The power of luck!: 겸손하라. 성공경험이 있다고 그것이 계속되는 것은 아니다.

Life is short… live by the NAR: 함께 일하고 싶은 사람들은 다른 사람을 존중할 줄 아는 사람이다.

By the time you know you need a leadership change, you’re probably late: 경영진 교체는 주저해서는 안된다.

Surround yourself with data-driven truth-seekers: Go/No-Go 결정을 해야할 때 데이터에 정직하게 대응할 줄 아는 경영자가 중요하다.

I’ve had CEOs do that in the past: “we saw an on-target tox signal and although we could ask to pull the next tranche, we think we should shut it down.” There are many variants of that – but fundamentally it’s truth-seeking and data-driven…truth-seekers are trying to learn from the data and be disciplined even if it means a “no-go” decision.

The best CEOs understand and are aligned with their current shareholders: 좋은 경영자들은 증자보다 파트너쉽을 통해 회사 가치를 증대함으로써 현재의 주주들을 위해 일하려고 노력한다.

They understand that a CEO represents current owners, not future owners, and so are both disciplined on raising capital and exploring alternatives to equity sales (like when asset dilution through partnerships is a better alternative).

Most CEOs are either openers or closers, rarely both: 딜을 잘 만들어 내는 성향과 딜을 꼼꼼히 마지막까지 체결하는 성향을 동시에 가진 CEO는 없기 때문에 좋은 팀을 구성해야 한다.

Build lean organizations by encouraging teams to “earn the right” to grow: 몸집을 최소화해서 역량을 결과에 집중하라. G&A 팀을 키우지 않도록 주의하라.

Fractional leadership in a startup works until it doesn’t: 파트타임이나 컨설턴트로 CEO, CBO, CMO, CFO 등을 운용하는 것은 시리즈 A 이전까지만이다. 시리즈 A를 마치면 풀타임으로 전환해야 한다.

Leadership coaches/advisors are valuable for all types of performers: 리더쉽 코칭이 중요하다.

Build authentic multi-faceted relationships with people in your biotech community: 일만 해서는 안된다. 삶의 다양한 면 – 가족, 취미 등 -에 대해서도 다방면으로 친해져야 한다.

역시 이번에도 많이 배웁니다. 특히 마지막 부분에서 소셜 이벤트를 회사 생활의 한 부분으로 생각을 했는데 그게 아니군요. 삶을 함께 살아가는 인생의 동반자를 만나가는 과정으로 스타트업을 보내요. 이런 점은 정말 배워야 할 것 같습니다.

요즈음 In vivo CAR-T가 마치 대세처럼 거의 모든 제약회사와 바이오텍 기업들이 경쟁적으로 뛰어들어 오고 있습니다. 본래 CAR-T의 T 세포가 고형암에서 약점을 내포할 수 있다는 점 때문에 다른 세포를 고형암 치료를 위해 사용할 수 있는지 연구가 진행되었는데요 그 중의 하나가 Macrophage를 이용한 CAR-M이었습니다. CAR-M 치료제를 개발할 목적으로 세워진 Carisma Therapeutics의 스토리를 공부하면서 글을 써보려고 합니다.

Carisma Therapeutics (formerly CARMA Therapeutics)는 2016년에 Michael Klichinsky와 Saar Gill에 의해 시작되었습니다. Michael Klichinsky 박사는 Saar Gill 교수와 Karl June 교수 지도하에 박사과정을 하고 있었는데 그 기간동안에 CAR-Macrophage에 대한 발견을 하게 되었고 이 결과를 바탕으로 회사를 설립한 것입니다. 이 회사의 기반이 된 CAR-M 기술을 보고한 Nature Biotechnology 논문은 아래와 같습니다.

UPenn’s Penn Center for Innovation (PCI) helped Saar and I initiate the process of founding the company – from forming an LLC to initiating our fundraising efforts. The company grew as we raised a Seed Round and eventually a Series A in 2018, with support from a fantastic team of investors that believe in the potential for myeloid based cell therapy of solid tumors.

UPenn의 PCI에서 LLC 설립부터 Seed round, Series A까지 도와주었다고 합니다.

잘 나가는가 하더니 갑자기 2024년 4월에 직원을 37% 정리해고하고 프로그램을 크게 변경시켰습니다. CT-0508의 임상1상을 중단하였고 대신 CT-0525로 대체하고 Moderna와 진행 중인 In vivo CAR-M 치료제 개발로 우선순위를 변경하기로 한 것입니다. 그리고 개발 중이던 Ex-vivo anti-Mesothelin CAR-M 치료제인 CT-1119의 전임상 연구도 중단한다고 발표했습니다.

그리고 6개월만에 다시 34%의 인력 구조조정을 진행합니다. CFO, general counsel 및 SVP HR도 포함된 구조조정이었습니다. 이 결정은 사실 좀 이해하기 어렵습니다. CT-0525의 임상시험 중단을 결정하였습니다. 이로써 모든 임상시험을 중단하게 된 것입니다. 이미 6명의 환자 등록이 마쳤고 확대할 단계였는데 전략적인 결정에 의해 갑자기 중단이 된 것입니다.

The company said the anti-HER2 cell therapy was safe and well-tolerated, but the discontinuation decision was rooted in an assessment of the current competitive landscape, including recently approved anti-HER2 therapies on HER2 antigen loss and downregulation.

The Company will assess a full range of strategic alternatives, including but not limited to, the sale, license, monetization, and/or divestiture of one or more of the Company’s assets or technologies, a strategic collaboration, partnership, or merger with one or more parties, or the sale of the Company. The Company’s exploration of strategic alternatives may not result in the consummation of any transaction or the realization of any value for the Company or its stockholders.

Pipeline Updates

Fibrosis

Our liver fibrosis program is based upon the discovery of a key efferocytosis defect in the macrophages that reside within the livers of patients with fibrosis. Using a novel mRNA/LNP approach, our product candidate, CT-2401, aims to reverse fibrotic disease and improve the outcomes of patients with advanced liver fibrosis.

In the second quarter of 2024, we achieved pre-clinical proof of concept in our liver fibrosis program, demonstrating the anti-fibrotic potential of engineered macrophages in two liver fibrosis models.

CT-2401 has the potential to be a first-in-class efferocytosis therapy for advanced metabolic associated liver disease.

In Vivo Program (Moderna Collaboration)

In June 2024, we announced that Moderna nominated the first development candidate under the collaboration, which targets Glypican-3, or GPC3.

In November 2024, we announced new pre-clinical data on our anti-GPC3 in vivo CAR-M therapy for treating hepatocellular carcinoma. These pre-clinical data demonstrated robust anti-tumor activity.

In February 2025, Moderna nominated ten additional oncology research targets and ceased development of two oncology research targets and two autoimmune research targets.

As of February 2025, Moderna has nominated all 12 oncology research targets under the collaboration for which we have the potential to receive future milestones and royalty payments.

The Company will not conduct any additional research activities under the collaboration agreement, and we will not be receiving any further research funding from Moderna under the collaboration agreement.

Moderna agreed to terminate the in vivo oncology field exclusivity, which would allow us to pursue in vivo CAR-M programs outside of the 12 nominated oncology targets and product polypeptides.

Corporate Update

On March 25, 2025, the Company’s Board of Directors approved a revised operating plan focused on evaluating strategic alternatives and preserving capital.

The Company has reduced operations to core functions necessary to support this strategic review and has paused all research and development activities at this time, pending the outcome of the review.

The Company may engage external advisors to support the evaluation of strategic alternatives and prepare for a potential wind-down of operations, if necessary.

결국 Moderna와의 Exclusive deal이 종료되면서 Carisma Therapeutics는 모든 연구 프로그램을 중단하고 전략적인 대안을 찾기로 했다는 것입니다. 무슨 전략적인 대안인가요?

곧 이어서 발표한 계획은 충격적인 거의 전직원 해고였습니다. 46명에서 6명으로 줄인다고 발표를 한 것입니다.

The macrophage-focused therapeutics company is in the process of “identifying and evaluating potential strategic alternatives with the goal of maximizing the value” of its remaining drug candidates. These assets include CT-2401, an off-the-shelf, in vivo mRNA/LNP, which the biotech has touted as having the potential to be a first-in-class efferocytosis therapy for advanced metabolic-associated liver disease.

There’s also CT-1119, a mesothelin-targeted CAR-monocyte Carisma had been teeing up for a phase 1 trial in China in combination with BeiGene and Novartis’ tislelizumab in patients with mesothelin-positive solid tumors.

그리고 2개월 후에 Ocugen의 자회사인 OrthoCellix와 Reverse-Merger를 발표합니다. 결국 회사가 CAR-M을 완전히 포기하는 상황에 이른 것입니다.

OrthoCellix failed to secure commitments for shares of at least $25 million by Sept. 15, as required by the merger terms, prompting Carisma to ax the agreement…In the meantime, the beleaguered Philadelphia biotech is receiving a $4 million payout from Moderna as the mRNA company cuts ties with its former partner.

이 합병 결정은 결과적으로 매우 좋지 않은 결정이었던 것으로 판명이 났습니다. OrthoCellix가 $25 Million의 펀딩을 유치해야 하는데 그것을 하지 못한 것이면서 그래서 합병결정은 최종적으로 결렬되었고 이 결과 결국 회사는 나스닥에서 상장폐지가 되어 버리고 말았습니다.

참으로 안타까운 상황이 아닐 수 없습니다. 결국은 경영진의 잘못된 결정으로 임상시험을 조기에 중단하면서 추가펀딩의 기회를 놓쳐 버렸고 CAR-Macrophage이든지 CAR-Monocyte이든지 Ex vivo이든지 In Vivo 이든지 상관없이 회사는 1년 사이에 갑자기 사라져 버린 것입니다.

CAR-M 자체는 어떤 임상시험에서의 문제점을 노출하거나 한 적이 없습니다. 다만 개발이 진행되지 못한 것이죠. 가장 최근에 Carisma Therapeutics에서 내놓은 회사 프리젠테이션을 공유합니다.

제 소개에도 남기기는 했지만 저는 2000년부터 2002년까지 약 2-3년간 한국에서 벤처캐피탈리스트로서 바이오텍 기업에 투자를 하는 일을 한 적이 있었습니다. 주로 여의도 증권가와 광화문에서 투자자로 일을 했었죠. 당시는 아직 지금처럼 강남에서는 투자회사가 그리 많지 않았고 주로 강북의 여의도를 중심으로 해서 밀집해 있었습니다. 그리고 2002-2003년은 바이오텍 중 하나의 독일법인에서 일을 하면서 유럽의 빅파마 기업들과 비즈니스 관련한 미팅을 하면서 그들의 수요를 배울 수 있었고 어느 독일대학교의 교수연구실과 공동연구를 통해서 새로운 표적의 물질을 개발하는 일을 진행하기도 했습니다. 이렇게 지낸 약 3년간의 생활은 제가 그 이후 지금까지 미국으로 넘어와서 바이오텍에서 평생(?)을 연구원으로 살면서도 시장과 자본이라는 두 축을 항상 염두에 두고 살 수 있도록 도와줌으로써 제가 단순히 과학자로만 안주하지 않도록 저를 일깨워주고 단련시켜 주었습니다.

보스턴 지역에 여러 벤처캐피탈리스트가 있지만 그 중 한분으로 잔뼈가 굵은 분으로 자타가 공인하는 분은 Bruth Booth 박사님이 계십니다. Bruce Booth 박사님은 투자도 왕성하게 하시지만 회사 투자의 성공이나 실패에 대해 꾸준히 블로그를 쓰시고 계십니다. 이 분이 보스턴의 초기 바이오텍 스타트업을 만들고 투자하는 Atlas Ventures의 Partner이신데 2005년에 시작해서 20년이 지난 지금까지 자신의 소회를 3부에 걸쳐서 남기셨습니다. 이 분의 말씀을 좀 나누어 보려고 합니다.

Over the course of the first nine years after joining, we retooled ourselves from a global multi-office, multi-sector firm into a biotech-only VC based in Cambridge MA.

본래 Atlas Ventures는 다국적, 여러 섹터에 투자하는 VC였는데 지금은 케임브리지 지역에서 바이오텍만 투자하는 VC로 바뀌었다고 합니다.

Science-first opportunism beats top-down strategy for deal selection: Top-down approach보다는 과학에 근거한 bottom up approach가 좋은 결과로 이어졌고 여기에 더해서 disease-agnostic approach가 유효했다고 하십니다.

Don’t believe what you read in science papers at face value: 과학논문의 결과가 재현성에 문제가 있는 경우가 많았기 때문에 wet-experiment를 통해 seed stage NewCo를 거치는 전략을 통해 재현성이 결여된 과학적 가설을 일찍부터 제거할 수 있었다고 하십니다.

Don’t over-value reductionism, but also avoid phenotypic over-enthusiasm: 표적에 대한 이해가 중요하다고 말씀하십니다.

Rare disease drug development isn’t as “easy” as it seems on paper: 희귀질환치료제 개발이 개발비용이 저렴하고 비교적 빠르다고 알려져 있지만 실상은 그렇게 쉽지 않다고 말씀하십니다.

The single most important value creation activity in biotech is excellent clinical trial execution: 임상시험에서 회사의 CMO와 CRA들의 임상시험 현장에서의 참여와 이해가 매우 중요하다는 점을 강조하고 계십니다. 임상시험의 아웃소싱에 대한 염려와 함께.

Novelty is great, but only when it’s unlocking something truly valuable to patients: 신규라고 할 때 임상결과에서 의미있는 신규성이 중요한 것이지 과학적 신규성이 아니라는 점을 강조하십니다. 예를 들면 .Undruggable을 Druggable로 만들 수 있는 것과 같은 것이 필요하다는 것입니다.

Be skeptical, as most things fail, but embrace “a permission to believe”: TPP (Target Product Profile)과 DC (Drug Candidate)가 어떠해야 하고 초기 임상 시험에서 어떤 결과를 얻어야 하는지에 대한 정확한 이해가 전제가 되어야 한다고 강조하십니다.

Understand the real risk you are underwriting and the value of discharging it: 임상적 차별성, CMC risk 등의 중요성을 잘 이해해야 한다고 말씀합니다.

Seek the scientific truth, not just “making money”: 과학적 진실에 다가가려는 노력을 하라고 말씀하십니다.

Innovation and optimism are tightly interconnected – and have been ever present in biotech

오늘 과학에 대한 Bruce Booth 박사님의 글을 전체적으로 보았을 때, 결국 (1) 초기 과학논문결과가 재현되는지 확증하는 것의 중요성 (2) 표적에 대한 정확한 이해 (3) 임상에서 유의미한 차별점을 얻기 위한 노력과 (4) CMC 등 다각도의 문제를 종합적으로 이해하고 접근해야 한다는 점을 강조하신 것으로 보입니다.

항상 Top-down이 좋으냐 Bottom-up이 좋으냐 이런 논쟁이 있는데 결국 좋은 과학적 발견으로 부터 시작하는 것이 옳바르다는 것을 배울 수 있어서 큰 배움이 되었습니다.

보통 매주 토요일은 아내와 골프를 치기로 되어 있는데 이번주가 두사람 모두에게 좀 일이 많았던 주였기도 하고 날씨도 쌀쌀해서 가벼운 산책과 코스코에서 함께 장을 보는 것으로 함께 시간을 보내는 것으로 했습니다.

이렇게 시간이 좀 나게 되니까 생각을 좀 더하게 되고 블로그도 좀 쓸 수 있게 되었습니다. 텔레비전을 끄고 이러저런 생각과 대화를 하다 보니 뜻밖에 좀 생각해 볼 주제에 대해 듣게 되었습니다. 그것은 관계에 대한 이야기인데요 놀랍게도 벤처캐피탈리스트 두사람이 하는 팟캐스트에서 듣게 된 이야기입니다. 이 두사람이 투자를 하면서 관계에 대한 이야기를 했는데요 두가지 다른 개념의 관계를 얘기하더라고요.

그 중 하나는 우리가 항상 하는 관계이죠. Transactional Relationships 글쎄 이걸 어떻게 번역하면 좋을까요? 그냥 문자적 번역을 하게 되면 “거래관계” 정도가 되겠지만 실제 영어에서 말하는 의미는 좀더 확대된 개념인 것 같습니다.

The transactional relationship definition refers to a business-like approach to a relationship, where each person in that relationship has clear responsibilities and rewards. Those responsibilities will define what each individual is expected to contribute, as well as the rewards each will receive (or expects to receive) as a result of their efforts. (출처:Transactional Relationship | Definition & Characteristics – Study.com)

그러니까 Transactional relationship이란 마치 비즈니스를 하는 것과 같은 관계를 의미하는데 각자가 관계 설정에서 명확한 책임과 보상을 가지는 관계라는 것입니다. 즉, 책임이라고 하면 각 개인이 기여를 해야한다는 점을 서로 기대하고 보상이라는 것은 이러한 노력의 결과로서 무언가를 얻게 될 것이라는 것을 말합니다.

그러니까 사실 우리가 하는 대부분의 관계가 이런 관계죠. 예를 들면 네트워킹을 해야 한다고 말할 때 우리는 그 네트워킹의 결과 상대방이 내게 무언가를 주기를 바랍니다. 예를 들면 새로운 직장의 기회를 얻을 수 있도록 도와준다거나 새로운 사업상 거래를 제공한다든가 하는 것을 말하는 것이겠죠. 이거야 뭐 특별히 다른 점은 없고 사실 이런 관계는 오래 가지 못합니다. 왜냐하면 각자가 원하는 결과를 얻으면 그것으로 그 관계의 결말이 맺어진 것이니까요.

이런 Transactional relationship의 가장 비근한 예가 바로 직장생활이라고 생각합니다. 보다 더 구체적으로 말하면 내가 가진 직장이라는 울타리에서 이루어지는 인간관계들이죠. 좋은 직장에서 높은 직책을 가진 사람은 그렇지 못한 직장에서 그다지 높지 않은 직위를 가진 사람의 상위에 존재하게 되는 다소 상하관계도 은근히 형성되게 되고요 나아가 퇴직을 하거나 은퇴를 하게 되면 이런 관계는 바로 끊어지게 됩니다.

이에 반해 벤처캐피탈리스트들이 말하는 다른 관점이 있는데 Compounding Relationship 인데요 여기서 Compounding이 경제적 관점인 “복리”를 말하니까 직역하면 “복리관계”라고 해야 할까요? 이것에 대해서는 좀더 자세한 이야기가 있습니다. Deepti Pahwa라는 스탠퍼드 대학 LEAD incubator의 창업자분이 쓰신 글인데요 한번 생각해 볼만합니다.

How Atomic Habits Can Transform Professional Networking: The Warren Buffet Way

In a relational context, compounding can be visualized as the deepening and broadening of connections that, over time, increase in value and influence.

인간관계에서 “복리”는 시간이 흐름에 따라 가치와 영향력이 증가하면서 깊어지고 확장되는 관계로 볼 수 있다는 것입니다. Compounding relationship을 만드는 몇가지를 정리해 주고 있는데요

첫째, 양보다 질 (Quality Over Quantity)

Focus on fostering deep connections with a select few rather than accumulating a vast number of superficial contacts. These quality relationships are more likely to provide meaningful support and opportunities.

피상적으로 수많은 사람을 만나기 보다는 선택한 소수의 사람들과 깊은 관계를 이어가도록 노력하라는 것입니다.

둘째, 일관성과 신뢰도 (Consistency and Reliability)

Be a stable and reliable presence. Consistency builds trust, and trust is the foundation of any strong relationship.

안정적이면서 믿을만한 사람이 되라. 일관성은 신뢰를 쌓게 하고 신뢰는 견고한 관계의 기초를 이룬다.

셋째, 시간과 노력을 투자해라 (Invest Time and Effort)

Relationships require effort. Regular check-ins, active listening, and showing genuine interest in others’ success are all crucial.

인간관계를 맺으려면 노력이 필요하다. 규칙적으로 만나고 잘 듣고 서로의 성취를 위해 진정한 관심을 보이는 것이 중요하다.

넷째, 가치를 더하라 (Add Value)

Aim to provide value in every interaction. Whether sharing knowledge, providing support, or connecting people within your network, ensure that your actions contribute positively to the lives of those you connect with.

의미있는 인간관계에 촛점을 맞추라. 지식을 나누거나 상대방을 지원하거나 당신의 아는 사람들을 서로 연결시킬 때 긍정적으로 사람들의 삶에 기여할 수 있는 방향으로 발전하도록 애쓰라.

다섯째, 변화를 수용하고 성장하라 (Embrace Change and Growth)

When you invest in building and sustaining strong relationships, the effects can be far-reaching. Beyond the immediate circle, a robust network can open doors to new opportunities, foster collaborations, and build a support system that can help navigate both personal and professional challenges. The ripple effects of such networks can often be the difference between a stagnant career and a flourishing one.

끈끈한 인간관계를 만들고 유지하면 그 결과는 아주 오래 지속될 수 있다. 친한 사람들을 넘어서 인간관계를 잘 유지하면 새로운 기회를 만들 수 있고 협력을 이루어내며 개인 삶과 일상에서 일어날 수 있는 어려움을 극복할 수 있도록 지지해 주는 관계를 만들어 갈 수 있다. 이러한 인간관계의 파급효과로서 일터에서 정체되지 않고 성취감을 얻을 수 있는 단계로 나아갈 수 있다.

소수의 사람들에게 깊이있게 오랜관계를 유지하고 시간을 투자하고 노력하며 신뢰관계를 형성하는데 힘쓰라는 말씀이 마음에 와닿습니다.

제가 커리어 코칭을 통해서 그리고 저도 코칭을 받으면서 오랜 기간 서로를 지지하고 격려할 수 있는 건설적인 관계를 맺고자 하는데 여기에서 말하는 The Power of Compounding Relationships 라는 개념처럼 점차 더 깊어지고 성장할 수 있는 그러한 관계가 되도록 하고 싶은 것이 저의 목표이기도 합니다.

The Power of Compounding Relationships에 대해 얘기하는 필 대니얼이라는 투자은행가의 이야기도 있습니다. 인디애나의 크리스찬 가정에서 자란 필 대니얼은 자신의 부모님으로 받은 가르침을 나누면서 인간관계를 어떻게 가져갈 것인지에 대해 배웠다고 말씀하고 있습니다.

Prepare early and ahead of time to prepare your legacy and identity ahead of a sale, exit, or merger.

Not all ideas and businesses are going to generate high profits, but they can still have a high impact.

You will receive a lot of “no” answers.

They teach discipline, accountability, persistence, and trust in the Lord.

Be willing to be mentored, and be a mentor.

필 대니얼은 크리스찬으로서의 가치를 함께 얘기하고 있는데요 여기에서 이야기하는 몇가지 요점은 이렇습니다.

일찍 준비하고 미리부터 어떤 레거시를 남길 것인지, 자신만의 아이덴티티를 준비하라.

모든 아이디어와 사업이 높은 수익을 보장하지는 않지만 여전히 큰 임팩트를 만들 수 있다.

살면서 부정적인 답변을 많이 듣게 될 것이라는 점을 알아라.

부모님으로 부터 훈육, 책임감, 끈기를 배웠고 주님을 믿었다.

배우려고 애쓰고 누군가의 멘토가 되라.

“Prepare your legacy“라는 말도 사실 번역이 좀 어렵네요. 거래하듯이 인간관계를 하려고 하지 말고 무언가를 남기는 인간관계가 되도록 하려면 어떻게 해야 할지 잘 준비하고 그대로 실행하라는 그런 의미라고 생각합니다. 그리고 누군가로 부터 배우고자 애쓰고 자신도 누군가의 멘토가 되라는 말씀도 마음에 와닿습니다.

커리어 코칭에 대해 요즈음 많이 읽고 생각하며 지냅니다. “Prepare your legacy and identity“라는 말씀을 잘 새기고 잘 준비해서 선한 영향력을 끼칠 수 있는 사람이 될 수 있도록 해야 할 것으로 다짐을 하게 됩니다.

Adimab은 항체개발의 One-stop shop으로 임상시험 없이 오로지 연구와 파트너쉽을 통해서 성장한 모델이었는데요 이 회사에 대해 글을 쓰던 중 잠깐 언급했던 인물이 한명 있는데요. 그 이름은 Errik Anderson입니다.

“여기에서 두분의 교수 – Tillman Gerngross 교수와 Dane Wittrup 교수 – 가 가진 입증된 연구성과를 바탕으로 계약 주체들과의 신뢰를 형성한 것이 중요했고 또 하나 Errik Anderson이라는 분의 치밀한 특허분석과 전략 수립 그리고 사업계발 전략이 큰 공을 차지한 것으로 보입니다. 나중에 Errik Anderson의 다른 벤처에 대해 얘기할 기회가 있으리라 생각합니다.”

Errik Anderson이 Adimab에 참여할 당시는 Tillman Gerngross 교수의 학생이었는데 그는 빅파마, 바이오텍이 항체개발을 외주를 주려면 어떤 특허적인 문제들을 넘어야 할지를 면밀히 분석하고 이렇게 분석한 Patent map에 근거해서 전략을 수립해서 필요한 특허들을 매입하고 그 이후에 사업개발을 통해서 회사를 성장시키는데 큰 역할을 한 주역으로 함께 성장을 했습니다. 이렇게 10여년간 경험을 쌓은 Errik Anderson은 자산을 많이 축적하게 되었고 이렇게 축적한 자산을 바탕으로 Ulysses Diversified Holdings 라는 Single-family office를 2013년에 창업해서 자신의 자산을 바탕으로 한 VC를 시작했습니다. 이 회사가 Private company이고 특별한 정보를 제공하지 않기 때문에 자세히 알 수는 없지만 7년 전에 VC analyst를 모집하는 공고가 있는데 이 공고에 보면 어떤 일을 하는 회사인지 살짝 들여다 볼 수 있습니다.

이 잡공고가 너무 재미있고 까탈스러워서 이 곳에 그대로 올립니다. 그리고 공고문 중간중간에 제 생각을 좀 남깁니다.

Ulysses Diversified Holdings is looking for Analysts to help us change the world.

This is likely going to be the hardest job you’ve ever had in your life. We’ll ask you to take responsibility for yourself, our companies and the impact we all have in the world. This is an apprenticeship model, where you’re expected to be independent and do the work alongside our team and our companies.

여기에서 말하는 Apprenticeship model이라는 것은 소위 견습생이라는 개념입니다. 즉, 가르쳐서 키우겠다는 의미를 담고 있죠. 그러니까 현재를 보지 말고 미래를 보고 합류하라는 행간의 의미를 담고 있습니다. 이미 여기서부터 심상치 않습니다.

The hours are as long as necessary to change the world – you do the math. Please recognize that our Analyst position is coming in at the ground level and we try very hard to stay lean and close to the action. We don’t have assistants. We don’t have “people” who do things. We do things. All of us here at Ulysses. That’s life. Doing the small things is what connects us to the reality of startup life.

Everyone takes a pay cut to come to Ulysses. This world needs missionaries, not mercenaries. When we create value, we share that value, pure and simple.

자, 여기에 그 의미를 담았죠? Finance, accounting 학부를 나오고 1-2년간 VC, PE, consulting 업계에서 일을 한 사람이어야 자격조건에 들어갑니다. 이런 사람은 이미 고액연봉자일 가능성이 크죠. 그러니까 연봉은 줄어든다는 것입니다. (pay cut) 그런데 선교사 (missionaries)래요. 선교사가 누구입니까? 현재 아무것도 없는 곳에 들어가서 복음의 씨앗을 뿌리지만 그 열매가 언제 거두어질지 알 수 없는 일을 하는 사람입니다. 투자 선교사라…가치를 창출하고 그 창출된 가치를 공유하겠다고 합니다. (create value…share that value)

You will learn the ins and outs of new company creation, venture capital and private equity while starting up and scaling our own companies and analyzing other investment opportunities. In 3 years, we expect all our Analysts to be working actively inside a company in a leadership position, starting their own company or continuing to grow their career in venture capital or private equity. As long as you continue to support and project our values in the world, you’ll always be a member of the Ulysses team, even after you move on to another company or start your own company.

뽑으려는 견습공에게 3년 후를 설명합니다. 이 투자심사역은 3년 후에 어떤 회사의 중역으로 혹은 자기 회사를 설립해서 혹은 VC나 PE로 성장하게 될 것이라고 말이죠. 그러니까 이 포지션은 결국 VC인데 PE 즉 M&A를 포괄하는 업무를 하게 된다는 것이고 3년후에 회사를 경영하든지 투자자로 나아가든지 당신 스스로 결정할 수 있다. 뭐 이런 느낌을 줍니다.

Ulysses Diversified Holdings is a private, diversified holding company founding, incubating, growing and funding cutting-edge biotech, high-tech and consumer-focused companies. Ulysses supports entrepreneurially-minded individuals, their companies and other startups with the world’s best executive talent and resources in finance, legal, strategy, leadership development, recruiting, HR, and business development.

While we have access to hundreds of millions of dollars in permanent, evergreen capital, we are not a typical venture capital shop. We evaluate our projects using three simple criteria: 1) it must be a problem worth solving, 2) we must be working with good people, and 3) we must be able to add value beyond the check we write. Problem worth solving, people worth helping and time worth spending. Simple. We choose our projects for maximum impact in the world and our communities. We do the work. Right alongside entrepreneurs and their families.

이제 회사를 소개합니다. Ulysses Diversified Holdings는 첨단 바이오텍 (cutting-edge biotech), 첨단기술/소비자 중심 회사 (high-tech and consumer-focused co)를 설립, 인큐베이팅, 성장하고 투자하는 회사입니다. 일반적인 family office가 아니죠. 결국 VC firm의 성격이 아주 강한 회사인데 소비자 중심회사 이것 때문에 PE가 결부되는 것입니다. 창업자 마인드를 가진 개인 (entrepreneurially-minded)과 그들의 회사들 혹은 스타트업을 돕는데 여기에 재무, 법률, 전략, 리더쉽 개발, 채용, 인사, 사업개발 분야의 세계 최고 경영진 풀을 제공하겠다는 것입니다. 수억불의 펀드가 있지만 전형적인 VC는 아니고 (1) 해결할만한 가치 있는 문제에 대하여 (2) 좋은 사람들과 일해야 하고 (3) 투자금을 훨씬 상회하는 가치를 창출할 수 있어야 한다. 는 것입니다. 굉장하죠?

Ulysses’ mission to “Make People Better at Making the World a Better Place” is a recognition that the greatest impact on the world will be made with and through people who share its core values, work ethic and commitment to excellence.

While we are a biotech and healthcare heavy shop, we have a strategy to reach millions of people through our more consumer-focused efforts. As an example, Ulysses is the owner and manager of New England Rugby Club (aka the Free Jacks), which is a part of Major League Rugby. Ulysses is intimately involved in every aspect of day-to-day operations of the professional rugby team and the league. As a member of the Ulysses team, be prepared to love rugby.

There is no “typical” day at Ulysses, nor is there a “typical” person. We need insanely hard-working, motivated leaders who understand that no job is too small in a startup while no ambition is too large over the long run.

투자부문은 바이오텍, 의료 분야인데 소비자-중심 전략으로 수백만의 사람들에게 다가가고자 한다고 해요. 이미 New England Rugby Club을 소유, 경영하고 있고요. 럭비를 좋아해야 한다는군요. 미식축구말고 럭비요. 미국에서 누가 럭비를 하나요? 축구도 그리 많이 안 좋아하는데…여하튼 마지막으로 촌철살인을 날립니다.

우리는 일에 미쳐서 스스로 일하는 그런 사람을 찾는다. 이 사람은 어떠한 스타트업도 작다고 여기지 않고 어떤 야망도 결국 그다지 크지 않을 수 있다고 믿는 사람이다. 라고요. 스타트업을 오랜 기간 해 온 경험과 에릭 앤더슨의 철학이 들어가 있습니다. 스타트업을 시작할 때 생각했던 것과 달리 실제로 경영을 하다보면 전혀 다른 방향으로 크게 성장하는 경우를 너무 많이 봤다는 것이죠. 에릭 앤드슨이 대학 졸업 후 Adimab과 그에서 파생된 스타트업을 경영하면서요.

Principal Responsibilities

Make People Better at Making the World a Better Place.

Act with integrity.

Be present, do the work.

Required Qualifications

Be an entrepreneurially-minded, self-starter constantly looking for ways to add value without being told what to do every minute of the day

A strong technical or financial background and general curiosity about the way the world works

Superior written and verbal communication skills. The ability to articulate thoughts in a clear and concise manner through written correspondence, presentations and in meetings

Strong skills in at least a few of: PowerPoint, Excel, Benchling, antibody engineering, functional genomics, Quickbooks, Filemaker Pro, Adobe Create Suite, CRM platforms, Matlab, R, Python, Java, SQL, Scratch

Bachelor’s Degree or equivalent Thiel Fellowship

Helpful Qualifications

Minimum 1 – 2 years of work experience in private equity, investment banking, or management consulting as an Analyst or 3-4 years of work experience in another field.

Bachelor’s Degree with a concentration in Finance, Economics, Accounting or a related field

이 공고에 보면 연구자료를 보관하는 benchiling과 항체공학 그리고 Functional genomics에 대한 기술적 재능이 있어야 한다고 합니다. 즉, 에릭 앤더슨이 항체와 유전자 분야에 진출하고자 한다는 의미가 되겠죠. 그리고 AI/ML도 이미 생각을 하고 있습니다. 이 공고가 7년전 그러니까 2017-2018년 즈음이 됩니다.

이 공고가 날 즈음 에릭 앤더슨은 새로운 바이오텍을 설립합니다. 그 바이오텍이 오늘 얘기할 Alloy Therapeutics입니다. Alloy Therapeutics는 2017년에 설립되고 시리즈 A, B를 지나서 2021년에 시리즈 C를 했습니다. 이 당시 3가지 비즈니스 모델로 펀딩을 했는데요 (1) Humanized mouse platform licensing revenue (2) CRO revenue (3) 스타트업 지분을 통한 미래수익을 제공한다는 것이었습니다. 그리고 에릭 앤더슨은 3세대 바이오 벤처캐피탈 모델이라고 Alloy Therapeutics의 사업모델을 설명했습니다.

The Series C round valued Alloy at $563 million…Anderson’s pitch was focused on the startup’s humanized mouse platform...Around 70 organizations have licensed Alloy’s mouse technology.

Another branch of the business conducts contract research work and tech support for drug companies and academic laboratories.

It’s the third arm of the business that offers the most upside for investors: Alloy’s in-house company creation studio dubbed 82VS.

Alloy and its entrepreneurs-in-residence will create new startups by working with other drug companies, or funnel some ideas into Alloy’s own wholly owned subsidiary, New Frontier Bio.

It’s already started doing this, launching eye-disorder drugmaker Broadwing Bio in December with Maze Therapeutics, a San Francisco-based biotech developing treatments for genetically driven diseases.

Alloy’s investors will automatically get a stake in those ventures and could make money if they’re acquired or go public.

Alloy is part of what he calls the third generation of biotech venture capital. Investors have moved from simply handing over a check, to creating biotechs themselves, to now developing companies with the infrastructure to support multiple ventures.

그리고 1년반 후 시리즈 D를 추가로 했습니다. 1년반동안 Keyway TCR Discovery라는 TCR 개발서비스를 신설했고 gapmer를 발명한 Sudhir Agrawal 박사와 Genetic medicine 서비스를 만들었으며 스위스 바젤, 미국 조지아와 샌프란시스코에 연구소를 개소했습니다. 그리고 공동연구에 필요한 CRO, CDMO 및 특성적 기술기반 서비스 회사와 연계한 서비스를 제공하게 했습니다.

Alloy has expanded from its foundational antibody discovery technologies and discovery services into T-cell receptors (TCRs), with the launch of its Keyway TCR Discovery division, and genetic medicines through its collaboration with Dr. Sudhir Agrawal, the inventor of gapmer technology. Alloy has further expanded with three new research sites, in Basel, CH; Athens, GA; and San Francisco, CA.

Alloy also supports complementary CROs, CDMOs and other discovery and development service providers as a critical part of the collaborative ecosystem to empower pharma in its mission to cure disease.

Alloy Therapeutics에 대한 기사가 GEN Edge에서 3년전에 나온 적이 있습니다.

What would it look like to build a company that you scale this up in a different way?…Alloy Therapeutics. Anderson wanted to help the scientist-entrepreneur who has a great idea about how to make a drug but then is faced with the problem of how to get access to the tools, technologies, protocols, scientific team, and capital—all the things that have to come together to build a biotech company.

Errik Anderson은 Alloy Therapeutics의 철학에 대해서 말하고 있습니다. “과학자 창업자를 도와줄 도구, 기술, 프로토콜, 과학자 팀과 자본을 제공하는 회사를 만들고 싶었다”

Founded in 2017 in Boston and privately funded by visionary investors, Alloy also has labs in Athens, GA, San Francisco, and European labs in Cambridge, U.K., and Basel, Switzerland...Five-and-a-half years ago, Alloy started with antibodies and eventually moved into adjacent fields. Alloy’s second and third modalities are T-cell receptors (TCRs) and genetic medicines. In 2022, it launched Keyway TCR Discovery as a fully integrated TCR-mimic and engineered TCR discovery platform and service offering. Now, it’s developing new novel formats in antisense oligonucleotides as pre-competitive technology that it will share with interested groups through its Genetic Medicines group. Alloy Therapeutics also works in peptides, cell therapy, and drug delivery. More than 130 companies are already working with one or more of Alloy’s platform technologies.

Anderson doesn’t shy away from the word service provider or CRO. “In science, everything we do is providing services,” he said. “We embrace a bit of that service mentality that is trying to collect cash, while using that capacity to also do something more strategic by improving our technologies.

Alloy’s venture studio 82VS…provides venture partners and entrepreneurs access to all platforms and services at a low cost to enable quick initial experimentation, paired with company creation expertise to empower newer entrepreneurs.

“We’re trying to cut out those first 1.5–2 years and be able to run those initial experiments,” said Anderson. “Maybe it’s a few hundred thousand dollars in experiments.– in cases where the partner is a venture partner or an executive in residence (EIR) in the venture studio, the common stock is split between Alloy and the founding team.

“Our typical model is we open a multimillion-dollar master services agreement (MSA) that allows that company to access our services, and so they don’t pay any cash,” said Anderson. “It’s like a loan to the company. It’s also non-dilutive. The idea is how quickly can we start designing experiments and doing drug discovery.”

If that works out and an 82VS company can make it to seed financing, Alloy Therapeutics writes the first million-dollar check to get some cash into the company. “When you have a lead or maybe two drugs in hand and some enabling data, and now you’re out doing your Series A or seed financing with new external venture capitalists with a lot of data in hand, it shifts the power dynamic a bit in this field where you can go to an investor with data in hand and maybe a drug lead,” said Anderson. “This is why we talk about innovation and access to innovation. When we think about 82VS with a venture studio, it’s not just access to innovation but also capital and expertise.”

We get excited about bringing access to technology, capital, and expertise and allowing people to start up these companies and then leave the venture studio. At that point, it’s external financing. We support them along the way and want to be really good permanent friends. We’ll always be there.

“The deals Flagship, Atlas, and Third Rock Ventures will do just don’t fit our model,” said Anderson. “Ours is pretty lean. It’s a different sort of project that we’re doing. Once we step in and do that seed or Series A financing with an external party, that’s exactly the folks that we want investing in our companies. Maybe we’re taking away the company creation pieces for a year or two and bringing them a fully formed idea with our scientist-entrepreneurs we’re working with. We see this as doing a slightly different part of the value chain of how you do venture creation behind drug assets.”

For now, not a single company that has licensed Alloy’s technology has gone out of business, according to Anderson.

The controlling class of stock is held in an entity that cannot be sold. “Alloy cannot be sold,” said Anderson. “Theoretically, Alloy could go public, but it will continue to exist so long as we don’t run out of money. It’ll just continue to be around in 100 years, innovating and sharing that innovation with others.”

Alloy reinvests 100% of revenue into innovation and access to innovation. “When we’re collaborating with big pharma and emerging biotech companies, we’re making this promise and commitment that if you give us $5 million to do something, we will use that to develop new technology and share it with the world,” said Anderson. “We are going to reinvest all of this.”

Those two aspects of Alloy’s business model allow the ecosystem to build technologies and companies across slightly longer time horizons than a traditional venture model. “When you can start playing with time as one of your variables, like great technology and great people, you can do things that look extraordinarily different,” said Anderson. “Most of the ideas we have had are those others have had. We’ve just executed this with a slightly different business model and different constraints.”

In October 2022, Alloy closed $42 million in Series D financing led by its existing investors 8VC and Mubadala Capital and joined by return investors Thiel Capital, Presight Capital, Founders Fund, and other unnamed family offices and sovereign wealth funds. Alloy will use proceeds from the Series D financing to further support the drug discovery community with new pre-competitive drug discovery technologies in biologic modalities and new partnership models designed to further fuel innovation.

We believe the best scientific insights should dictate which drugs advance to the clinic, rather than whether someone can afford access to the right enabling technologies. Since Alloy’s founding in 2017, we have been a company focused on democratizing access to tools, technologies, services, and company creation capabilities for the global scientific community. Having launched our first commercial platform in 2019, we’ve grown our ecosystem to 130+ partners across academia, biotech, and pharma, and have achieved our first IND filing from a licensee of our first platform, the ATX-Gx for human antibody discovery, and continue to see more partners advancing to the clinic. We have rapidly expanded ATX-Gx with new strains designed to solve different problems in antibody discovery, all of which are accessible to our partners under their original license. We have expanded this model of democratizing access from antibodies into five adjacent biologic modalities: TCRs, genetic medicines, cell therapies, peptides, and drug delivery technology.

With the help of our venture studios, 82VS, we’re also able to continuously support the launch of new asset-focused startups that in turn leverage our platforms and services. These new startups also serve as early adopters of our innovations and help expand our technology and service offering for our entire ecosystem.

Alloy’s novel business model has been embraced by 16 established pharmaceutical companies, all of whom understand and share our commitment to developing and supporting long-sustaining research and development.

This allows our team to become experts in using our proprietary in vivo, in vitro, and in silico technology, as well as incorporate other top industry standard protocols to discover the best therapeutic drug candidates for our partners. To further support the industry as an innovation partner, earlier this year we launched an Innovation Subscription program, which offers access to all current and future Alloy discovery technologies at one fixed annual fee. This offering has a multiplier effect given our commitment to reinvesting 100% of our revenues into innovation: each Innovation Subscription fee is invested into acquiring and inventing new technology that can benefit the entire consortium.

3년전에 Errik Anderson이 인터뷰한 1시간 30분 짜리 동영상이 있습니다. 신약개발은 100년 이상 사람들이 사용하게 되는 의미있는 일이라는 에릭 앤더슨의 말씀이 인상적입니다.

그리고 1년전에 PE Firm인 10X Capital과 인터뷰한 최근 동영상도 있습니다. 제목이 재미있습니다. 20개 이상의 스타트업을 창업해서 $10 Billion 이상의 가치를 만들어 내겠다는 야심이 대단합니다.

요즈음은 출근해서 돌아오는 길은 이상하리만치 에너지가 떨어집니다. 차에서 조금씩 조는 저 자신을 발견하는데요 다행히 차가 자율주행을 하는 Tesla라서 그래도 문제없이 집까지 오는 것 같습니다. 오늘 이렇게 피곤한 상태에서 그래도 좋은 공연을 관람해서 그 얘기를 좀 나누고자 합니다.

미국의 아카펠라 그룹인데요 “Voctave“라는 그룹입니다. 11명의 혼성으로 구성된 아카펠라 그룹인데 2015년에 시작해서 올해로 10주년이 되었다고 합니다.

2015년에 Jamey Ray가 유튜브에 올린 영상이 대박이 나면서 지금까지 오게 되었다고 해요.

Jamey Ray의 개인적인 성장기와 Voctave의 성장사는 이 기사에 잘 나와 있습니다.

공연은 참 대단했습니다. 앵콜곡으로 사운드 오브 뮤직의 Climb the mountain을 불렀는데 왠지 울컥 하더군요. 아내도 그랬다고 하더군요. 우리가 좀 힘들게 살아 왔나봐요. 오늘은 큰딸 내외와 함께 관람해서 너무 좋았습니다. 아카펠라 그룹을 했던 막내도 함께 봤으면 좋았겠다 싶었어요.

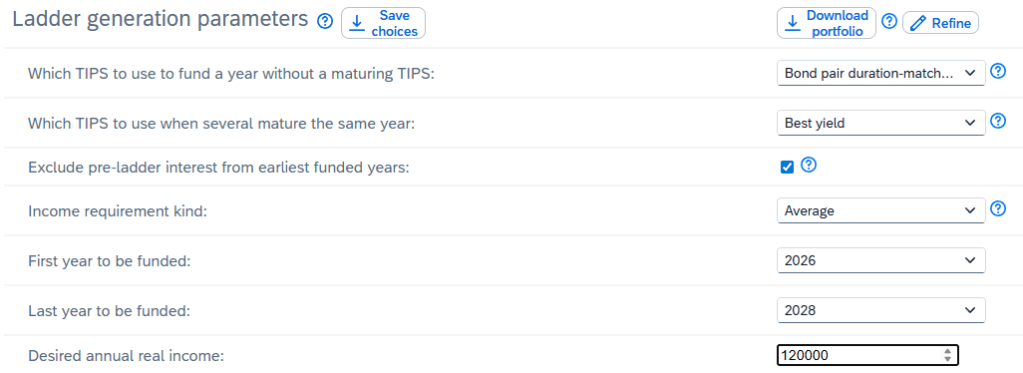

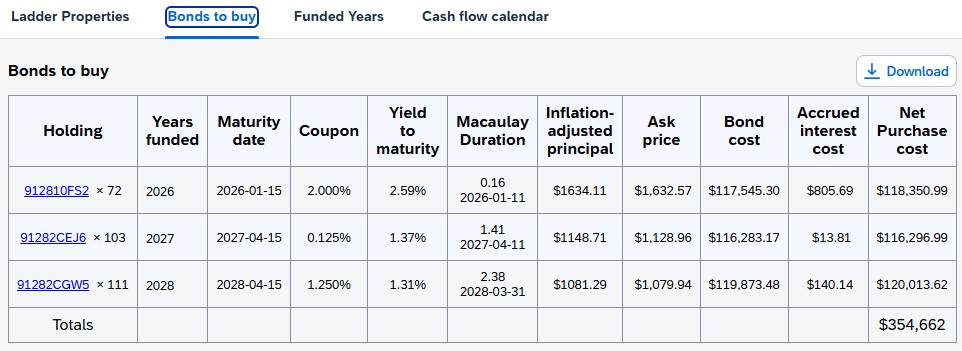

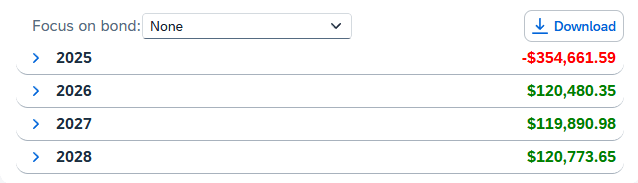

노잼투자에 대해 글을 쓴 지 꽤 오래 지난 것 같습니다. 아마 그만큼 제가 투자에 대해 많이 생각하지 않고 살고 있다는 방증이 되겠지요. 몇주전에 찾은 좋은 사이트가 하나 있어서 여기에 그 이야기를 좀 남기려고 합니다. 이러면서 저도 공부를 좀 할 수 있을 것 같습니다.

친구들이 가끔 채권투자는 하느냐고 물어보는 경우가 있습니다. 그에 대한 저의 답은 “안한다”입니다. 그러면서 덧붙이는 것이 저자신이 채권처럼 돈을 벌고 있는 동안에는 채권투자는 따로 하지 않아도 된다고 생각한다고요.

그렇지만 만약 일을 하지 않을 때를 대비해서 일부의 채권투자는 필요해 보입니다. 특히 3년 정도의 생활비에 해당하는 부분은 채권투자를 하면 좋겠다고 생각을 하는데요. 문제는 어떤 채권을 투자하느냐 하는 것입니다. 요즘 채권이 좋지가 않지요. 저도 401(k) 투자하면서 채권 ETF를 투자해 본 적이 있는데 제 성향과 전혀 맞지 않더라고요. 그래서 전부 빼서 거의 100% 주식에 투자하고 있습니다. 주로 S&P500 Index Fund에 투자하고 있어요.

채권 중에서 제가 관심을 가지는 것은 TIPS (Treasury Inflation-Protected Securities)라는 인플레이션 헤징 미국채에 관심을 가지고 있습니다. TIPS는 다른 채권과 같이 원금+이자를 지불하는데요 일반 채권과 다른 점은 원금이 인플레이션만큼 매년 올라간다는 점입니다. 그러니까 인플레이션만큼은 항상 올라가거나 내려간다는 장점이 있는 것이지요. TIPS도 아주 많은 종류가 있는데요 그 많은 TIPS 중 어떤 것에 투자해야 할지 알 수 없는 경우가 많아서 곤란을 겪게 됩니다. 이에 대해 좋은 가이드가 있습니다.

Dartmouth College의 Bioengineering의 Tillman Gerngross 교수는 2000년 GlycoFi라는 항체회사를 창업했습니다. GlycoFi는 효모 (Yeast)에서 단백질을 생산하는 기술을 기반으로 한 회사로서 $20 Million VC funding을 포함해서 총 $32 Million을 투자해서 6년 후인 2006년도 Merck에 $400 Million에 매각되었습니다. 이 회사에 투자했던 회사는 Polaris Partners였습니다.

GlycoFi 가 매각되고 나자 Gerngross 교수는 다시 Adimab LLC를 창업했는데 이 회사는 매각을 하지 않으려는 목적으로 설립을 했다고 전해집니다. 수년이 지나 Merck는 GlycoFi의 직원 중 일부는 해고하고 일부는 보스턴으로 이전시켰는데 Adimab은 GlycoFi에서 해고된 직원을 고용하고 GlycoFi를 다시 사고자 했습니다. 그에 대한 기사는 아래에 있습니다.

Adimab’s funded discovery partners include top pharmaceutical companies, such as Merck, Roche, Novartis, Eli Lilly, Genentech, Biogen Idec, Novo Nordisk, Gilead, Kyowa Hakko Kirin, Pfizer, Celgene and innovative biotechnology companies, such as Arsanis, Jounce, Five Prime Therapeutics, Alector, Mersana and others. Adimab typically receives various upfront payments, commercial license fees, development milestones and downstream milestones and royalties on product sales.

그리고 2020년부터는 Adagio Therapeutics를 필두로 스타트업을 분사하기 시작합니다. Adagio Therapeutics는 Invivyd로 사명을 변경하였습니다.

The major problem Adimab solved was legal not technical — it created a platform that served as a one-stop shop for antibodies in an environment where larger companies had difficulty building out their own processes due to the potential of infringement.

Adimab’s model was not an overnight success — the amount of technical and business development work and patience over the last…

In order to create a one-stop shop for antibodies, Adimab did a tremendous amount of work to analyze the hundreds of different patents in the field and design a platform that wouldn’t infringe on most of them. Consequently, their first business deal was the purchase of a patent portfolio. By deliberately creating a platform that minimized royalties to other companies, Adimab was in the position to scale up quickly and solve the legal problems large biopharma companies were facing.

An important feature of Adimab’s deals have been non-exclusivity for targets allowing the company to work with multiple companies that are experts in their targets and indications. By focusing solely on discovery and scaling up partnerships, Adimab ended up very capital efficient with enough cash-flow to be returned to shareholders and reinvested into the company.

Adimab의 성공요인으로는

첫째, 항체 특허 분석을 통해 One-stop shop을 만들 수 있는 특허 포트폴리오 구입을 한 것

둘째, Non-exclusivity 계약으로 최대한 많은 기업과 계약을 체결할 수 있도록 한 것

셋째, 오직 연구와 파트너쉽에만 집중함으로써 충분히 자본을 축적하고 투자자들에게 충분한 현금흐름을 제공하고도 넉넉한 자금을 회사에 재투자한 것입니다.

여기에서 두분의 교수 – Tillman Gerngross 교수와 Dane Wittrup 교수 – 가 가진 입증된 연구성과를 바탕으로 계약 주체들과의 신뢰를 형성한 것이 중요했고

또 하나 Errik Anderson이라는 분의 치밀한 특허분석과 전략 수립 그리고 사업계발 전략이 큰 공을 차지한 것으로 보입니다.

지난 몇주간 Pfizer와 Novo Nordisk 사이에서 M&A 전쟁이 있었던 Metsera가 결국 Pfizer가 종전 가격보다 높은 가격으로 Bidding함에 따라 Pfizer가 최종 승자가 되었습니다. 이번 M&A는 처음에 Pfizer가 쉽게 인수하는가 했는데 갑자기 Novo Nordisk가 경쟁에 참여하면서 몇주간 아주 큰 뉴스가 되었습니다. 오늘은 이 인수전에 대한 이야기를 좀 해 보려고 합니다.

Clive Meanwell, MD는 The Medicines Company를 1996년에 창업해서 2019년에 Novartis에 Inclisiran 등의 파이프라인을 가지고 $9.7 Billion에 매각하고 계약을 2020년 1월에 마무리 지었습니다. 그리고 나서 Private Equity Firm인 Population Health Partners를 설립하고 ARCH Ventures와 함께 Obesity, Diabetes 신약개발 회사로서 Metsera를 설립하기로 했습니다. 2020년에 Big Pharma에 투자 의향을 물어 봤지만 당시 뜨뜻미적지근해서 결국 2022년에 설립하게 되었다고 합니다.

The $290 million financing was led by founder Arch and is a series A round that includes a “little seed” money, according to Meanwell. “There was emerging evidence that diabetes and weight loss was going to become a big category,” he said, explaining how Metsera came to be. “Initially, we had discussions with Big Pharma about their appetite for investing—I’d say in 2020, it was sort of lukewarm,” Meanwell said. “Nobody had quite seen the juggernaut that was coming.”

Meanwell also helped form and is a partner of private equity firm Population Health Partners. The firm, alongside Arch Venture Partners, launched Metsera during biotech’s “nuclear winter” in early 2022, the CEO explained. However, the company was able to stay warm in stealth with the help of several other investors such as F-Prime Capital, GV, Mubadala Capital, Newpath Partners and SoftBank Vision Fund 2, alongside other undisclosed investors.

200개 이상의 회사들을 쇼핑하기 시작했고 그 중 가장 좋은 회사로서 영국의 Zihipp을 인수하게 되었습니다.

After Eli Lilly and Novo Nordisk started publishing “great data” for the diabetes and obesity franchises-in-a-drug semaglutide and tirzepatide, respectively, Meanwell and the Arch crew decided to abandon the Big Pharma aspirations and start something of their own. “We went out and said, let’s go shopping among the 200-plus companies that are already working in this space, and let’s see if we can pick up some great technology and create a new company that could develop these technologies for commercial use,’” he explained.

Zihipp은 2012년에 런던에서 설립된 바이오텍으로서 2022년에 Metsera에 인수된 것입니다. Zihipp은 Imperial College Institute의 Steve Bloom 교수가 개발한 물질에 기반하여 창업한 회사였는데 당시 호르몬을 모방하는 2만개의 Peptide library를 가지고 있었습니다. 그 중 GLP-1 표적인 MET-097i와 Amylin 표적인 MET-233i를 Metsera에서 인수했습니다.

The Zihipp drug candidate that became MET-097i was invented by Professor Steve Bloom, a globally renowned researcher from Imperial’s Department of Metabolism, Digestion & Reproduction, whose 1996 discovery that GLP-1 affects appetite sparked the revolution in obesity treatment using GLP-1 drugs. At Imperial, Professor Bloom and his team built up a library of 20,000 peptides that mimic hormones. The group carried out initial studies to build the library of peptides at the Imperial Biomedical Research Centre and the Imperial NIHR Clinical Research Facility. With support from Imperial Enterprise, they went on to commercialise their discoveries through the Imperial spinout Zihipp…Metsera also obtained an Imperial drug candidate later called MET-233i from Zihipp, which mimics another appetite-regulating hormone, amylin. MET-233i is being investigated for its potential to be combined with MET-097i.

그리고 Steve Bloom 교수님의 연구에 대해서 상세한 이야기가 Imperial에서 기사화된 것이 있습니다.

A first spinout company, Thiakis, was set up in 2005 to develop the hormone oxyntomodulin as a potential treatment for obesity. A second spinout, Zihipp, followed in 2019, this time developing a broad range of diabetes and obesity therapies…Thiakis was sold to Wyeth in 2008, and Zihipp was sold to Metsera Therapeutics in 2023.

그리고 Metsera는 D&D Pharmatech로 부터 Long acting oral peptide technology를 얻었습니다. 이 기술과 D&D Pharmatech의 역사에 대해서는 전에 블로그를 쓴 적이 있습니다. 이강춘 석좌교수님의 아드님이신 이슬기 대표이사의 이야기가 참 흥미롭고 부럽죠.

그리고 올해에 Pfizer가 M&A를 발표했죠. 처음에 Pfizer가 $7.3 Billion으로 Metsera를 M&A 한다고 발표를 했는데요 곧이어 Novo Nordisk가 $9 Billion으로 새로운 오퍼를 했고 결국 Pfizer가 $10 Billion으로 오퍼를 올려서 M&A를 성사시킨 것입니다.

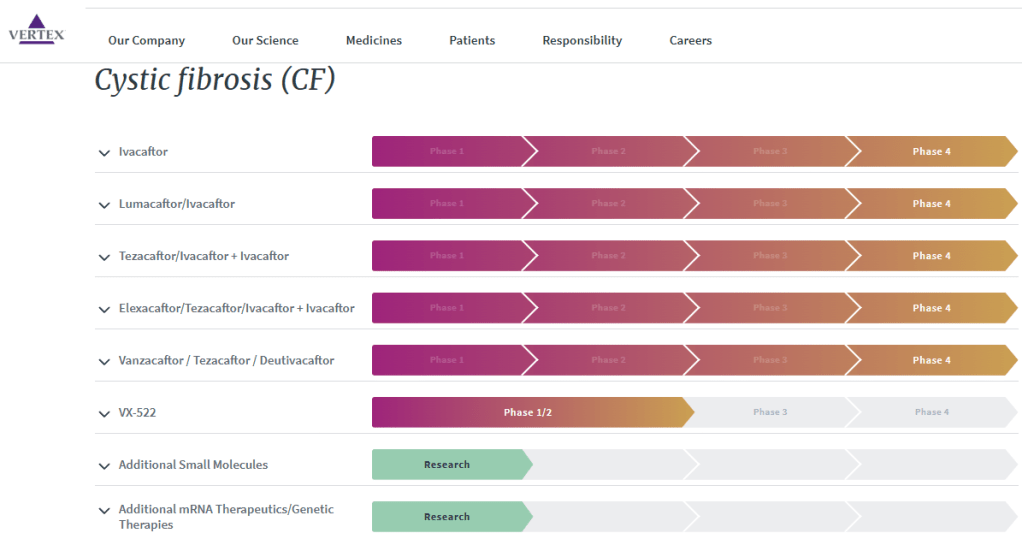

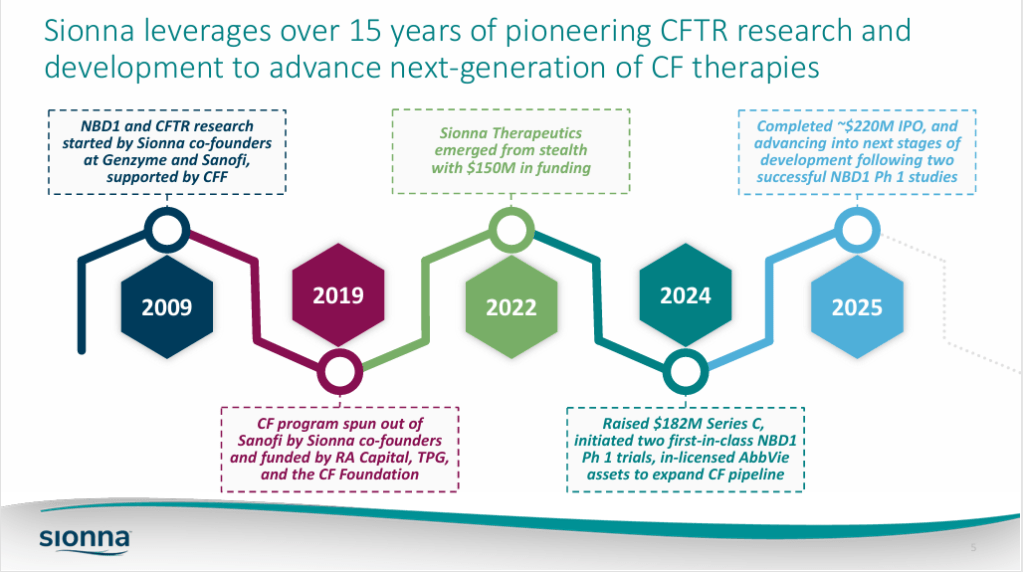

Cystic Fibrosis (낭포성 섬유증) 은 F508del이라는 이상 염색체에 기인한 유전성 폐질환인데요 보스턴의 Vertex Pharmaceuticals가 이 부문의 약품을 판매하는 세계적인 바이오텍 기업인데요 CFTR drug으로만 2024년에 $11 Billion의 매출을 올렸습니다.

CFTR drug discovery는 지금도 많은 기업들에서 하고 있는데요 그 중의 하나가 Sanofi/Genzyme 입니다. Sanofi/Genzyme은 2009년부터 연구를 시작해서 2011년에 Cystic Fibrosis Foundation과 공동연구를 하며 이 분야에 대한 연구를 진행했습니다.

이렇게 10여년간 연구를 거듭한 결과로 나온 약물들을 개발해 온 Greg Hurlbut 박사와 Mark Munsun 박사는 2019년에 Sionna Therapeutics를 Co-founding하게 되었고 Sanofi로 부터 약물들을 $1.5 Million Upfront payment 로 사오게 됩니다.

Sionna is building on the efforts of Sanofi and AbbVie in cystic fibrosis. Greg Hurlbut, Ph.D., and Mark Munson, Ph.D., set up the biotech after working together at Sanofi, and it wasn’t long before Sionna had licensed compounds designed to stabilize NBD1 from the French pharma for $1.5 million upfront.

Multiple companies have studied NBD1, reflecting its key role in CFTR function, but are yet to develop a drug against the target. Pfizer called its results “discouraging,” adding that the binding domain “may not contain the features needed to build high‐affinity interactions.” However, Sionna believes it can hit the target, positioning it to advance treatments for the 90% of cystic fibrosis patients with F508del mutations.

Sionna has raised approximately $150 million to date.

Sionna is advancing a pipeline of first-in-class small molecules designed to fully restore the function of the cystic fibrosis transmembrane conductance regulator (CFTR) protein that is defective in CF, by stabilizing CFTR’s first nucleotide-binding domain (NBD1). The leading cause of CF is the genetic mutation ΔF508 that affects NBD1 stability and CFTR function.

2009년-2019년까지의 Sanofi/Genzyme 연구 결실을 바탕으로 2019년에 설립된 Sionna Therapeutics는 2022년 Series B와 2024년 Series C를 한 이래 2025년에 나스닥에 상장되었습니다.

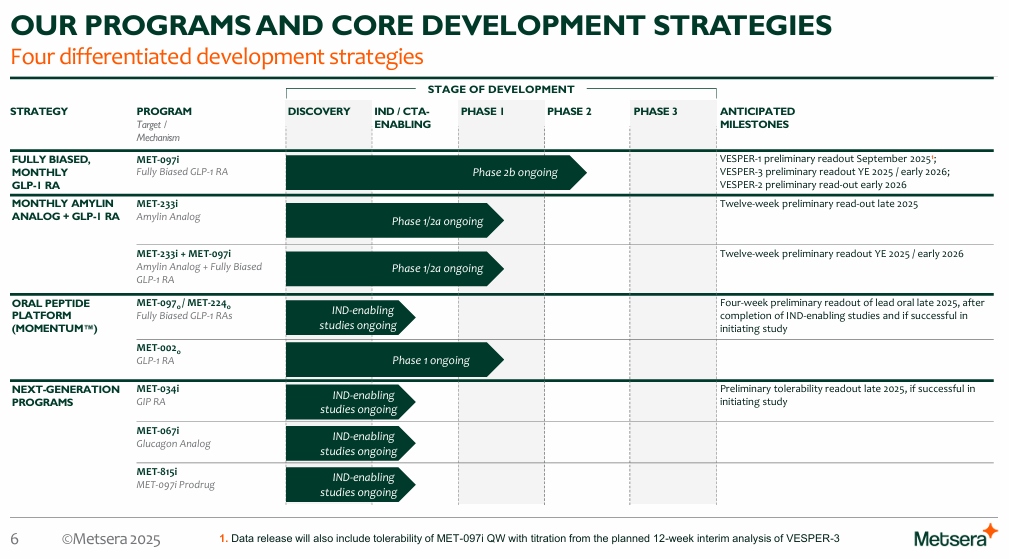

Sionna Therapeutics에서 10월에 발표한 회사 프리젠테이션은 아래와 같습니다. 현재 SION-451 (NBD1 Stabilizer)을 SION-2222 (TMD1 Stabilizer) 혹은 SION-109 (ICL4 Stabilizer)와 겸용하는 임상 1상을 진행 중에 있습니다. Sionna Therapeutics의 새로운 CFTR 신약들이 새로운 메카니즘을 통해 새로운 치료제로 성공할 수 있을지 귀추가 주목됩니다.

Bruce Booth – Atlas Ventures’ 20-year reflection (2) People")

Carisma: CAR-M Therapy")

Bruth Booth – Atlas Ventures ‘ 20-year reflection (1) Science")

The Power of Compounding Relationships vs Transactional Relationships")

Alloy Therapeutics: Better medicine together – drug discovery one-stop shop")

Voctave 공연 관람기")

TIPS Ladder")

Adimab LLC: One-stop antibody shop with discovery and non-exclusive partnership")

Metsera: Oral Peptide Drugs Acquired by Pfizer")

Sionna Therapeutics: Genzyme Spinoff for CFTR")