeth into the ankle of this mighty deal, and one would assume that mongersen itself is no more. There’s a lot of finger-pointing about putting that much money into something so thin, but of course if the compound had worked, everyone would be taking visionary dealmaker victory laps. It’s evaluating that “if the compound works” part that is the tricky part, and a tiny company’s oral antisense agent for Crohn’s was always going to be a gamble. You just wonder if it had to be quite as expensive a gamble as it was. And as always, whenever something like this happens, I will remind people that this is why you run big, well-controlled Phase III trials. Back in Phase II, mongersen looked as if it were going to work (as that quote above illustrates). It doesn’t seem to have any particularly bad safety issues, so under some regulatory proposals, that would have been the time to let suffering Crohn’s patients take it on a risk basis, speed up development, get the regulatory barriers out of the way, all that stuff. But that would have given everyone three years of useless placebo, at a no doubt stiff price. And since more drugs in clinical trials fail than work, I’m still baffled at how giving people a chance to pay for them at that point is supposed to improve health or save anyone money. It certainly wouldn’t have in this case. Celgene stuffed well over $700 million in real money into the shredder on this effort, and a million Crohn’s patients could have joined them.

이 블로그 글이 올라온 지 7년여가 지났지만 어찌된 영문인지 Nogra Pharma의 홈페이지에는 여전히 Mongersen의 임상3상이 진행 중인 것으로 나옵니다.

2015년 New England Journal of Medicine에 Mongersen의 임상2상 결과가 나와 있습니다.

The objective was to assess the efficacy and safety of GED-0301, an antisense oligodeoxynucleotide to Smad7, in active Crohn’s disease (CD).

METHODS:

This phase 3, blinded study randomized patients (1:1:1:1) to placebo or 1 of 3 once-daily oral GED-0301 regimens: 160 mg for 12 weeks followed by 40 mg continuously or alternating placebo with 40 or 160 mg every 4 weeks through week 52.

RESULTS:

In all, 701 patients were randomized and received study medication before premature study termination; 78.6% (551/701) completed week 12, and 5.8% (41/701) completed week 52. The primary endpoint, clinical remission achievement (CD Activity Index score <150) at week 12, was attained in 22.8% of patients on GED-0301 vs 25% on placebo (P = 0.6210). At study termination, proportions of patients achieving clinical remission at week 52 were similar among individual GED-0301 groups and placebo. More placebo vs GED-0301 patients achieved endoscopic response (>50% decrease from baseline Simple Score for CD) at week 12 (18.1% vs 10.1%). Additional endoscopic endpoints were similar between groups at weeks 12 and 52. More placebo vs GED-0301 patients had clinical response (≥100-point decrease in the CD Activity Index score) at week 12 (44.4% vs 33.3%); at week 52, clinical response rates were similar. Adverse events were predominantly gastrointestinal and related to active CD, consistent with lack of clinical and endoscopic response to treatment. Two deaths occurred (GED-0301 total group) due to small intestinal obstruction and pneumonia; neither was suspected by the investigator to be treatment-related.

DISCUSSION:

GED-0301 did not demonstrate efficacy vs placebo in active CD.

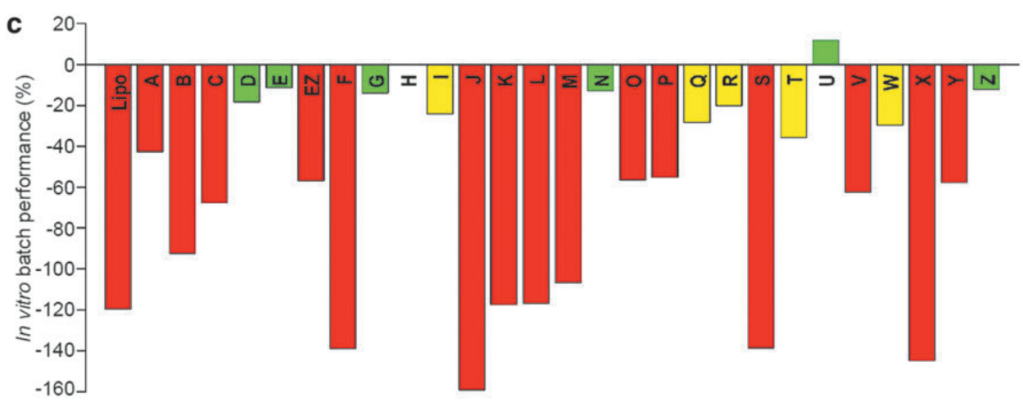

Batch 별로 SMAD7 in vitro test를 했을 때 약효가 크게 차이가 나는 것을 관찰했습니다. Green (best performance batches), Yellow (decreased performance batches), Red (poor performance batches)의 세가지 군으로 나눠보았을 때, Red의 것이 크게 낮은 것을 알 수 있습니다.

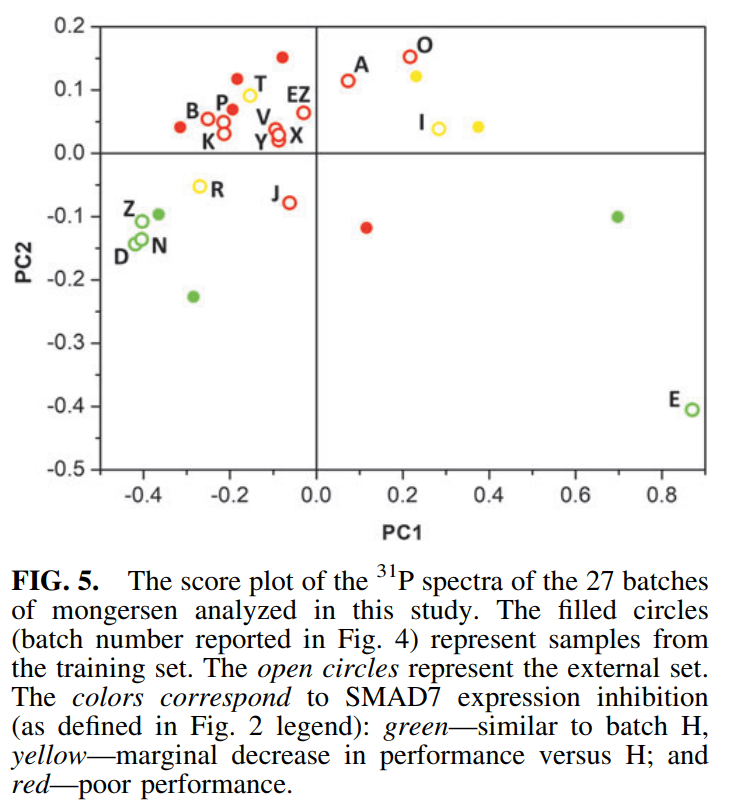

그리고 그 이유로 13P NMR을 측정해 본 결과 Batch 별로 Thiophosphates의 Chirality가 다르게 분포한 것을 발견한 것입니다. Green (best performance batches), Yellow (decreased performance batches), Red (poor performance batches)의 세가지 군으로 나눠보더라도 위치가 크게 차이가 나는 것을 알 수 있습니다. 따라서 Nogra Pharma의 결론은 Chirality of thiophosphates가 Critical Quality Attributes (CQAs)라는 것입니다. 흥미로운 관찰입니다.

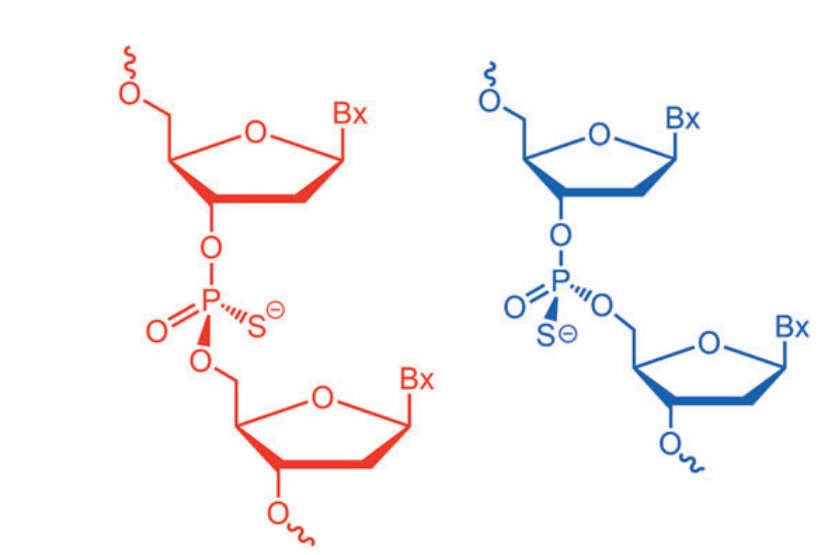

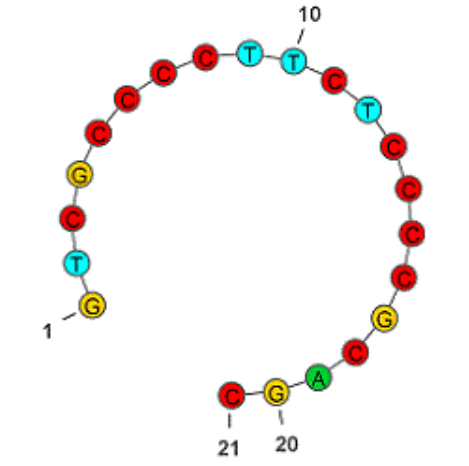

Mongersen은 21-nt Oligonucleotide인데 (3′-5′)d(P-thio)(G-T-m5C-G-C-C-C-C-T-T-C-T-C-C-C-m5C-G-C-A-G-C)로서 세번째 C와 17번째 C는 5-meC이고 모든 Linker는 Thiophosphate Bonds로 되어 있어서 실제로 N20 개의 Stereoisomers가 가능합니다.

이 결과에 대해 2023년 Pharmaceutics에서 이탈리아 과학자들은 Monsergen의 임상2상과 임상 3상 데이타가 큰 차이가 난 이유는 Thiophosphates Stereochemistry에 대한 Batch-by-batch variability 때문이라고 하는 논조를 냈습니다. 이 약물이 개발될 당시에는 Thiophosphate bond의 Chirality를 Control하는 Synthetic methods가 없었는데요 하지만 이제는 다양한 방법들이 존재합니다.

예를 들면 Wave Life Sciences가 바로 Thiophosphate Stereocontrol을 Platform 기술로 하는 회사입니다.

이외에도 Antisense Oligonucleotide 기술이 지금은 훨씬 진화해서 아마 새로운 디자인을 해야할 것으로 보이지만 Oral Antisense Oligonucleotide Drugs에 대한 가능성은 아직 개발 가능성이 남아있다고 볼 수 있을 것 같습니다. Mongersen은 아마 결국 다시 사용될 수는 없을 것 같습니다. 이 결과를 인정한다고 하더라도 어떤 Stereocontrol을 해야할지에 대한 연구도 필요하고 또한 Stereocontrolled Antisense Oligonucleotide 생산은 훨씬 비싸서 투자자를 만나기도 아마 어려울 것 같습니다. 그래도 한가지 알게 된 사실은 임상2상에서 성공하고 임상3상에서 실패한 경우 그냥 지나칠 것이 아니라 이와 같이 원인 규명이 반드시 필요하다는 것입니다. 기술진보는 계속되어 언젠가 Oral Antisense Oligonucleotides의 시대가 오기를 기대합니다.

Opioid 약물을 FDA에서 승인해 준 이래로 Opioid 약물로 인한 여러가지 부작용으로 인한 Opioid Endemic이 연일 기사를 도배하고 있습니다. 이런 가운데 Vertex는 최근 Non-Opioid Replacement NaV1.8 Inhibitor Suzetrigine에 대한 기대되는 임상3상 결과를 발표했습니다.

Amgen 출신의 Sean Harper 박사 등이 세운 VC 인 Westlake Village BioPartners가 2020년에 Suzetrigine에 대항하는 Best-in-class NaV1.8 Inhibitors를 개발하기 위해 Amgen 연구원들을 모아서 Latigo Biotherapeutics를 설립했습니다.

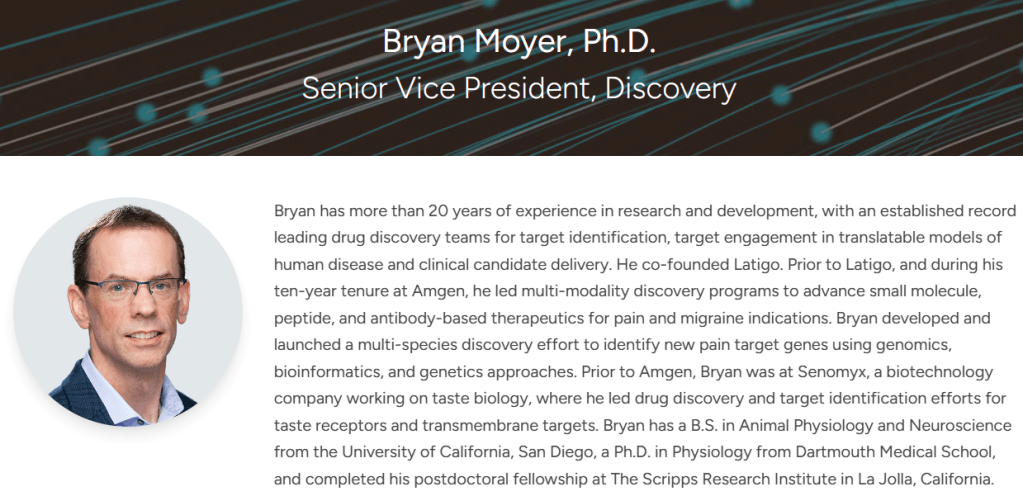

Amgen에서 NaV1.7 Inhibitor 개발을 했던 Bryan Moyer박사가 Co-founder and SVP Discovery로 참여하고 있습니다.

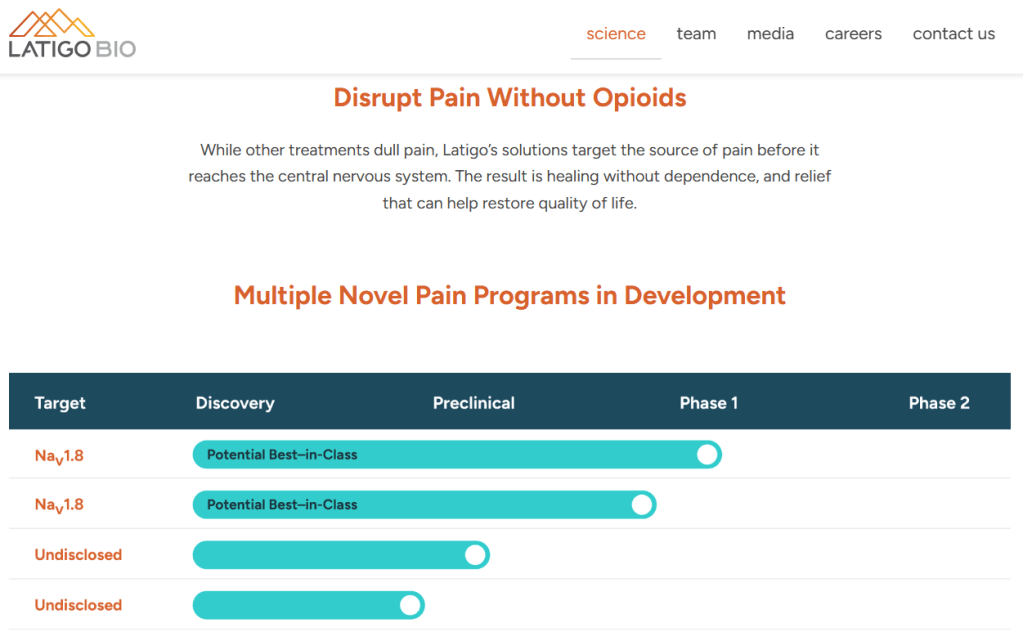

Latigo Biotherapeutics의 홈페이지에 나온 파이프라인을 보면 LTG-001이 임상1상을 진행 중이고 Follow-on molecule (NaV1.8 Inhibitor) 가 전임상 단계에 있습니다.

Latigo Biotherapeutics는 Amgen Neuroscience와 연관이 있습니다. 기사를 통해서 보면 Amgen은 2015년에 Novartis와 AMG 334 (Erenumab)라는 Calcitonin-Gene-Related Peptide (CGRP) receptor를 공동개발한다고 발표한 바 있습니다. 이 당시 Novartis의 BACE Inhibitor도 공동개발에 함께 들어가 있었습니다.

As for the migraine program, the companies said they will work to co-develop new Amgen drugs that include the Phase III compound AMG 334, the Phase I compound AMG 301, and potentially another Amgen compound. Novartis will have global co-development rights and commercial rights to Amgen’s migraine treatments outside the U.S., Canada, and Japan.

AMG 334 is a fully human monoclonal antibody under study for the prevention of migraine. AMG 334 targets the Calcitonin-Gene-Related-Peptide (CGRP) receptor, which according to Amgen is believed to transmit signals that can cause incapacitating pain. AMG 334 is currently under evaluation in several large global, randomized, double-blind, placebo-controlled trials to assess its safety and efficacy in migraine prevention. AMG 301 is a monoclonal antibody being investigated for the treatment of migraine.

“Our collaboration on BACE inhibition reflects Amgen’s strategic focus on genetically validated drug candidates while our collaboration in migraine creates an opportunity to more rapidly advance AMG 334 on a global scale,” Sean E. Harper, M.D., Amgen evp of research and development, said in a statement.

이 약물 Aimovig (AMG 334, Erenumab)은 2018년에 FDA로 부터 승인을 받았습니다.

The U.S. Food and Drug Administration today approved Aimovig (erenumab-aooe) for the preventive treatment of migraine in adults. The treatment is given by once-monthly self-injections. Aimovig is the first FDA-approved preventive migraine treatment in a new class of drugs that work by blocking the activity of calcitonin gene-related peptide, a molecule that is involved in migraine attacks. The FDA granted the approval of Aimovig to Amgen Inc.

Pain Medicine으로 Amgen에서는 오랜 기간 NaV1.7 Inhibitor의 개발에 투자를 해 왔습니다. Latigo의 SVP Discovery인 Bryan Moyer박사는 2017년에 Journal of Medicinal Chemistry에 NaV1.7 Inhibitor의 Lead Optimization에 관한 논문을 발표한 바 있습니다.

뿐만 아니라 2017년에는 Boston Children’s Hospital과 새로운 Pain Syndrome Targets를 발굴하기 위한 Genetic collaboraton을 발표한 바 있습니다. 이렇듯 Amgen의 Neuroscience 부문에서 Pain과 관련한 연구는 오랜기간 지속적으로 발전해 왔습니다.

Amgen (NASDAQ:AMGN) and Boston Children’s Hospital today announced that they have entered into a neuroscience research collaboration aimed at identifying novel pain targets based on human genetic analyses. The one-year collaboration will focus on patients with genetic anomalies of pain sensitivity. Amgen will leverage its industry-leading expertise in genetic target identification and validation and will have access to Boston Children’s Hospital’s Division of Pain Medicine to identify patients with abnormal pain conditions. Amgen and Boston Children’s Hospital will collaborate to validate the genetic findings as potential pain targets.

“Traditional approaches to analgesic drug discovery have been pretty disappointing during the past 20 years,” says Charles Berde, M.D., Ph.D., chief of the Division of Pain Medicine in the Department of Anesthesiology, Perioperative and Pain Medicine at Boston Children’s Hospital. “The most innovative biotech companies have realized that they need to pursue new directions for drug discovery. Patients with unusual patterns of increased or decreased pain responsiveness can offer important clues in this pursuit.”

“Amgen is pleased to enter into this collaboration as it underscores our extensive investment and expertise in pursuing targets that have clear genetic support,” said John Dunlop, Ph.D., vice president of Neuroscience Research at Amgen. “We look forward to working with Boston Children’s Hospital to explore novel pain targets that will potentially include new non-addictive approaches to treating pain in patients.”

The agreement brings Amgen, a world leader in human genetic target validation, together with Boston Children’s Hospital’s Division of Pain Medicine, the first and most active pediatric pain program in the world, and its Manton Center for Orphan Disease Research. Both organizations have leading researchers in neuroscience and genomics, including Michael Costigan, Ph.D., of the F.M. Kirby Neurobiology Center and Catherine Brownstein, M.P.H., Ph.D., in the Division of Genetics and Genomics and scientific director of the Manton Center for Orphan Disease Research.

Boston Children’s Hospital’s Division of Pain Medicine treats patients with rare conditions that make them strikingly insensitive to pain or, conversely, hypersensitive to pain or apt to experience pain spontaneously, with no apparent stimulus.

As part of the collaboration, the teams will study patients with the following pain syndromes:

genetic disorders that diminish pain sensitivity;

erythromelalgia, a condition causing intense, burning pain in the extremities;

paroxysmal extreme pain disorder, a condition characterized by skin flushing and severe pain attacks in various parts of the body; and

hereditary sensory and autonomic neuropathy.

그러나 2019년 10월말에 Amgen은 Neuroscience R&D 부문을포기하고 Layoff를 하게 됩니다. 항상 위기는 누군가에게 기회가 됩니다. Amgen Neuroscience EVP였던 Sean Harper 박사는 Westlake에서 새로운 벤처 스타트업을 생각하고 있었는데 Amgen이 Novartis와 공동으로 개발하던 BACE Program이 Alzheimer치료제로서 효과를 보이지 않자 뇌과학 분야를 중단한다는 발표는 Sean Harper 박사에게는 기회가 되었습니다. 2020년에 Bryan Moyer 박사를 비롯한 ex-Amgen Neurosciences Drug Hunters들을 모아 Latigo Biotherapeutics를 설립할 수 있었습니다.

Recent scientific breakthroughs have transformed treatment of some cancers, as well as a number of rare genetic diseases. But disease-modifying medicines for the most prominent diseases of the brain, such as Alzheimer’s and Parkinson’s, have remained elusive.

Earlier this year, Amgen reported a major clinical setback in Alzheimer’s. Along with its partner Novartis, the drugmaker stopped two studies testing an experimental BACE inhibitor in pre-symptomatic patients with the neurodegenerative disease.

The trial failure was one of many for the Alzheimer’s field, but, for Amgen, it brought to a close the only named clinical neuroscience program in its pipeline outside of the approved migraine therapy Aimovig (erenumab).

Now, Amgen will steer its internal R&D efforts clear of neuroscience, prioritizing instead cardiovascular disease, oncology and inflammatory diseases. As a result of the decision, approximately 180 roles will be affected, according to a company spokesperson.

“We made the difficult decision to end our research in neuroscience, which is largely based in Cambridge, Mass.,” said the spokesperson in an emailed statement. “We are consolidating our U.S.-based research presence primarily in Thousand Oaks and San Francisco.”

On Tuesday’s earnings call, company executives previewed how Amgen could stay involved via partnerships. CEO Bob Bradway said they’ll explore models with venture capital or academic institutions, particularly via deCODE, a subsidiary specializing in genetics, to better understand these diseases.

“We believe that genetics will ultimately drive progress in this area, and we’ll continue to work with deCODE to generate insights,” Bradway said on the Tuesday call.

Reese also added the company will maintain support for the ongoing clinical development of its migraine therapy, Aimovig (erenumab).

Amgen’s decision bears similarities with those taken by some of its peers.

Pfizer, for instance, first announced its intention to halt neuroscience work in January 2018. Several months later, the big pharma teamed up with Bain Capital to launch a start-up called Cerevel that took over development efforts for many of Pfizer’s CNS compounds.

And Biogen has remained focused on developing central nervous system treatments, even as it has suffered multiple clinical failures. In a shocking turn, the big biotech recently revived development efforts for an experimental Alzheimer’s drug.

Latigo Biotherapeutics는 Johns Hopkins University의 Lieber Institute와 새로운 NaV1.9 Inhibitor에 대해 2022년 10월에 발표한 적이 있습니다. 이 약물의 적용분야로 거론된 것은 진통제, 관절염, 심장병, 위경련, 암, 정신병 등 광범위한 분야의 통증완화 치료제의 개발이었습니다.

Latigo Biotherapeutics Inc. and Lieber Institute Inc. have synthesized new methyl-substituted pyridine and pyridazine compounds acting as sodium channel protein type 10 subunit α (Nav1.8) channel blockers reported to be useful for the treatment of pain, arthritis, atherosclerosis, irritable bowel syndrome, cancer and psychiatric, respiratory and neurological disorders, among other disorders.

그리고 지난달에 $135 Million Series A를 했다는 발표를 했습니다. 이미 LTG-001이 임상1상에 진입을 한 상태인데 Vertex를 속히 따라잡기 위해서 조기에 임상1상을 완료하고 다양한 임상2상을 시작한다는 계획입니다. Vertex 약물이 primary endponts는 좋게 나왔지만 secondary endpoint는 아직 확실한 승리를 장담할 수 없다고 생각하고 이런 Vertex 약물 Suzetrigine (VX-548)의 약점을 파고든다는 전략입니다. 임상2상에서는 Chronic Pain 에 대해서도 임상시험을 계획하고 있습니다.

A new pain-focused biotech is emerging this Valentine’s Day—not to cure heartache, but pretty close. Latigo broke stealth cover today with $135 million to chase Vertex, the front runner in the effort to develop a new non-opioid pain option.

Latigo Biotherapeutics unveiled Wednesday with a lead nav1.8 inhibitor, LTG-001, currently being tested in healthy volunteers. If that target sounds familiar, it’s because Vertex is going after it as well with its own non-opioid treatment. VX-548just beat placebo in a phase 3 trial in patients with acute pain but did not manage to best the standard of care, Vicodin. Vertex plans to file for FDA approval anyway this year and is seeking a broad label in moderate to severe acute pain.

Sean Harper, M.D., co-founding managing director of Westlake Village BioPartners, which founded and incubated Latigo beginning in 2020, said beating opioids is a “tough bar.”

“I think a goal in an acute pain setting to beat that type of comparator handsomely … would have to be [an] aspiration,” he said in an interview. With that said, Harper believes Latigo’s molecule will differentiate from Vertex’s by mitigating off-target effects in the brain and by tackling chronic pain.

“We have every reason to believe that our nav1.8 inhibitor will be effective in both acute and chronic pain,” Harper said in an interview. “But obviously, that remains to be proven.”

The asset is in a healthy volunteers study now, and executives hope to initiate a phase 2 study for patients with acute pain later this year.

Harper said some of the foundational science behind LTG-001 originated from the Lieber Institute for Brain Development in Baltimore but that preclinical work was done at labs in Thousand Oaks, California. The VC firm plucked homegrown talent for help, hiring many Amgen employees who left as part of the pharma’s neuroscience divestment in late 2019. The next molecule behind LTG-001 was developed completely in-house, Harper said, in addition to other discovery work.

Desmond Padhi, an operating partner at Westlake, will be the interim CEO while Neuron23 CEO Nancy Stagliano, Ph.D., has been called upon to chair the board. Although corralling investor interest is never easy, Stagliano acknowledged that Latigo has “hit this important catalyst at just the right time.”

“Once in a while, you get the timing to be perfect,” she said.

The inaugural financing was co-led by 5AM Ventures and Foresite Capital with participation from Corner Ventures. Padhi wouldn’t lay out how much of a runway the $135 million affords but expects it would allow the company to complete the ongoing phase 1 trial and a future phase 2 acute pain study while planning for the chronic pain study. He also said Latigo was planning to initiate a clinical trial for the second molecule in the “near future.”

같은 날 Biospace의 기사는 좀더 약물의 디자인과 관련한 차별점에 방점을 찍고 기사를 송고했습니다. 독성 완화를 위해 peripheral nervous system에만 전달을 하고 Central Nervous System (CNS)에는 약물이 들어가지 않도록 디자인하고 테스트를 했다는 것을 강조하고 있습니다. 뿐만 아니라 Latigo 연구팀이 Amgen에서 오랜기간 개발에 참여한 NaV1.7과의 병용이 중요하다는 얘기도 Yale University의 Waxman 박사의 입을 빌려 어필하고 있습니다.

Founded by Westlake Village BioPartners in 2020, Latigo is developing non-opioid-based therapeutics against genetically validated targets for pain—and with the opioid epidemic continuing to ravage the U.S., new options are urgently needed. In an interview with BioSpace, Sean Harper, founding managing director at Westlake, noted a dearth of available programs in which to invest.

“When we began to get into this focus of a pain company, we found that . . . it [was] really hard to find any programs that you could license in,” he said. Additionally, he said it was difficult to find people with expertise in the space, “because there’s so little investment and innovation going on in biopharma or academia in pain. It’s kind of shocking.”

Fortunately for Westlake, Amgen—where Harper was previously head of R&D—had recently made the strategic decision to get out of the neuroscience space, which included pain, Harper said. “I knew the pain research unit . . . had these fabulous drug hunters with deep expertise in pain, and when they were laid off, we swooped in and we hired them and assembled this team.”

‘Best-in-Class’ Potential

Like Vertex’s VX-548, Latigo’s lead program, LTG-001, is a selective NaV1.8 inhibitor. “There definitely is room for multiple agents targeting NaV1.8,” said Stephen Waxman, a professor of neurology at Yale School of Medicine who previously consulted for Latigo. “At a minimum, there are going to be small nuances of difference.”

While hitting the primary endpoint of significant reduction of pain intensity from 0 to 48 hours in two Phase III trials, VX-548 missed a key secondary endpoint—superiority to Vicodin—and analysts also questioned the drug’s performance in another secondary endpoint: median time to pain relief. VX-548’s time-to-onset had a “more rapid onset to meaningful pain relief” than placebo, Vertex reported, with median time to pain relief being two hours in patients following abdominoplasty (tummy tuck) and four hours in bunionectomy patients versus eight hours for the placebo group.

In its press release, Latigo stated that LTG-001, currently in Phase I trials, has the potential for rapid onset. Harper said VX-548’s time-to-onset “may not be entirely a characteristic of the target. . . . It may be partially due to the particular characteristics of the compound, and we hope that the particular characteristics of our compound could result in faster time to onset.”

Desmond Padhi, interim CEO of Latigo, said the team believes LTG-001 has the potential to be best-in-class. “We’re very focused on making sure that we get optimal biodistribution of our compounds to the tissue of interest . . . the peripheral nervous system where the target is expressed, and minimizing exposure in tissues where the target is not expressed,” the central nervous system (CNS).

But Waxman noted that the jury is still out on the benefits of specifically targeting the peripheral nervous system. He pointed to research suggesting that another sodium channel, NaV1.7, must be blocked within the spinal cord in order to get adequate pain relief. This question has not been raised regarding NaV1.8, he said, but “whether peripheral sequestration of the NaV1.8 blocker is an advantage or not, I think, is still up for grabs.”

Alongside Latigo and Vertex in the pain space, Orion Pharmaceuticals is developing also developing a NaV1.8 inhibitor, and Virpax Pharmaceuticals is looking at other targets.

Harper said he has been interested in the pain space for a long time but has been met a “huge amount of resistance” with people noting the very genericized market. “Of course, that’s what happens when there’s been no innovation for 30 years. Everything’s off-patent.”

“I believe that . . . you have to be a little bit of a contrarian, and kudos to Vertex for having the first real breakthrough here to get it into proof of concept in humans,” he said. “It’s huge for patients.”

같은 날에 나온 Biopharmadive의 기사는 Vertex 약물이 통증 완화에 몇시간이 걸린다는 약점을 파고드는 디자인이라는 것에 방점을 찍고 있습니다. 하지만 Vertex도 Best-in-class 약물 개발이 진행 중이라는 점을 잊지 않고 있습니다.

Vertex’s results provided clinical validation of a hypothesis that was already well supported by genetic data. They also set a high bar for success. And with a drug ready for regulatory review, Vertex has established a sizable head start on any competition.

Even so, Latigo claims there’s room to improve on its larger rival’s treatment.

“When a new category opens up like this, somebody makes a first-in-class molecule. Occasionally, that’s the best-in-class, but most of the time something else comes along that is more refined,” said Harper. “So we’re really focused on the differentiation that we can bring to the table.”

Latigo’s lead drug, dubbed LTG-001, is currently in a Phase 1 study. The company is preparing to advance it into a mid-stage trial in acute pain, such as after bunion or stomach surgeries. Testing in chronic pain is also part of the plan, said Desmond Padhi, interim CEO and an operating partner at Westlake.

According to Padhi, preclinical data has shown LTG-001 to be highly selective for NaV1.8, avoiding penetration into the brain and the side effects that would go with it. He also noted early safety data suggesting Latigo could explore a wide range of doses.

Selectivity was also prioritized by Vertex’s chemists, who crafted a molecule that’s at least 30,000 times more selective for NaV1.8 than eight other sodium channels. The Massachusetts company is working on successor molecules, too.

Harper describes such selectivity for NaV1.8 as “table stakes” for companies who, like Latigo, hope to follow Vertex. Still, he noted questions that remain unanswered, such as whether the several hours it took for Vertex’s compound to provide relief in testing reflect the Nav1.8 approach or the drug.

“We think it’s possible that could be a molecule attribute,” said Harper. “We think it’s possible that you could get a faster onset with a different molecule, along with perhaps more efficacy by being able to push dose safely in the chronic setting.”

Latigo, which currently has 26 employees, has to prove that in testing. But investor interest is high, said board chair and Neuron23 CEO Nancy Stagliano, giving Latigo options for further fundraising.

“I do think the potential here is to raise capital via a number of vehicles,” said Stagliano. “It’s now going to be a question of what the company views as the best situation.”

Endpoints News에서는 좀 색다른 것을 적고 있는데, Sean Harper가 Drug Pricing에 대해 경험한 일을 나누고 있습니다. 과거 Migraine 약물인 Avvig을 개발할 때 경험을 토대로 만성 통증 완화 치료는 Opioid로 거의 불가능하기 때문에 이러한 Unmet Medical Need를 만족하는 Non-Opioid 약물의 가격적 Merit이 있다는 것을 얘기하고 있습니다.

The company uses computer-assisted structural-based drug design to “optimize the selectivity, potency and biodistribution” of its compounds, Padhi said. In Nav1.8, Latigo is making sure its drug gets into the peripheral nervous system while avoiding the central nervous system.

During his days at Amgen, Harper was confronted with the realities of drug pricing, a key factor that Vertex, Latigo and other biotechs will have to contend with as they develop non-opioid pain medicines. He pointed to his experience developing biologics for migraine prophylaxis, describing migraine as a “different kind of pain syndrome.”

“Trying to treat patients with chronic pain with opioids is really virtually impossible, so you end up with a lot of patients who you send home with nothing that works. There’s an enormous opportunity,” Harper said.

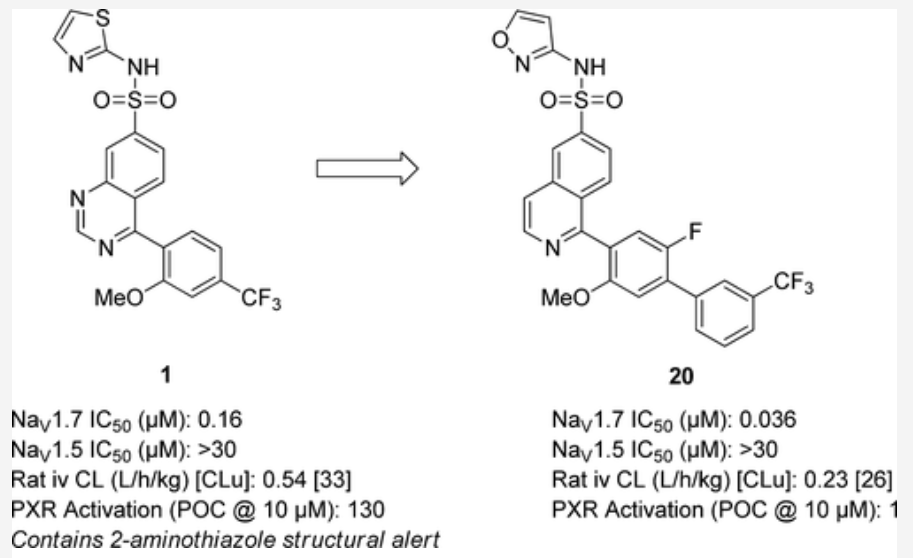

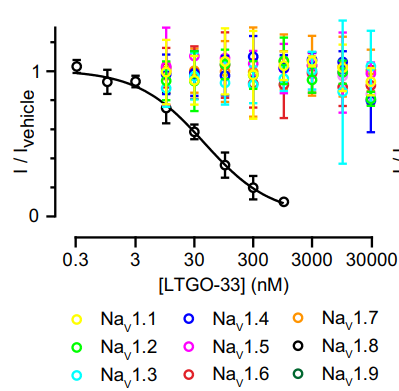

올해초에 Latigo Biotherapeutics의 Bryan Moyer 팀은 LTGO-33이라는 약물에 대한 연구결과를 Molecular Pharmacology에 발표했습니다. LTGO-33의 구조는 아래와 같습니다.

NaV1.1을 비롯한 8개의 타겟에 비해 NaV1.8에 대한 선택성이 600배 이상입니다. LTG-001은 LTGO-33에서 보다 Lead Optimization 된 약물일 것이니까 선택성이나 약효면에서 좋다는 가정을 할 수 있겠습니다. Non-Opioid Pain Medicine 개발에서 과연 ex-Amgen vs Vertex의 경쟁이 어떻게 판결나게 될지 흥미진진합니다.

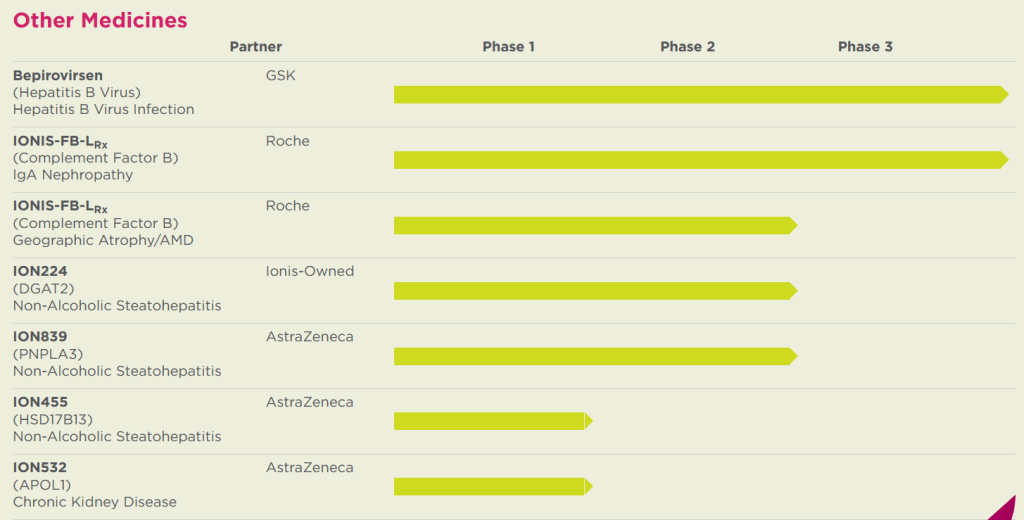

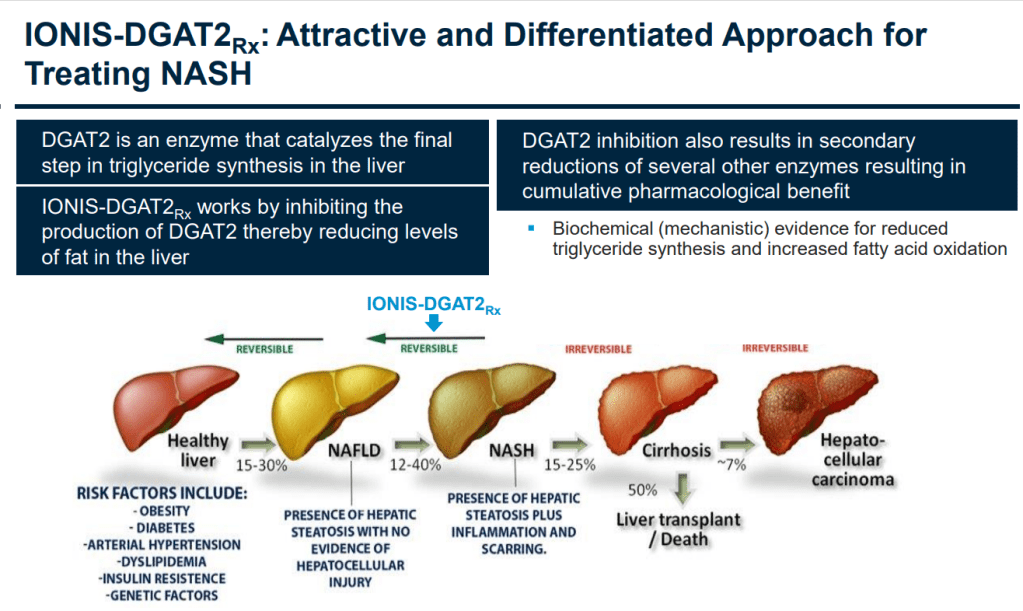

최근에는 Neurology 분야에서도 좋은 결과가 많이 나오지만 NASH (Non-Alcoholic Steatohepatitis) 분야에도 3개의 약물이나 파이프라인에 있습니다. 이 중 AstraZeneca와 파트너쉽된 두개 약물과 자체 개발 약물인 ION224 (Ionix-DGAT2rx)가 있습니다.

Ionis-AstraZeneca NASH drug deal은 2018년에 $30 Million upfront 및 총 $400 Million으로 계약을 했습니다.

AstraZeneca has licensed a NASH candidate from Ionis. The Big Pharma is paying $30 million upfront to pick up the rights to the program and take it into the clinic.

Ionis advanced the asset through target validation and into development with the strategic support of AstraZeneca, which secured a front-row seat on its progress through a cardiovascular, metabolic and renal disease deal it struck in 2015.

The drug, like one previously licensed by AstraZeneca, features antisense technologies intended to improve affinity chemistry and cell-specific targeting.

“This combination provides us with drugs that are substantially more potent than either Generation 2.5 or LICA alone, and supports administration of infrequent, very low doses, and even enables the potential for oral dosing,” Ionis COO Brett Monia said in a statement.

Gen 2.5 LICA는 현재 가장 약효와 독성 및 세포선택성 등에서 가장 앞선 기술 플랫폼입니다.

Beyond that, little is known publicly about the program. There are no online references to the drug, IONIS-AZ6-2.5-LRx, from before news of the licensing deal broke and neither Ionis nor AstraZeneca has disclosed its target.

Ionis has a long-standing interest in NASH, though. The biotech’s Akcea-partnered angiopoietin-like 3 protein drug AKCEA-ANGPTL3-LRx is currently undergoing phase 2 testing in patients with NASH and other conditions to assess its effect on endpoints including liver fat. A phase 2 trial of another Ionis drug, IONIS-DGAT2Rx, is also using liver fat as an endpoint. The IONIS-DGAT2Rx trial is enrolling type 2 diabetics at risk of NASH.

By offloading its latest NASH drug, Ionis has landed a $30 million upfront fee and a chance to pull in up to $300 million in milestones. If IONIS-AZ6-2.5-LRx comes to market, AstraZeneca will pay Ionis tiered royalties that top out in the low teens.

The financial terms are the same as for the last Ionis drug licensed by AstraZeneca. That deal gave AstraZeneca the rights to the kidney disease candidate IONIS-AZ5-2.5Rx, now known as AZD2373.

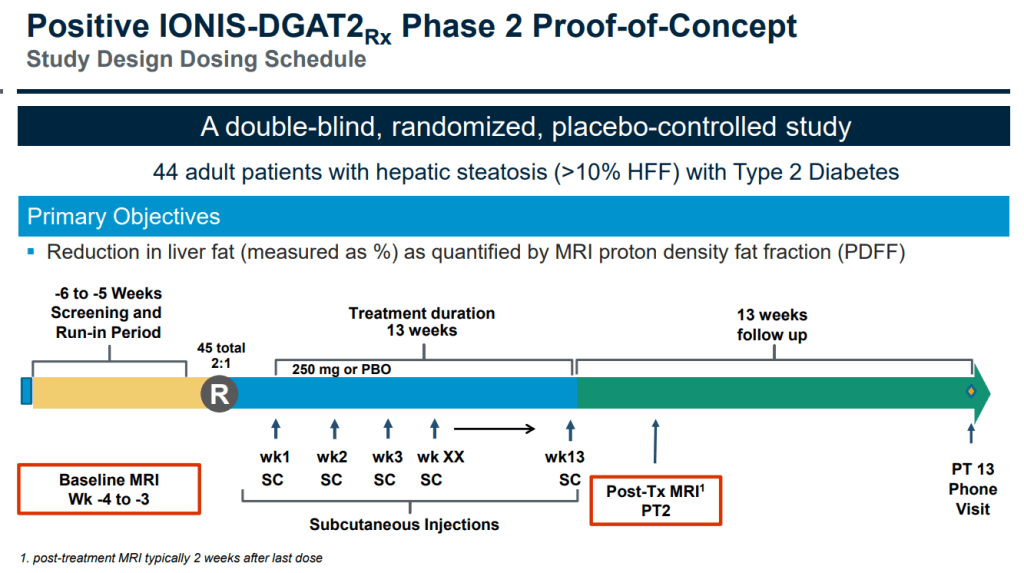

2020년에 UC San Diego School of Medicine의 Rohit Roomba 교수 연구진에서 ION224 (Ionix-DGAT2rx)의 13주 임상2상 결과를 The Lancet Gastroenterology and Hepatoloty에 발표했습니다.

Using a first-of-its-class drug in a clinical trial, an international research effort headed by a scientist at University of California San Diego School of Medicine reports that inhibition of a key enzyme safely and effectively improved the health of persons with non-alcoholic fatty liver disease (NAFLD), a chronic metabolic disorder that affects hundreds of millions of people worldwide.

The gene silencing approach represents a novel way to reverse NAFLD. The findings are published in the June 15, 2020 online issue of The Lancet Gastroenterology and Hepatology.

NAFLD occurs when fat accumulates in liver cells due to causes other than excessive alcohol intake. The precise cause is not known, but diet and genetics are believed to play substantial roles. The condition is typically not noticed until the disease is well-advanced, and perhaps has transitioned to non-alcoholic steatohepatitis (NASH), a progressive form that can lead to cirrhosis, liver cancer and liver failure.

There is no cure. Treatment primarily consists of ameliorating contributory factors, such as losing weight, improving diet, exercising more and controlling for other conditions, such as diabetes and hypertension. No Food and Drug Administration-approved medications exist. In worst cases, a liver transplant may be required.

“NAFLD wasn’t even recognized as a disease three decades ago; now it is alarmingly prevalent, affecting roughly one-quarter of all Americans and emerging as one of the leading causes for liver transplant in the United States,” said the study’s lead author Rohit Loomba, MD, professor of medicine in the Division of Gastroenterology at UC San Diego School of Medicine and director of the UC San Diego NAFLD Research Center. “Given its relative ubiquity and its potentially calamitous consequences, safe and effective treatments are absolutely needed.”

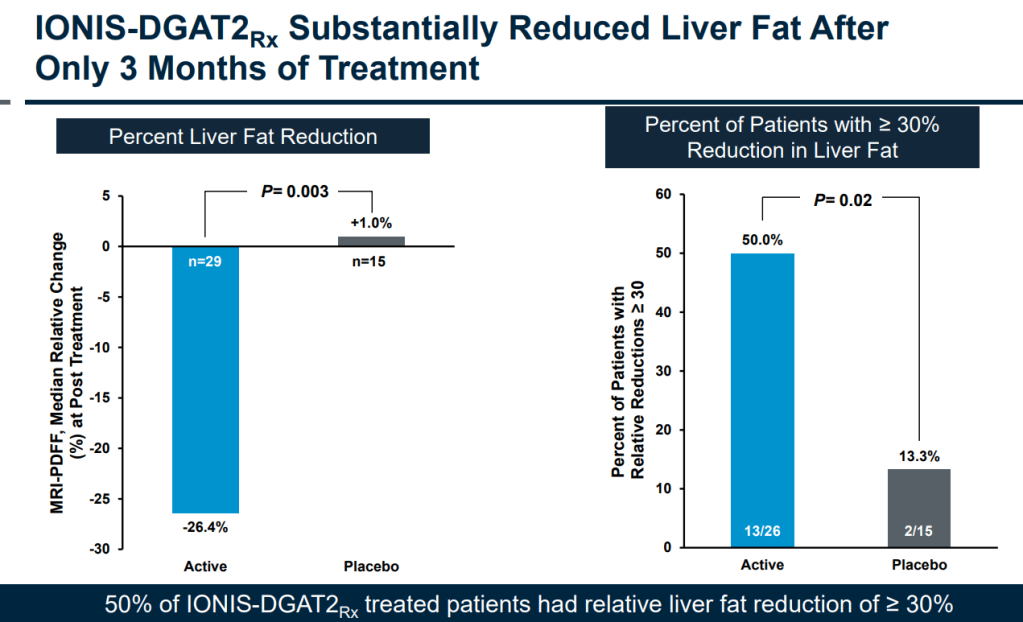

In the double-blind, randomized, placebo-controlled Phase II trial, Loomba and colleagues enrolled 44 qualifying participants at 16 sites in Canada, Poland and Hungary. For 13 weeks, participants were injected with either an antisense inhibitor called IONIS-DGAT2 or a placebo. The inhibitor, produced by Carlsbad-based Ionis Pharmaceuticals, interferes with Diacylglycerol-O-acyltransferace or DGAT2, one of two enzyme forms required to catalyze or accelerate the production of triglycerides, a type of fat found in blood. High levels of triglycerides boost fat storage throughout the body, including the liver.

The researchers found that after 13 weeks of treatment, participants who received the enzyme inhibitor experienced measurable reductions in fatty liver levels compared to baseline, without elevated levels of fats, enzymes or sugars in the blood. There were six reported serious adverse events, including a cardiac arrest and deep vein thrombosis, but the researchers determined the events were unrelated to the study drug.

“These findings showed robust reduction in liver fat by MRI without corresponding increases in blood lipids,” said Loomba. “Given significant proportion of patients achieving roughly a 30 percent reduction in MRI-PDFF, the threshold that corresponds with higher odds of histologic response when treated for a longer duration, it looks like after just 13 weeks of treatment, the drug was actually slowing progression of NAFLD to NASH.

“All of this is very encouraging and argues for the next step: longer term trials to further investigate the potential of this drug in improvement of liver histologic features associated with NASH, the progressive sub-type of NAFLD.”

Co-authors of the study include: Erin Morgan, Lynnetta Watts, Shuting Xia, Lisa A. Hannan, Richard S. Geary, Brenda F. Baker and Sanjay Bhanot, all at Ionis Pharmaceutical, Carlsbad, Calif.

Funding for this research came from Ionis Pharmaceuticals. Loomba is supported, in part, by the National Institute of Diabetes and Digestive and Kidney Diseases (grants R01DK106419 and P30DK120515).

Disclosures: Rohit Loomba is a consultant or advisory board member for Arrowhead Pharmaceuticals, AstraZeneca, Bird Rock Bio, Boehringer Ingelheim, Bristol-Myer Squibb, Celgene, Cirius, CohBar, Conatus, Eli Lilly, Galmed, Gemphire, Gilead, Glympse bio, GNI, GRI Bio, Intercept, Ionis, Janssen Inc., Merck, Metacrine, Inc., NGM Biopharmaceuticals, Novartis, Novo Nordisk, Pfizer, Prometheus, Sanofi, Siemens, and Viking Therapeutics. In addition, his institution has received grant support from Allergan, Boehringer-Ingelheim, Bristol-Myers Squibb, Cirius, Eli Lilly and Company, Galectin Therapeutics, Galmed Pharmaceuticals, GE, Genfit, Gilead, Intercept, Grail, Janssen, Madrigal Pharmaceuticals, Merck, NGM Biopharmaceuticals, NuSirt, Pfizer, pH Pharma, Prometheus, and Siemens. He is also co-founder of Liponexus, Inc. His co-authors are all employees and/or stockholders of Ionis Pharmaceuticals.

최근에 160명 환자에 대한 51주 경과에 대한 임상2상 발표를 했는데 120 mg을 맞은 환자에서 44%가 >50% 의 Liver Steatosis 개선을 보였습니다. 아주 긍정적입니다. 그리고 32%는 1기 이상의 Stage 개선을 보였습니다. 이러한 임상결과를 가지고 Pivotal clinical trials로 진입할지 기대됩니다.

Ionis Pharmaceuticals, Inc. (Nasdaq: IONS) announced positive results from a Phase 2 study of ION224, an investigational DGAT2 antisense inhibitor in development for the treatment of metabolic dysfunction-associated steatohepatitis (MASH), previously referred to as nonalcoholic steatohepatitis (NASH). The study met its primary endpoint at both doses (120 mg and 90 mg), achieving liver histologic improvement, and also met the important secondary endpoint of MASH resolution.

Key highlights from the 160-patient study at 51 weeks included:

ION224 achieved statistically significant liver histologic improvement as measured by at least a 2-point reduction in NAFLD Activity Score (NAS)* (p<0.001 (120 mg) and p=0.015 (90 mg)).

Subgroup analysis indicated that significant improvements in the primary endpoint were observed in patients with both F2 and F3 (advanced) fibrosis.

ION224 achieved statistically significant MASH resolution without worsening of fibrosis, as measured by biopsy (p=0.039).

44% of patients treated with 120 mg achieved ≥50% relative reduction in liver steatosis as measured by MRI-PDFF compared to 3% for placebo.

32% of patients treated with 120 mg achieved a ≥1 stage improvement in fibrosis without worsening steatohepatitis as measured by biopsy compared to 12.5% for placebo.

ION224 was safe and well-tolerated in the study.

“This Phase 2 trial of ION224 is the first to demonstrate clinical evidence that the reduction of hepatic fat after DGAT2 inhibition correlates with improvements in MASH histological endpoints,” said Rohit Loomba, MD, MHSc, professor of medicine and chief, division of gastroenterology and hepatology, University of California San Diego; founding director, MASLD Research Center, University of California San Diego. “I believe ION224 offers a unique precision medicine opportunity with an approach that is potentially complementary to others in development for MASH, and I look forward to continued evaluation of this important investigational medicine.”

MASH is the more severe form of metabolic dysfunction-associated steatotic liver disease (MASLD) and can lead to liver fibrosis, cirrhosis and liver-related death. ION224 is an investigational LIgand-Conjugated Antisense (LICA) medicine designed to reduce the production of diacylglycerol acyltransferase 2 (DGAT2) to treat patients with MASH.

“Reducing the production of DGAT2 enzyme decreases the overproduction of triglycerides that contribute to excess liver fat, which can result in liver damage and inflammation. We are encouraged by these ION224 data, showing that a monthly subcutaneous medicine targeting DGAT2 has the potential to improve MASH and prevent its progression to more severe stages, including advanced liver fibrosis and cirrhosis,” said Sanjay Bhanot, MD, PhD, senior vice president and chief medical officer at Ionis. “The inhibition of DGAT2 represents a novel approach for MASH, a progressive disease in need of better treatment options. We look forward to sharing the full results from this study at an upcoming medical conference and discussing next steps to advance this potentially promising therapy for patients.”

In this study, ION224 was safe and well-tolerated in MASH participants. Those in the ION224 study arms did not experience any worsening of hepatic or renal function or gastrointestinal side effects, and there was a lower rate of early termination compared to placebo. Additionally, there were no on-study deaths or treatment-related serious adverse events.

The adaptive Phase 2, two-part, multi-center, randomized, double-blind, placebo-controlled study was designed to assess the efficacy, safety and pharmacokinetics of multiple doses of ION224 when administered subcutaneously once-monthly in adults with MASH. The study enrolled 160 patients to receive ION224 or placebo over a period of 49 weeks. In Part 1, 93 patients were randomized 1:1:1 to the three dose cohorts (60, 90, and 120 mg) and within each dose cohort, randomized 3:1 to receive ION224 or placebo. In Part 2, an additional 67 patients were randomized 1:1 to two selected dose cohorts (90 and 120 mg) and then in a 2:1 ratio to receive either ION224 or placebo within each cohort. The study was powered for the primary endpoint, which was the percentage of patients who achieved MASH histologic improvement, defined as achieving at least a 2-point reduction in NAS with at least 1-point improvement in hepatocellular ballooning or lobular inflammation, and without worsening of fibrosis at end of the treatment period.

About ION224 ION224 is an investigational LIgand-Conjugated Antisense (LICA) medicine designed to reduce the production of diacylglycerol acyltransferase 2 (DGAT2) to treat patients with MASH. DGAT2 is an enzyme that catalyzes the final step in triglyceride synthesis in the liver. Reducing the production of DGAT2 should therefore decrease triglyceride synthesis in the liver. Additionally, there is evidence of an increase in both fatty acid oxidation and oxidative gene expression associated with antisense inhibition of DGAT2. ION224 offers a unique approach, which is potentially complementary to other therapies currently in clinical development.

About Metabolic dysfunction-associated steatohepatitis (MASH) MASH is the more severe form of metabolic dysfunction-associated fatty liver disease (MASLD). It is related to the epidemic of obesity, pre-diabetes and diabetes. Unlike liver disease caused by alcohol consumption, MASH is the result of an accumulation of fat in the liver, which can lead to inflammation and cirrhosis, an advanced scarring of the liver that prevents the liver from functioning normally. About 20% of MASH patients are reported to develop cirrhosis, which is associated with increased risk of liver-related and overall mortality.i MASH is the fastest growing indication for liver transplantation in the U.S. and Europe.ii

In 2023, several multinational liver societies made the recommendation to update NAFLD to metabolic dysfunction-associated steatotic liver disease (MASLD) and to update non-alcoholic steatohepatitis (NASH) to metabolic dysfunction-associated steatohepatitis (MASH). Ionis has adopted the use of MASH to describe this Phase 2 trial. ION224-CS2 is registered on clinicaltrials.gov as a study in patients with non-alcoholic steatohepatitis (NASH) and was registered before the recommended update.

About Ionis Pharmaceuticals, Inc. For three decades, Ionis has invented medicines that bring better futures to people with serious diseases. Ionis currently has five marketed medicines and a leading pipeline in neurology, cardiology, and other areas of high patient need. As the pioneer in RNA-targeted medicines, Ionis continues to drive innovation in RNA therapies in addition to advancing new approaches in gene editing. A deep understanding of disease biology and industry-leading technology propels our work, coupled with a passion and urgency to deliver life-changing advances for patients. To learn more about Ionis, visit Ionispharma.com and follow us on X (Twitter) and LinkedIn.

Forward-looking Statements This press release includes forward-looking statements regarding Ionis’ business and the therapeutic and commercial potential of ION224, additional medicines and technologies. Any statement describing Ionis’ goals, expectations, financial or other projections, intentions, or beliefs is a forward-looking statement and should be considered an at-risk statement. Such statements are subject to certain risks and uncertainties, including but not limited to those related to our commercial products and the medicines in our pipeline, and particularly those inherent in the process of discovering, developing and commercializing medicines that are safe and effective for use as human therapeutics, and in the endeavor of building a business around such medicines. Ionis’ forward-looking statements also involve assumptions that, if they never materialize or prove correct, could cause its results to differ materially from those expressed or implied by such forward-looking statements. Although Ionis’ forward-looking statements reflect the good faith judgment of its management, these statements are based only on facts and factors currently known by Ionis. Except as required by law, we undertake no obligation to update any forward-looking statements for any reason. As a result, you are cautioned not to rely on these forward-looking statements. These and other risks concerning Ionis’ programs are described in additional detail in Ionis’ annual report on Form 10-K for the year ended Dec. 31, 2023, which is on file with the SEC. Copies of this and other documents are available at www.ionispharma.com.

Ionis Pharmaceuticals® is a registered trademark of Ionis Pharmaceuticals, Inc.

* Nonalcoholic Fatty Liver Disease Activity Score (NAS) with at least 1-point improvement in hepatocellular ballooning or lobular inflammation, and without worsening in fibrosis stage.

iLe MH, et al. Clin Mol Hepatology 2022;28:841–850. iiEstes C, et al. Hepatology. 2018;67(1):123-133.

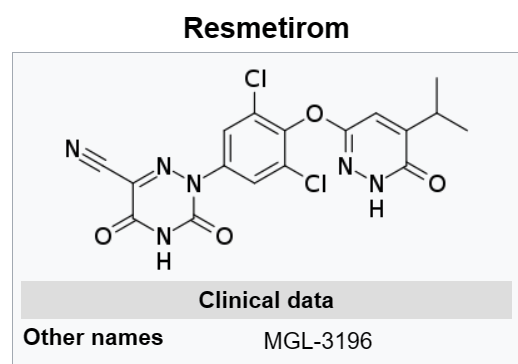

이런 날을 보려고 바이오텍 연구원으로 삽니다. 드디어 기다리고 기다리던 MASH (Metabolic dysfuction-associated steatohepatitis) 치료제가 FDA 승인 관문을 넘었습니다. 그 약물은 전에 임상3상 성공소식을 올렸던 Madrigal Pharmaceuticals의 Resmetirom입니다.

Madrigal Pharmaceuticals’ NASH drug won an accelerated approval on Thursday, becoming the first treatment for a liver disease that for years has vexed scientists and investors.

The medication, resmetirom, was approved under the brand name Rezdiffra for patients with stage 2 and 3 fibrosis. It’s expected to be available in April, according to Madrigal. While the FDA described the disease as NASH in its label, it is now often referred to as metabolic dysfunction-associated steatohepatitis (MASH).

The company declined to comment on the price it will charge for Rezdiffra, its first approved drug. Earlier this year, CEO Bill Sibold touted resmetirom as a specialty drug that “provides tremendous value” in a high-need area and would be priced as such. ICER, a drug pricing watchdog, determined in May that the drug would be cost-effective if it was priced between $39,600 and $50,100 per year.

In an interview before the approval, Sibold told Endpoints News that Madrigal will initially focus on the roughly 315,000 MASH patients in the US who have stage 2 or 3 fibrosis and are being seen by hepatologists and gastroenterologists.

“They’ve been diagnosed. They’re with the right physicians who know the disease. They’ll understand the product and know how to follow these patients,” he said. “Let’s focus on those patients and give them something because they haven’t had anything.”

The approval is likely to be viewed as a crucial milestone in the treatment of nonalcoholic steatohepatitis (NASH), which is now referred to as metabolic dysfunction-associated steatohepatitis, or MASH. For years, companies have tried to bring treatments to market, only to be foiled by negative readouts or safety questions.

A ‘huge moment’ for MASH

“This is one of those diseases that industry has tried for years to find a solution,” Sibold said. “To be the first, it’s really a huge moment for patients, a huge moment for the medical community, a huge moment for industry, a huge moment for Madrigal.”

He’s optimistic about access and said Madrigal has had “extremely productive conversations” with health insurers.

“Payers also understand what the cost of NASH is as it progresses along,” he said, noting that some patients develop liver cancer or eventually need a transplant.

Madrigal’s drug follows the high-profile failure of a product that once led the field — and helped inspire it. In 2014, Intercept Pharmaceuticals’ early data readout for its experimental drug, obeticholic acid, helped put MASH on the map as a disease that offered a huge number of patients and no approved treatments. The readout triggered a surge of interest from investors and the medical community.

But it never made it across the finish line. The FXR agonist was rejected by the FDA for a second time last year after members of an advisory committee raised safety concerns. Shortly after the rejection, Intercept scuttled its MASH programs and sold itself to Alfasigma, with analysts highlighting the importance of a “pristine” safety profile.

Madrigal’s drug works a bit differently than Intercept’s. It’s designed to activate the thyroid hormone beta-receptor in the hopes of reducing a patient’s liver fat, inflammation and fibrosis, while also lowering their cholesterol.

It met both primary endpoints in a Phase III study, helping patients achieve MASH resolution with no worsening of fibrosis, and fibrosis reduction with no worsening of the nonalcoholic fatty liver disease (NAFLD) activity score, a widely-used metric that tracks changes in patients with nonalcoholic liver disease, including MASH.

About half of the patients treated with 100 mg of resmetirom and biopsied at 52 weeks showed MASH resolution or fibrosis improvement, Madrigal announced in February.

There was “no incidence of drug-induced liver injury,” the safety concern that worried FDA advisors about Intercept’s drug. The FDA did not require an adcomm for resmetirom.

The first, but not likely the last Rezdiffra is now the only approved treatment for MASH patients. Previously, patients have been told to make lifestyle changes such as diet and exercise to avoid the need for a liver transplant.

“It’s just an awful thing to have them say, ‘Well, you have cirrhosis, and I’m sorry. We have no treatment,’” said Wayne Eskridge, a MASH patient and founder of the Fatty Liver Foundation, which has received contributions from MASH drug developers. “For patients coming on that will be diagnosed over the next few years, just not having to have that terrifically negative interaction is awesome.”

But he doesn’t think Madrigal’s medication will be the only option for long.

“With FDA, you never know,” Eskridge said. “But there’s been good progress and research. So we’re hoping that in the next two or three years, we see some other drugs as well to give broader treatment options for patients.”

He expects a class of drugs called FGF21s will pose the greatest competition to Rezdiffra, including a pair of late-stage therapies in development by Akero Therapeutics and 89bio. FGF21 is an endogenous metabolic hormone, and enhancing its activity has been shown to improve a list of symptoms, including hepatic fibrosis and inflammation. 89bio recently launched a Phase III trial for pegozafermin, while Akero’s efruxifermin is in an ongoing Phase III trial.

Akero recently unveiled additional data from its Phase IIb study suggesting that MASH patients treated with efruxifermin saw improvements in fibrosis without worsening of MASH through week 96. And Novo Nordisk and Eli Lilly are also testing their respective GLP-1 drugs, semaglutide and tirzepatide, in MASH.

In a trial readout in February, Eli Lilly reported that 74% of participants who took tirzepatide in a Phase II study showed an absence of MASH with no worsening of fibrosis at week 52, compared to about 13% of patients on placebo. The patients had stage 2 or 3 fibrosis.

Sibold previously suggested GLP-1s may perform best in early-stage MASH, before there is fibrosis or significant fibrosis, while later-stage patients “are in need of a liver-directed therapy quickly.”

당시에 MDS (myelodysplastic syndrome)에 대한 임상3상 결과가 좋아서 FDA 승인이 기대가 되는 상황이었습니다. 오늘 FDA의 Advisory Committee Meeting이 있었는데 12:2로 승인을 하는 쪽으로 결론이 났습니다. 물론 FDA가 이 결정에 따룰 이유는 없지만 그래도 최종 결정에 긍정적인 결과를 주리라고 기대합니다.’

현재 MDS의 치료제로는 erythropoiesis-stimulating agents (ESA)가 거의 유일한 치료제라고 해도 무방한데 Geron은 Imeltestat을 ESA에 듣지 않는 환자들에 대한 치료제로 승인 요청을 할 예정입니다. Imetelstat에 대한 PDUFA date는 6월 16일입니다.

Members of the FDA’s Oncologic Drugs Advisory Committee voted 12 to 2 on Thursday that the benefits of Geron’s imetelstat outweigh safety risks for the treatment of certain anemic myelodysplastic syndrome (MDS) patients who are dependent on blood transfusions.

While regulators raised concerns around cases of cytopenia, or low levels of white blood cells or platelets, advisory committee members said they were confident that the risks appear manageable. The FDA noted on Thursday that there was a “notably higher” incidence of neutropenia and thrombocytopenia in the imetelstat arm of a Phase III trial.

“Though I am concerned about the risks in this total trial population — in other words, not just the responders — I do believe it is more likely than not that there is a quality-of-life benefit here that is real,” University of Colorado associate professor Christopher Lieu said.

Stanford University School of Medicine professor Ranjana Advani added, “The community of doctors who take care of these patients know how to manage these side effects.”

Members also pointed to the fact that imetelstat met its primary endpoint in a Phase III trial, helping patients achieve eight-week red blood cell-transfusion independence, as well as a key secondary endpoint measuring 24-week independence.

MDS occurs when the normal production of blood cells is disrupted. Most patients with lower-risk MDS experience anemia, which can cause symptoms ranging from fatigue to irregular heartbeat and has also been linked to shorter survival. Those with severe anemia may be dependent on continuous transfusions. Patients who spoke during the adcomm stressed that frequent transfusions impacts their quality of life.

Ravi Madan, a senior clinician head at the National Cancer Institute’s Center for Cancer Research, was one of two members who voted against imetelstat’s benefit-risk analysis.

“I interpreted the question pretty strictly,” he said. “Even low-risk MDS patients are at high risk from their disease, but they shouldn’t also be at risk from their treatments as well.”

The FDA also raised concerns in briefing documents published in advance of the meeting that a majority of patients in the only randomized efficacy trial for imetelstat were enrolled outside of the US. Geron’s chief medical officer Faye Feller acknowledged that a majority of patients were from the EU, but assured the committee that “overall, the demographics are representative of the US MDS population.”

Traditionally, a class of drugs called erythropoiesis-stimulating agents (ESA) have been used off-label to treat lower-risk MDS patients with transfusion-dependent anemia. Bristol Myers Squibb’s Revlimid and Reblozyl are approved to treat anemia in MDS patients, and last year Reblozyl won a label expansion for first-line lower-risk patients who may require transfusions.

But Vanderbilt University School of Medicine professor Michael Savona, who was a member of the steering committee for imetelstat’s Phase III trial, said the use of those drugs is restricted to specific subgroups of patients.

“After failure of ESAs there is no good therapy for most patients,” he said during the meeting.

Geron is seeking approval for patients who have failed on or are ineligible for ESA treatment.

Johnson & Johnson saw early potential in imetelstat, shelling out $35 million upfront and promising another $900 million in milestones to partner on the drug a decade ago. The company backed out of the collaboration four years later, citing “a strategic portfolio evaluation and prioritization of assets.”

GRO Biosciences Inc. today announced that the company has secured $2.1 million in a seed funding round led by Digitalis Ventures and joined by Eric Schmidt’s Innovation Endeavors. The funds will support buildout of bioprocess development for GRO Biosciences’ platform of genomically recoded bacteria for the production of therapeutic proteins with enhanced properties, such as increased potency and stability, and improved targeting and delivery into cells and tissues.

GRO Biosciences was co-founded by the following:

George M. Church, Ph.D., professor of genetics, Harvard Medical School, will serve as head of the company’s scientific advisory board.

Andrew D. Ellington, Ph.D., professor of biochemistry, University of Texas at Austin, will serve on the company’s scientific advisory board.

Daniel J. Mandell, Ph.D., will serve as the company’s CEO.

Christopher J. Gregg, Ph.D., will serve as the company’s chief scientific officer.

P. Benjamin Stranges, Ph.D., will serve as the company’s principal scientist.

Marc J. Lajoie, Ph.D., and Ross Thyer, Ph.D., will serve the company in advisory roles on a consulting basis.

By recoding the genomes of bacterial strains used in biologics production, GRO Biosciences can expand beyond the 20 amino acid building blocks typically found in proteins to introduce non-standard amino acids that can customize the shape and chemical properties of the protein.

“For decades, bacteria have been used as the workhorses of the biotech industry in the production of blockbuster therapeutics, and we believe that we can dramatically expand their utility by recoding their genomes,” said Dr. Church. “GRO Biosciences’ technology addresses the fundamental limitations of producing proteins with non-standard amino acids, opening up the possibility of creating a new universe of designer proteins with enhanced therapeutic properties at commercial scale.”

Nearly all monoclonal antibodies, as well as many other therapeutic proteins, such as interferon, human growth hormone and insulin, used to treat common chronic conditions, rely on disulfide bonds to maintain their 3-dimensional structure needed for biological activity. However, disulfide bonds are not stable in the presence of reducing agents found in cells and in blood, which means that the therapeutic effect of the proteins is short lived after administration to the patient.

(Picture: Andrew D. Ellington at University of Texas at Austin)

GRO Biosciences is addressing the challenge of therapeutic protein instability by replacing disulfide-bond-forming cysteine amino acid residues with selenocysteine, a naturally-occurring amino acid that is rarely incorporated into proteins, but is found in the cell. Selenocysteine has a structure and chemical properties very similar to cysteine, however diselenide bonds are stable under the same conditions where disulfide bonds are not, leading to a much longer half-life of the therapeutic protein.

“Protein therapeutics represent a $180 billion market, yet product stability, targeting and delivery into the cell still remain significant challenges to be addressed if we are to enhance the patient experience, achieve better compliance and improve health outcomes,” said Geoffrey W. Smith, founder and managing partner of Digitalis Ventures. “If GRO Biosciences can make a therapeutic protein product that is more stable and requires less frequent dosing, then that is a win for patients and the healthcare system.”

GRO Biosciences is taking advantage of redundancies in the genetic code to reassign redundant codons to new, non-standard amino acids. For example, there are three different stop codons which are responsible for halting the elongation of a growing protein: UAG, UAA and UGA. GRO Biosciences has developed a recoded strain of bacteria that has replaced all of the UAG stop codons with UAA stop codons and reprogrammed the UAG codon to new amino acids such as selenocysteine. By replacing all codons that code for cysteine residues in a protein with UAG, selenocysteine can be selectively incorporated in place of cysteine residues to form stabilizing diselenide bonds.

“GRO Biosciences is literally reprogramming biology,” said Dror Berman, Managing Partner of Innovation Endeavors. “What I find most compelling is their ability to converge game-changing synthetic biology with powerful computational design to create a new class of living organisms, unlocking unprecedented capabilities in medicine, materials and biotechnology.”

GRO Biosciences has established preliminary proof of concept of its platform by producing diselenide stabilized antibody products as well as therapeutic proteins, such as human growth hormone, in its selenocysteine recoded bacteria. In all instances, yields were high, selenocysteine incorporation at the desired sites was 100 percent, and all diselenide bonds formed correctly leading to the properly folded protein. The diselenide bonds dramatically increased stability in physiologically relevant conditions, as confirmed by functional assays.

Many of the protein therapies available now, as well as many more still in development, got their start on computers. Software identifies the protein shapes best suited for therapeutic applications and those designs are tested in a lab. While computational techniques have advanced the design and development of new therapeutic proteins, even the most advanced of these are limited to 20 standard amino acids found in nature that are building blocks of all proteins. Harvard University spinout GRO Biosciences aims to improve protein therapies by expanding this amino acid alphabet.

GRObio has been quietly developing its technology for the past several years. The company has made progress in its preclinical research and it’s now positioning itself to advance its own therapies, and to strike up partnerships with pharmaceutical companies interested in working with the startup’s technology. To support those efforts, GRObio announced on Wednesday a $25 million Series A round of funding co-led by Leaps by Bayer and Redmile Group.

The science behind GRObio comes from the lab of George Church, a Harvard scientist whose discoveries have led to the founding of many life sciences startups. Dan Mandell, GRObio’s co-founder and CEO, was a research fellow in genetics at Harvard, where he worked with Church on computational design of new proteins whose folding and function depends on this new amino acids alphabet, comprised of non-standard amino acids (NSAAs).

Therapeutic proteins are produced by harnessing the protein-translation machinery of bacteria. Companies such as Ginkgo Biosciences, Synlogic, and Absci work with E. coli to produce their commodity chemicals and proteins. For many synthetic biology companies, E. coli are the bacteria of choice because they are inexpensive and easy to use, Mandell said. GRObio also works with an E. coli-based organism. But the company has gone further than what nature provides by recoding the E. coli genome so that these bacteria are able to produce proteins by using NSAAs. GRObio calls these bacteria “genetically recoded organisms,” or GROs.

“What’s special about these organisms is they can make proteins comprised of amino acids beyond the 20 standard amino acids,” Mandell said. “These organisms are the only organisms that can produce these NSAA proteins at high efficiency, and at scale.”

So why would anyone want a GRO-produced protein made from NSAAs? Mandell said that therapeutic proteins made with standard amino acids still have limitations ranging from safety issues to the durability of the treatment. Working with NSAAs enables the production of customized proteins whose shape and chemical properties offer advantages for a biologic drug.

GRObio is working with two families of NSAA chemistries so far. The first, which the company calls DuraLogic, makes a protein that is more stable and improves its half-life. Currently available biologic drugs dosed as frequent injections are inconvenient or undesirable (or both), which leads many patients to miss doses, Mandell said. By making a more stable protein, GRObio could produce a drug whose therapeutic effect lasts for a longer period of time, which means a protein therapy that requires less frequent injections.

The second NSAA family, which GRObio has dubbed ProGly, enables the biotech to directly modulate the immune system, offering a new way to address autoimmune diseases. The way the immune system distinguishes a foreign protein from one that is part of the body is by detecting sugar molecules called glycans on the protein’s surface, Mandell said. GRObio aims to express proteins decorated with human glycans, which would reeducate the immune system to recognize them as belonging to the body.

GRObio hasn’t disclosed what diseases it aims to address, other than to say the technology has applications in autoimmune and metabolic disorders. One of the company’s early projects was a form of insulin modified in a way to enable weekly dosing. The company wasawarded a Phase I Small Business Innovation Research grant in 2019 for that research, followed by a Phase II grant in 2020. Mandell acknowledged that GRObio has worked on insulin, and said the company has received about $1.5 million in non-dilutive capital to support that work.

Without specifying a disease target, Mandell said he expects GRObio could begin its first human tests of a GRO-grown therapeutic protein in 2024. The new financing will support the preclinical research leading up to those tests. GRObio is also looking for pharmaceutical industry partners. Those partners could license GRObio therapeutic candidates, taking on the responsibility of clinical development and potential commercialization of new protein therapies.

Mandell said GRObio is also considering alliances with companies that want to work with NSAAs but can’t because they don’t have access to a production platform that can produce NSAA-based proteins at scale. Mandell said GRObio has been approached by companies that have already designed their own new molecules and are looking at GROs as a way to produce them.

Prior to Wednesday’s funding announcement, GRObio had raised $2.1 million in a 2017 seed financing led by Digitalis Ventures and Innovation Endeavors. Those firms also joined the Series A round, bringing the startup’s total investment to $31.2 million to date.

Genomics and synthetic biology pioneer George Church, PhD, says GRO Biosciences (GRObio), a developer of enhanced protein therapeutics he co-founded based on platform technology discovered in his Harvard Medical School lab, reflects a truism about startup formation.

“Every postdoc has an invention, but not every invention is something that we want to immediately launch,” Church, who heads GRObio’s scientific advisory board, observed recently on “Close to the Edge”, GEN Edge’s video interview series. “We try to incubate them as long as possible inside the lab until we’re sure that they’re mature enough so that we won’t get diluted out immediately by running out of VC [venture capital] money.”

GRO stands for “genomically recoded organisms”—the first production organisms made with modified genomes and engineered protein translational machinery, according to the company.

By recoding the genomes of bacterial strains used in biologics production, GRObio reasons that it can expand beyond the 20 amino-acid building blocks typically found in proteins to introduce non-standard amino acids (NSAAs) that can customize the shape and chemical properties of the protein.

“What we do is to systematically alter the genetic code,” Daniel J. Mandell, PhD, who is GRObio’s CEO, summed up to GEN Edge.

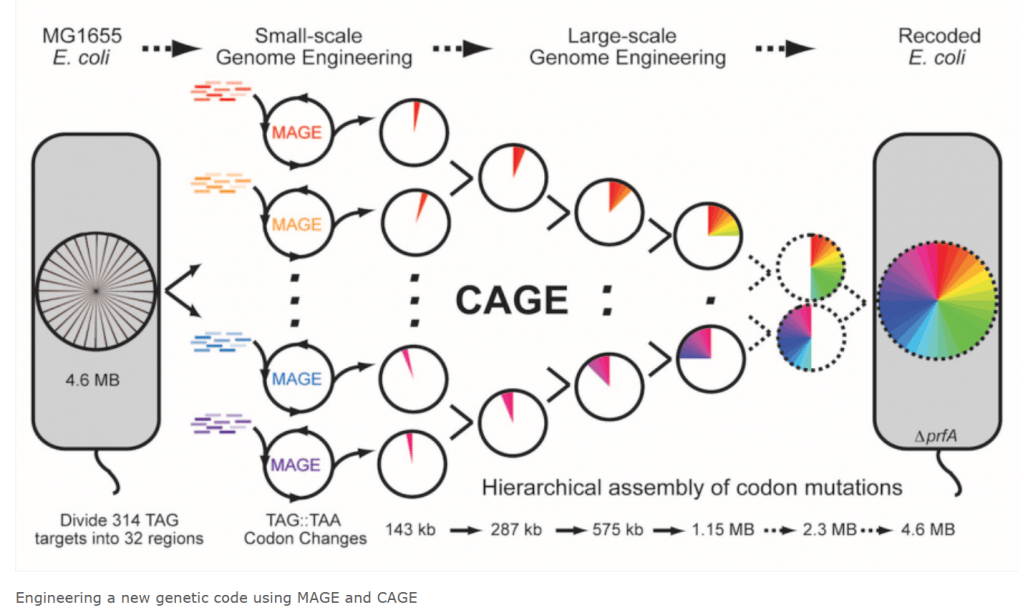

Church’s Harvard Medical School lab first described and characterized GROs in a paper published in 2013 in Science.

In 2015, Church, Mandell and seven co-authors reported in Nature their successful computational redesign of essential enzymes in the first organism possessing an altered genetic code, conferring metabolic dependence on NSAAs for survival.

The following year, Church led a research team in applying recoding to design and synthesize a bacterial genome, an exercise designed to show how new organisms could be created that feature functionality not previously seen in nature.

Also in 2016, Church, Mandell, and four others co-founded GRObio to commercialize the technology by developing protein therapeutics based on computational protein design and synthetic biology technologies. Among the co-founders are Andrew Ellington, PhD, whose lab at the University of Texas at Austin focuses on developing novel genetic codes and synthetic organisms based on engineering the translation apparatus; and Christopher Gregg, PhD, GRObio’s chief scientific officer (CSO).

Mandell was wrapping up a PhD in computational protein design at University of California, San Francisco, about a decade ago, and seeking a postdoctoral position when he came across Church’s research on GROs.

“It was an epiphany”

“For me it was an epiphany: Now we can go beyond the 20 amino acids and build designer proteins that can carry out almost any function. I came to George’s lab to bring these two worlds together of computational protein design and genome-wide recoding,” Mandell recalled.

Daniel J. Mandell, PhD, GRO Biosciences co-founder and CEO

“We did some early work demonstrating that you can in fact predictably engineer proteins whose folding and function depend upon non-standard amino acids, to convince ourselves that we really can do this in a rational way. That’s when we turned our attention to the question of what are the outstanding problems in the clinic that we might address using that technology.”

Mandell joined Church’s lab within a year of Gregg joining: “We very quickly realized we both had entrepreneurial designs and mesh very well, and we put a lot of time into thinking about how we could try to commercialize this technology.”

Gregg, now GRObio’s CSO, was pursuing a PhD in glycobiology, studying how glycans interact with the immune system. He started a short-lived synthetic biology startup focused on biofuel, before switching gears to integrating synthetic biology with organism and genome design.

“Luckily, I was able to get George’s interest in my thesis, which had to do with glycobiology and human-specific disease preponderances,” Gregg recalled. “I came in as the organism [GRO] was getting finished. It was just such a ripe platform for trying new things and solving new problems. Then when Dan and I realized that we had the same interests, we just started running with it.”

That pursuit paid off for GRObio last month, when it completed a $25-million Series A financing co-led by Leaps by Bayer and Redmile Group. Redmile is a San Francisco venture and private equity investment firm. Leaps is the equity investment arm created by Bayer to establish new companies and invest in early-stage technologies with breakthrough potential to “fundamentally change the world for the better.”

Bayer came to invest in GRObio, Mandell said, through relationships he had with the pharma/consumer goods/agbio giant and contacts from GRObio’s network of investors. Among investors joining the financing were Digitalis Ventures and Innovation Endeavors. (The Series A brings total investment in GRObio to $31.2 million so far.)

Proceeds from the financing, GRObio said, will support development of its GRO platform, a scale-up of bioprocess manufacturing, preclinical validation studies, and IND-enabling studies for GRObio’s pipeline of NSAA protein therapeutics designed to treat autoimmune and metabolic diseases.

“These are just initial focus areas,” says Mandell. “Autoimmune disease and metabolic diseases are a really a small part right of this broader universe [of opportunities]. But there are specific indications in there that we’re focusing on.” The company isn’t yet disclosing those indications, except to say they will address unmet clinical needs.

Beyond the pipeline

Taking this universe of NSAA chemistries, Mandell and colleagues want to ask some big questions. “Which problems really can’t be solved in the clinic without this new expanded universe of chemistries at the amino acid level? Some of these problems have interesting-looking solutions coming down the clinical development pipeline,” Mandell said. “That’s not really where we want to play. We want to play in areas where we think we can solve Holy Grail challenges and there isn’t another way to go about this.”

GRObio has constructed a “biofoundry” consisting of proprietary computational protein design and robotics pipelines, with the aim of streamlining development of NSAA translational machinery and NSAA protein products. The biofoundry applies strain and genome engineering, automation, analytics, and protein design software to build uniquely scalable NSAA protein “factories” from trillions of candidates.

GRObio emerged from stealth mode in 2017, raising $2.1 million in seed funding led by Digitalis Ventures, with participation from Innovation Endeavors, the venture capital firm whose co-founders include Eric Schmidt, Google’s former CEO and later executive chairman of Google and its parent company, Alphabet Inc.

From three people when it started, GRObio has since grown its staff to 16 people. “We will double in size by 2023,” Mandell said.

GRObio hopes its alphabet-expanding approach will enable it to grow its own significant share of a protein therapeutics market that according to Market Research Future (MRFR) is expected to increase over the next six years at a compound annual growth rate of 6.86%–for a nearly 60% rise to about $290.69 billion in 2027 from $182.69 billion this year.

GROs are intended for high-efficiency, commercial-scale production of proteins with NSAAs. These NSAAs are intended to enhance protein therapies with capabilities such as unprecedented duration of action and more precise control of the immune system.

GRObio is building its pipeline by advancing its first two product families of NSAA platform chemistries: DuraLogic™ is designed to enable flatter pharmacodynamic profiles and relaxed dosing schedules, while ProGly™—short for “programmable glycosylation”—are designed to produce biologics that enable the immune system to treat autoimmune disease, or to eliminate immunogenic side effects of protein-based therapies.